“Sir, Martin Sandbu writes: “We should not worry about inflation – if we strip out volatile or policy-driven elements, it stands at 1.5%, according to Citigroup”, (“Carney has not yet bent the markets to his will”, August 14.)

“Please arrange for Mr Sandbu to cancel the policies concerned and to prevent the volatile situations encountered. When was the last time inflation was 1.5% ? This comment is as meaningless as my saying: “If savings rates were 5%, then I could afford two more holidays a year.” They aren’t, and I can’t.”

– Letter to the editor of the Financial Times, from Mr Charles Kiddle, Gateshead, UK.

King Cnut The Great, more commonly known as Canute, was a king of Denmark, England, Norway and parts of Sweden (thanks Wikipedia !). He is likely to be known to any English schoolchildren still being educated for two specific things: extracting Danegeld – a form of protection racket – from the citizenry, and for the possibly apocryphal story that once, from the shoreline, he ordered back the sea. Over to Wikipedia:

Henry of Huntingdon, the 12th-century chronicler, tells how Cnut set his throne by the sea shore and commanded the tide to halt and not wet his feet and robes. Yet “continuing to rise as usual [the tide] dashed over his feet and legs without respect to his royal person. Then the king leapt backwards, saying: ‘Let all men know how empty and worthless is the power of kings, for there is none worthy of the name, but He whom heaven, earth, and sea obey by eternal laws.’ He then hung his gold crown on a crucifix and never wore it again “to the honour of God the almighty King”. This incident is usually misrepresented by popular commentators and politicians as an example of Cnut’s arrogance.

This story may be apocryphal. While the contemporary Encomium Emmae has no mention of it, it would seem that so pious a dedication might have been recorded there, since the same source gives an “eye-witness account of his lavish gifts to the monasteries and poor of St Omer when on the way to Rome, and of the tears and breast-beating which accompanied them”. Goscelin, writing later in the 11th century, instead has Cnut place his crown on a crucifix at Winchester one Easter, with no mention of the sea, and “with the explanation that the king of kings was more worthy of it than he”. Nevertheless, there may be a “basis of fact, in a planned act of piety” behind this story, and Henry of Huntingdon cites it as an example of the king’s “nobleness and greatness of mind.” Later historians repeated the story, most of them adjusting it to have Cnut more clearly aware that the tides would not obey him, and staging the scene to rebuke the flattery of his courtiers; and there are earlier Celtic parallels in stories of men who commanded the tides..

The encounter with the waves is said to have taken place at Thorn-eye (Thorn Island), or Southampton in Hampshire. There were and are numerous islands so named, including at Westminster and Bosham in West Sussex, both places closely associated with Cnut. According to the House of Commons Information Office, Cnut set up a royal palace during his reign on Thorney Island (later to become known as Westminster) as the area was sufficiently far away from the busy settlement to the east known as London. It is believed that, on this site, Cnut tried to command the tide of the river to prove to his courtiers that they were fools to think that he could command the waves. Conflictingly, a sign on Southampton city centre’s Canute Road reads, “Near this spot AD 1028 Canute reproved his courtiers”.

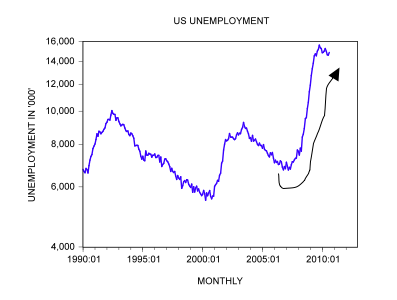

Cnut did exist, even if his mythologised battle with Nature was a fabrication. And for anyone who thinks that politicians are capable of learning from disastrous policy failures, the following lesson from history is also instructive. Explicitly linking economic policy and monetary policy rates to unemployment rates is not an innovation of either Ben Bernanke’s Fed or Mark Carney’s Bank of England. As Ferdinand Lips points out in his ‘Gold Wars’ (hat-tip to The Real Asset Company’s Will Bancroft):

With the passage of [the US Employment Act of 1946], the US government officially declared war on unemployment and promised to maintain full employment regardless of cost. Thus, it hoped to eliminate the business cycle and to prevent the country from ever sinking to the economic depths of the 1930s.

