“Interesting. Sex works even better than chocolate to modify behaviour. I wonder if anyone else has stumbled onto that.”

- Sheldon Cooper (Jim Parsons) in The Big Bang Theory.

In The Cluetrain Manifesto, four tech-savvy thinkers, back in April 1999, suggested how the Internet was going to change everything, not least business as usual. A latter-day reworking of Martin Luther’s 95 Theses, the Cluetrain Manifesto posited that

All markets are conversations

and went on to argue that

The Internet is enabling conversations among human beings that were simply not possible in the era of mass media.

Their argument struck a chord with this correspondent, who at the time was advising wealthy investors who were clients of Merrill Lynch Private Banking in London. It became clear that something tangible was shifting the tectonic plates of finance when, shortly afterwards, the market capitalisation of Merrill Lynch, with its 13,000-strong army of US financial consultants, was overtaken by the market capitalisation of Charles Schwab, the leading online (and no frills) broker of the time. This correspondent didn’t need to be told twice, so fairly soon after that he elected to abandon the thundering herd and take his chances in the New Economy, and with a new business.

Twenty years on, it’s plausible to argue that the impact of the Internet was, if anything, understated at the time. Of course, we experienced the first dotcom boom, and the attendant bust, but the likes of Facebook and Twitter were yet even to be twinkles in their founders’ eyes. And if any sector has been conclusively disrupted by digital technology, traditional media are surely in the frame as Exhibit Number One.

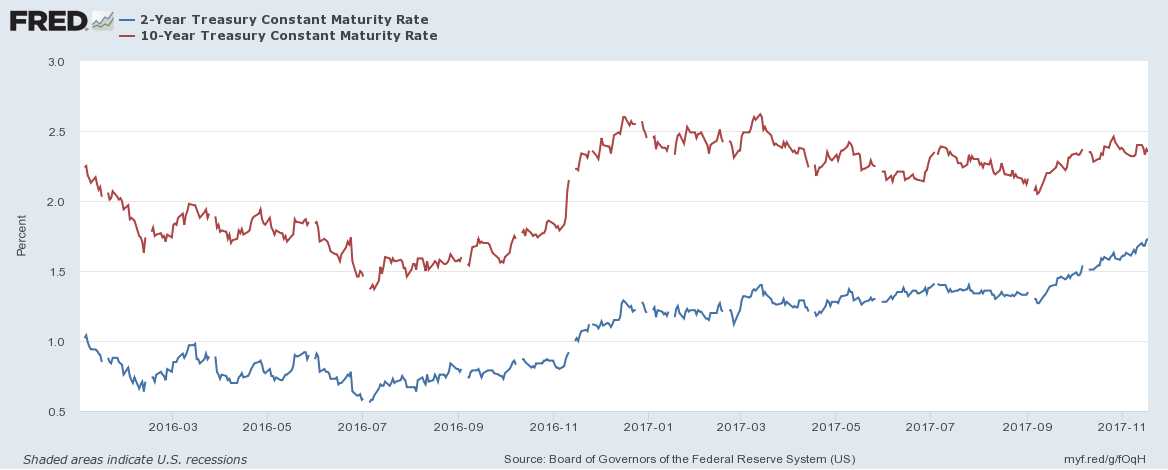

Ten years after the most damaging financial crisis in living memory, the role and fundamental relevance of the traditional financial media is in doubt. With interest rates rising, albeit slowly, from 5,000-year lows, one might expect the financial media to be asking more searching questions about the possible implications for investment markets, and thus for the portfolios of their readers. One might also expect the mainstream financial media to be asking more searching questions about the status quo in investment markets more generally, such as: was it a good idea for central banks to interfere powerfully with the free market mechanism by creating trillions of dollars in ex nihilo money and pumping them into the bond and stock markets ? If it was a good idea, who benefited ? At what cost ? Is there not a strong case for now debating the role and mandate of our central banks ? But on this topic, there is radio silence from the traditional financial media. The howl of conventional thinking can be deafening. In the UK, the two most celebrated journals of financial matters, The Financial Times and The Economist, failed, for example, to anticipate Brexit, advocated strongly against it, and still machinate against it. Anyone inclined to scepticism might conclude that these publications remain firmly on the side of the Establishment, and conclusively on the wrong side of history. Last week The Financial Times stirred itself from its apparent slumbers to report the shock revelation – egged on by its own agents provocateurs – that in a male-only gathering of wealthy businesspeople fuelled by alcohol and accompanied by flimsily clad hostesses, some of said gathering will behave unreasonably. The Financial Times may wish to follow up on this trailblazing scoop by visiting any pub, nightclub or strip club and reporting on their findings.

