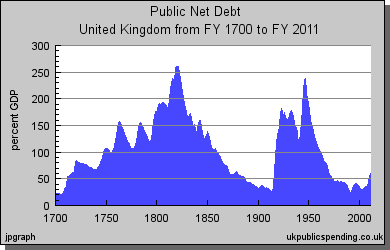

On 20 March George Osborne, the UK’s Chancellor, will present his budget. So far he has made a valiant attempt to cap public sector spending, particularly when compared with other finance ministers who were slow to adopt austerity. He has reduced public sector spending from what it would otherwise be, but has not managed to cut the total figure. His strategy now for controlling the budget deficit increasingly depends on higher tax revenues from a combination of forecast economic growth and more aggressive tax collection.

He may be unaware that this is too optimistic. He is advised by a Treasury staffed by economists who believe that through a process of economic modelling and continual refinement of method their control over the desired outcome will be improved. Errors of the past are therefore less likely to be repeated in the future. This approach is the key to understanding the forecasting method upon which Osborne’s budget assumptions are based, and it is completely wrong.

Keynesians and monetarists share a belief that mathematical models are a valuable forecasting tool. For this to be true individual consumer and capital transactions in the future as well as the prices at which they occur have to be calculable: this is obviously not the case. The economic effect of future technological and other relevant developments has to be factored in; but how can this be known? Future demand for British goods from overseas buyers has to be assessed, over which no one has any control. Future currency rates against sterling have to be predicted – a sore point at the moment with sterling dropping like a stone.

The fact that different economic models come to similar conclusions is a reflection of the commonality of their assumptions and construction, not independent confirmation of future economic trends. Instead we must use reason.

By taking economic resources away from the private sector through taxation and monetary debasement you reduce the potential for economic progress. By continuing to support and promote favoured public sector activities (the primary function of every government department) you ensure that resources are tied up in production the market would not itself choose to support. By regulating freedom out of consumer choice, you suffocate basic free-market efficiencies.

Today’s suppressive economic policies ensure that the economic future will disappoint. Consequently, future tax revenue is overestimated, as well as any reduction of public sector costs associated with economic recovery. If some of the smarter minds in the Treasury suspect this, their instinct will be to increase taxes further to protect government finances.

Meanwhile, storm clouds are gathering, with sterling under pressure. Perhaps it has more to do with the failure of monetary policy to rescue the economy, and the likelihood that the Bank of England will choose yet more easing, than any pre-budget nerves. One wonders how many of those econometric models incorporated a 7% slide against both the US dollar and the euro since the New Year. Either way, a sterling crisis is hardly a propitious background for a budget, painting George Osborne into a very difficult corner.

On fiscal policy Mr Osborne has not cut government spending – but has endlessly talked as if was cutting government spending.

Thus getting the worst of both worlds – the political cost of a cut in government spending, without the economic benefit of actually cutting it.

On taxation – Mr Osbourne has increased taxes. Even his recent “tax cut for the rich” (the cut in the top rate from 50% to 45%) is actually hiding a tax INCREASE (when the stamp duty changes and so on, are taken into account).

Again Mr Osbourne has managed to “achieve” the political cost of a “tax cut for the rich”, whilst not getting the economic benefit of actully cutting taxation.

And, of course, the “infrastructure” schemes (HSII and so on) the Corporte Welfare, so beloved by the Financil Times, continues

Turning to monetary policy…. Mr Osbourne supports the Bank of England policy of propping up the credit-money expansion (the bubble)especilly in the real estate (property) market.

The same man (Mr Osbourne) who complains about the price of housing is the man who is keeping up that price with loose monetary policy and lending schemes.

The wild monetary policy is also, of course, responsible for the situation in the stock market and bond market.

During the tenure of Harold Wilson, when Jim Callaghan was Chancellor of the Exchequer, it was revealed that the Treasury had an economic model that had charted the way to overcome the recession.

Some decades later it was revealed the economic model that the Treasury then had was in fact a mechanical model in the basement that had a main chute and a number of subsidiary chutes stemming from it.

The idea was that they poured water down the main chute, which represented the economy and they were able to see where the water went.

A bucket full of water would take a different course to a cup full and this was supposed to show what happened when the money supply was increased.

Childish though this might seem it had the advantage that you could see what went in as well as what came out and where. These days they have computers where you see only what comes out.

I liked Jim Callaghan – his speech to the Labour Party Conference (admitting that Keynesianism was wrong, and that he himself had been wrong when he was a Keynesian) took real courage.

Of course “Sunny Jim” was no Austrian School man (or really any School of economic thought), but he had a bit of common sense (in the ordinary sense of the term).

I quite like the water chute thing as well.

“But Paul…..”

I know, I know – I am clearly going into my second childhood.