In the 1950s and the 1960s a weekly column in Barron’s called “The Trader” was written by a certain Mr. Nelson. Week after week, he untiringly drew readers’ attention to the consequences the Employment Act had on the purchasing power of the currency..

One would have thought that economic central planning would have been somewhat discredited after the Soviet empire collapsed in 1989, in favour of free markets. That message has yet to get to the US Federal Reserve or the Bank of England. But the Soviet experience is doubly instructive, in that it shows just how long a fatally dysfunctional system can last in the face of its obvious, existential, contradictions and absurdities.

Our thesis is that we are perilously close to the disorderly end-stage of a 40 year experiment in money and unfettered credit. That experiment started when US President Nixon took the US dollar off gold in 1971, and in the process created a global unbacked fiat currency system for the first time in world history. The history of paper currencies is instructive, too. Not one has ever lasted. Fast forward 40 years.. Texan fund manager Kyle Bass points out that total credit market debt now stands at some 360% of global GDP. For an individual country to maintain a debt to GDP ratio of 250% is consistent with that country deficit-spending its way through a war – such as was the position for the UK in 1945. For the entire world (read: notably the western world) to be loaded with such an untenable debt burden today suggests that something has gone catastrophically wrong with our banking and credit system.

We don’t know what the future holds but, crucially, our investment process does not explicitly require us to, and we have engineered it such that our process carries a degree of insurance against our own overconfidence as asset management fiduciaries. The market can be directed, coerced, bribed, manipulated, distorted and pummelled, but we don’t believe it can ever be completely destroyed – despite the best efforts of central bankers. There is early evidence that bond market vigilantes have had enough with QE and other desperate policy manoeuvrings, and are voting with their feet. If bond yields continue to rise, think very carefully about your exposure to market risk in all its other forms. We have, and are positioned accordingly.

In the current context, if Cnut did ever order back the tide, whether he did so to instruct his courtiers or to display his arrogance over the forces of nature is somewhat moot. The great physicist Richard Feynman made a similar admonition to NASA after the 1986 space shuttle disaster ending up killing seven crew members. In his infamous warning to a bureaucracy seemingly overtaken by ‘spin’, he said in his conclusion to the Challenger report,

For a successful technology, reality must take precedence over public relations, for Nature cannot be fooled.

For Feynman, and for Cnut, it was Nature. For us, it is the markets. Modern critics of the central banks, like ourselves, would suggest that we now have a modern equivalent of Cnut’s Danegeld, in the form of punitively low interest rates, rates which are being kept artificially low to try and resurrect a borderline insolvent banking system which is still content to pay significant executive bonuses and, in some instances, even dividends (to shareholders foolish enough to own common stock issued by banks whose fundamental value cannot be remotely assessed on any sensible economic basis). The economy, in other words, is being held hostage to cater to narrow and largely unreconstructed banking interests. At the same time, the farce of “forward guidance” – the pledge to keep interest rates unchanged until there is tangible evidence of economic recovery, almost irrespective of the latent inflationary pressure being stoked up – is being revealed as farce by Gilt yields that have risen by over 100 basis points since May (and the same holds for US Treasuries). Despite the king’s orders, in other words, the tide continues to come in.

A version of this article was previously published at The price of everything.

The reaction of the British and American governments (for they back the Central Bankers) to the wild credit bubble policies that produced the 2008 bust has been (and is) to follow ever MORE wild policies (both monetary policy and fiscal policy is now even WORSE than it was before 2008).

It is impossible not to be depressed over this, the struggle is to avoid becoming suicidal.

“In 2008 we had a financial crisis, the next train station stop is when governments go bust and I believe in the western world they ALL go bust! But before they go bust they will print money and then we go to war and all of us will be doomed!” ~ Marc Faber, Feb 2009.

Never gets old. Gibraltar looks like a nice start to proceedings

Tim, I think you have misspelled Cnut in your article about Mark Carney. It should of course be spelled Kanute..

Either spelling of Cnut or Kanute is correct. Over the course of a thousand years and many translations anything close to phonetically accurate should be considered correct. When my ancesters left the Norskland to invade America, barely a century ago, it resulted in a great variety of spelling for some family names. I have seen my grandfather’s first name spelled various ways and the family name has two spellings in common use.

Excellent piece Tim