The FT is and should be free, of course, to flaunt its social justice warrior pretensions, and its ability to recognise and join a bandwagon, like any other creature of a market in free speech. But we already have tabloid newspapers. So what exactly is the FT for ? What is its raison d’être in 2018 – other than to defend the interests of Davos Man ?

On the topic of Davos Man, billionaire hedge fund manager Ray Dalio generated a fair amount of column inches last week in stating that

We are in this Goldilocks period right now. Inflation isn’t a problem. Growth is good, everything is pretty good with a big jolt of stimulation coming from changes in tax laws.. If you’re holding cash, you’re going to feel pretty stupid.

Which is quite a longwinded way of spelling ‘hubris’. Not to be outdone, the centa-millionaire CEO of asset gatherer BlackRock chimed in, urging investors to stop keeping money in cash as stock markets melt up to fresh highs.

As we discuss in our latest podcast with Paul Rodriguez, it helps to treat such musings with more than a pinch of salt. Asset management is riven with conflicts of interest, never more blatantly than when senior executives of gigantic asset gathering firms offer unsolicited and unchallenged investment advice to the public, and when said advice is then reported entirely uncritically by the financial media. Could these speakers by any chance have something to gain commercially by urging savers into risk assets at their most expensive levels in history ? This is not to say that the US stock market can’t ascend to fresh highs, but rather simply to point out that the ‘100% cash / 100% fully invested in equities’ proposition is a false paradigm. It grotesquely oversimplifies the subtleties and nuances required to navigate the financial markets in early 2018. Investors everywhere have a choice amongst a multitude of asset classes, investment approaches and discrete investments.

Ben Hunt, in his ever-excellent Epsilon Theory note, highlights the complacency of many current investors during this melt-up, and humbly suggests that the Federal Reserve simply cannot act as the investor’s saviour as and when markets correct; some form of hedging against the Establishment is required:

Each of these modern vampires of the Nudging State and the Nudging Oligarchy shares a certain DNA. Not to get all Marxist here, but these vampires share the DNA of Capital, in opposition to the DNA of Labour, and this is why you will never see the Fed or any other central bank lift a finger against them. Because the Fed is also a creature of Capital — not a vampiric destroyer as these modern manifestations of Capital have become — but a creature of Capital nonetheless.

Meaning what, Ben? Meaning that all of the Fed’s policies — and particularly the monetary policies that are most impactful on our investment portfolios — are in the service of Capital. Sometimes, as we’ve experienced over the past eight years, that means incredibly accommodative monetary policy to support asset collateral prices. Sometimes, as we’ve seen in the past and I think we’re about to see again, that means punitive monetary policy to crush labour and wage inflation.

I don’t know how this change in monetary policy regime plays out. I don’t know how quickly punitive monetary policy happens or how far it runs. I can’t predict it. But I know that the Fed won’t prevent it, because the Fed isn’t your protector, and that’s what you should hedge against in an intentional, systematic way.

In real life it’s never the monster that goes bump in the night that gets you.

It’s always the monster in plain sight.

Speaking of monsters, we get an eerie reminder of the Orwellian nature of modern media through the prism of Vanity Fair, of all things. First, in one of Annie Leibowitz’s photo shoots, Reese Witherspoon gains a third leg. Then Oprah Winfrey gains a third hand. The most disturbing Photoshopping, however, is not a sin of commission but a sin of omission. Having been accused of inappropriate behaviour by a number of women, the actor James Franco is digitally removed from the magazine altogether. Modern media, telling you how it is.