Stockman: Good Riddance, Janet, You Were A Colossal Failure, Part 1

byThis is one for the record books. During Janet Yellen’s last week in office, the Dow dropped by 1,095points or 4.1%. But by her lights, apparently, that wasn’t…

For honest money and social progress

For honest money and social progress

This is one for the record books. During Janet Yellen’s last week in office, the Dow dropped by 1,095points or 4.1%. But by her lights, apparently, that wasn’t…

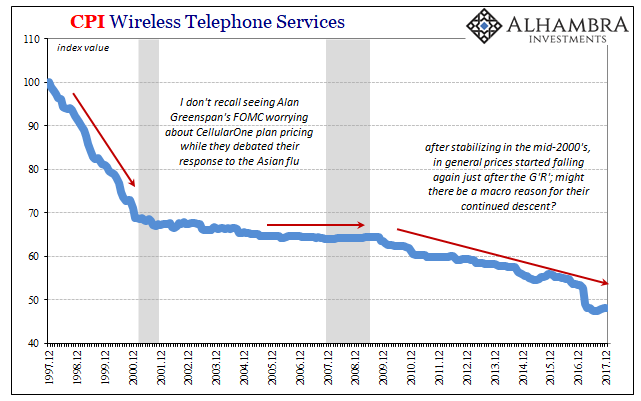

by Jeffrey P. Snider When Federal Reserve officials first started last year to mention wireless network data plans as a possible explanation for a…

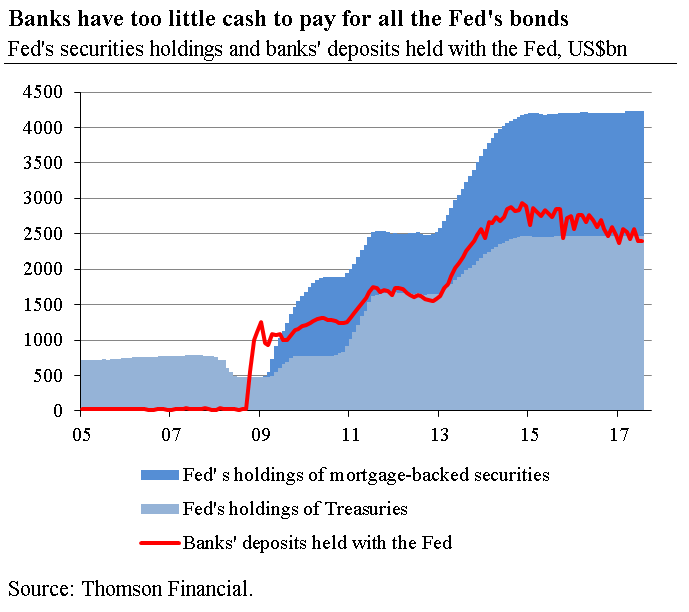

Ten years ago, before the collapse of Lehman Brothers rocked global financial markets, the Fed’s balance sheet stood at $925 billion—mostly U.S. Treasuries. After…

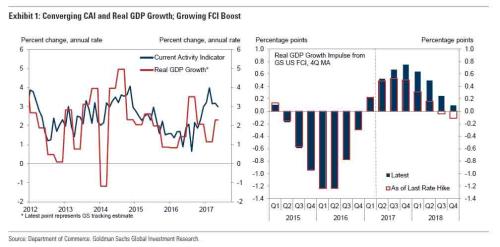

By Daniel Lacalle The appointment of Jerome Powell as the new chair of the Federal Reserve must be interpreted by the markets as a sign…

The Federal Reserve (Fed) is widely expected to continue to tighten its monetary policy this year. According to a latest Reuters Poll, the Fed…

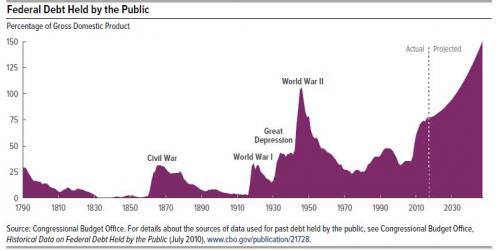

During her testimony this morning, Fed Chair Janet Yellen urged Congress to take into account the growth trajectory of the federal debt when making decisions…

by Mark Thornton Source here: https://mises.org/blog/bernanke-yellen-bubble-depression In a recent article I advocated for a new way of naming business cycles. The new approach emphasizes the cause rather than the…

On Wedensday the FOMC will hike rates by another 25 bps – an event which the Fed Funds market prices in with near virtual…

The US bond market trades at a quite high valuation. For instance, the 10-year US Treasury bond presents a price earnings (PE) ratio of…

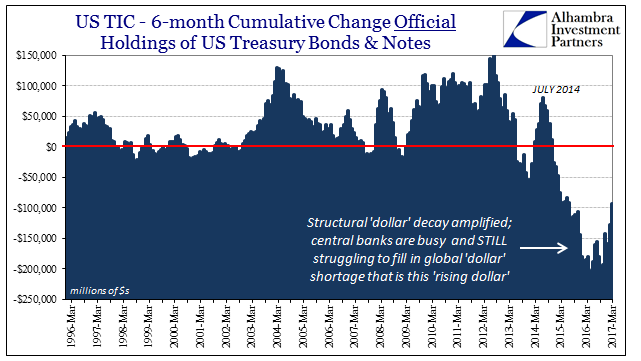

TIC data confirms that “reflation” captured more than just pricing sentiment. It appears to have occurred in bank balance sheet activity, and related official…