Merry Christmas from TCC: Treasury Select Committee to examine low interest rates

byNext year there will be a parliamentary enquiry into the effects of ultra low interest rates and other mechanisms of radical monetary policy. It…

For honest money and social progress

For honest money and social progress

Next year there will be a parliamentary enquiry into the effects of ultra low interest rates and other mechanisms of radical monetary policy. It…

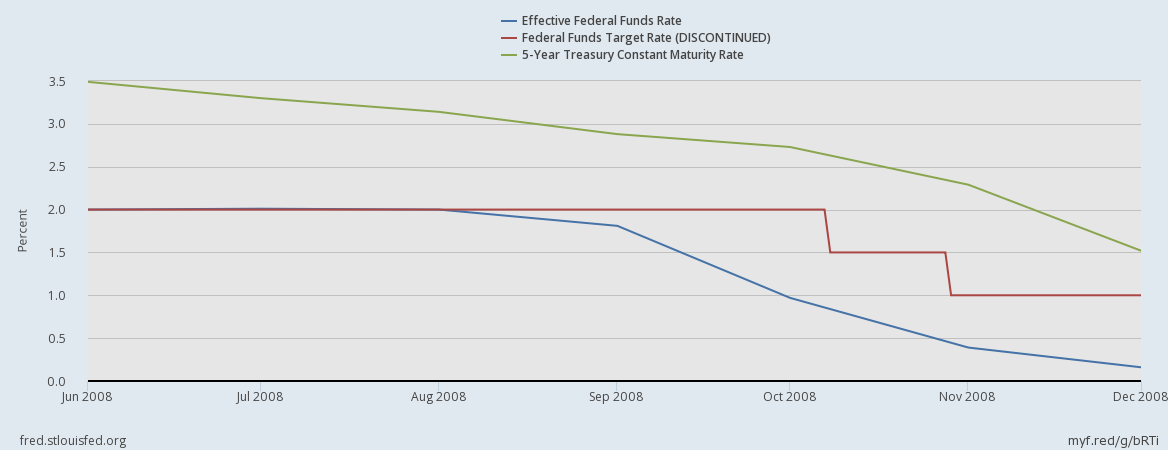

Source: https://www.alt-m.org/2016/12/01/fed-holding-interest-rates/ ONCE UPON A TIME, when my twin brother and I were tots, our father convinced us that he could make a traffic light…

A fall in the US unemployment rate to 4.6% in November from 4.9% in the month before and 5% in November last year has…

“..The iron convention observed by almost everyone in showbiz: no matter which way you vote in private, you must always pretend in public that…

In his speech at the New York Federal Reserve of New York on October 5 2016 the Federal Reserve vice Chairman Stanley Fischer has…

The violent exchange-rate fluctuations in pound sterling raise a host of issues that are causes for concern. Increased inflation is one of the primary…

I was recently flattered to be asked how I envisaged the dreaded ‘helicopter money’ working if it were not to simply add further to…

“There is no simple, painless solution. The world has to reduce debt, shrink the financial part of the economy, and change the destructive incentive…

A fall in the US velocity of money M2 to 1.44 in June from 1.51 in June last year and 2.2 in May 1997…

By Pater Tenebrarum Chopper Pilot Descends on Nippon Readers are probably aware of recent events in Japan, the global laboratory for interventionist experiments. The theories…