Inflation To Rise – We expect UK, ECB and US Policy to Diverge

Purely for geopolitical reasons, namely frustration at the failure of the governments of individual member states to respond to repeated calls for “structural reforms”,…

For honest money and social progress

For honest money and social progress

Purely for geopolitical reasons, namely frustration at the failure of the governments of individual member states to respond to repeated calls for “structural reforms”,…

Central Banking How will Central Banks cope with 2017 shocks? Perhaps new rules, one-off solutions, doubtless lots more QE. Populism will perhaps be their…

Central Banking Global Bond Market Yields are Rising The ECB’s recently announced 6 month extension of its QE programme reminds us that the speed…

“The key thing to know about Lehman Brothers is that it did not cause the financial crisis, it revealed the financial crisis”[1] Central Banking…

The ECB must be aware that investors’ confidence in stock markets, particularly bank shares, dropped in January. If contingency plans exist, they are likely…

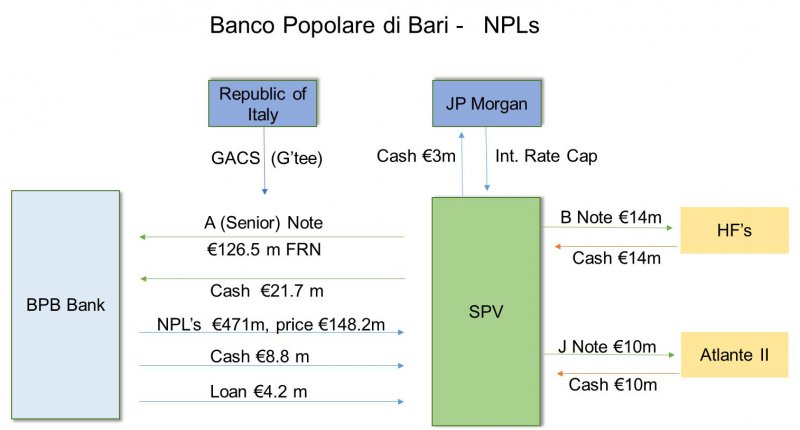

The Cobden Centre’s Gordon Kerr can be seen on Bloomberg discussing the Euro and the state of Europe’s banks, which are now in a…

Central Banking Low interest rates contribute to weak labour markets In the latter part of August, the cream of the world’s central bankers convened…

Late last year, a group of institutional investors sent a letter to officials in Brussels, warning that European Union accounting standards are “destabilizing banks”…

The evolution of banking as I have described it has satisfied the immediate demands of shareholders and managers, but has short-changed everyone else. There…

The Guardian: Bank of England official calls for bespoke accounting standards for banks The Telegraph: New bank accounting rules needed to avoid another crisis,…