ValueWalk interviews Detlev Schlichter

byReproduced by kind permission of Jacob Wolinsky at ValueWalk.com Can you tell us a little bit about your background? I studied economics in my…

For honest money and social progress

For honest money and social progress

Reproduced by kind permission of Jacob Wolinsky at ValueWalk.com Can you tell us a little bit about your background? I studied economics in my…

A very old and well known story is told in Genesis 11. It is the story of the curse of Babel: Now the whole…

Regular readers of this site may be aware of a debate relating to the contractual devices that banks might use to ensure that they…

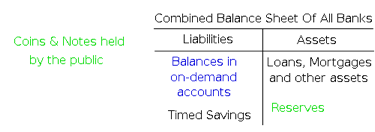

Steven Horwitz writes In some free-market circles fractional reserve banking (FRB) is blamed for everything from business cycles to bad breath. Defenders are seen…

Cross posted at Mises.org and The Coordination Problem. Come the Revolution, in a free banking world, where there is at least no lender of…

When discussing the “fraudulent” nature of fractional-reserve banking, the crux of the issue seems to be how the law distinguishes between banks and other…

On this website Toby Baxendale presented his plan for monetary reform. He offered a reward of £1000 for anyone who can provide a logical…

Last night, yours truly, along with a number of other Cobden Centre supporters and assorted free marketeers, listened to Toby Baxendale talk about a…

I offer a £1,000 reward for anyone who can tell me why this logically won’t work, practical politics, for now, being another matter. What…

If What Has The Government Done To Our Money? is an hors d’oeuvre, then The Mystery of Banking is the main appetiser in our…