Via EEC/CERT/CESP/Warm Front – Picking Losers…, an argument that government intervention in the energy markets is counterproductive:

These programmes¹ are examples, like the EU-ETS, where government intervention hands commercial advantage to the VILE (Vertically-Integrated Large Energy) companies, to little beneficial effect.

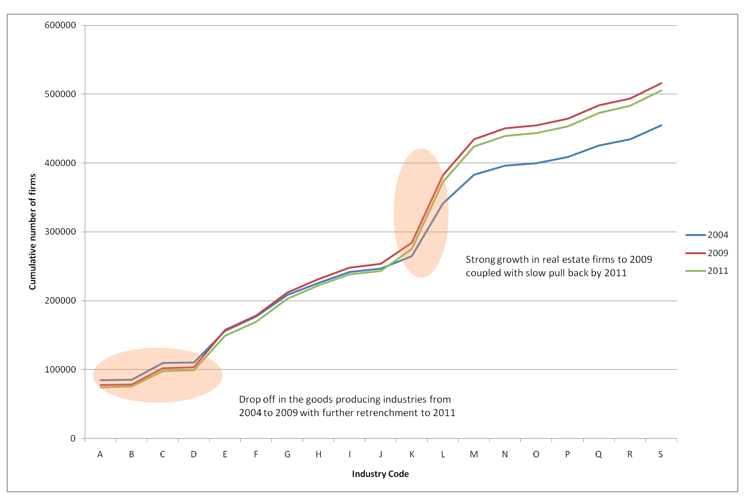

The VILE companies point to the fact that demand for domestic energy has fallen in the last couple of years, as evidence for their success. I have argued this was largely a response to price increases, increasing disparities between costs-of-living and disposable income, and warmer winters (until last year), and not the effect of their energy-efficiency programs. In my opinion, the timing demonstrates the point. EEC was introduced in 2002, and Warm Front in 2000, but domestic energy demand carried on rising until 2005², which coincidentally was when global wholesale gas prices spiked (consumers did not feel the full effect until Winter 06/07, but there was already concern and initial increases in 2005).

‘Energy Risk’ published an early critique of the ETS here almost five years ago

http://www.opencapital.net/papers/Opinionemissions.pdf

This presentation of mine at a gas conference in Rotterdam last week

http://www.slideshare.net/ChrisJCook/gas-market-presentation-03-12-2009

and a recent presentation in Scotland

http://www.slideshare.net/ChrisJCook/energy-pools-scottish-energy-institute-11-11-2009

both set out how it is simply possible to ‘unitise’ energy in a way that should be comprehensible to anyone who understands Air Miles or the Tesco Club Card.

We may thereby create a simple but radical alternative to the deficit-based nonsense being discussed in Copenhagen, and which was invented by Enron and brought to us by the same people who brought us the Credit Crunch.

The requirement is indeed for honest currencies, and a Value Standard or benchmark for exchange which is relevant to the average man on the street.

In that context, while I regard gold as an obviously fungible currency (one of several) its lack of utility renders it less relevant than (say) a Unit of energy which would give rise to transactions denominated in energy.

As I have said many times: oil is not priced in dollars; dollars are priced in oil.

I sat next to a former MEP and banker before a dinner last week, who repeatedly told me it was “absurd” to advocate a gold-backed currency. He facetiously suggested it might as well be backed by Rembrandts. So let’s walk through the same scenario with Chris that I walked through with him. Let’s say I have deposits of £50,000 in two banks operating in two different currencies – one backed by gold, the other backed by energy (or Rembrandts). I become concerned that the currencies are being debased (i.e. they are issuing more paper than they have backing commodity in their reserves). I go first to the bank with the gold-backed currency and withdraw my deposit as gold. I then go to the bank with the energy- (or Rembrandt-) backed currency and… What? Ask for the equivalent amount of energy (or a tiny corner of a Rembrandt) to stick in my pocket?

It offends many people’s sensibilities that a commodity with limited practical use, such as gold, should be accorded greater value as a monetary standard than other commodities that might seem to have greater “use value”. But that is simply because they have not made a serious study of the theory of money (or read the works of those who have) and have therefore failed to understand the nature of money. Chris and I have actually debated this before, on an energy mailing list dominated by socialists (see e.g. http://claverton-energy.com/pipermail/claverton-group_claverton-energy.com/2009-August/001939.html), and we have established that Chris isn’t big on the theory of money. I think I’ve probably recommended it to Chris before, but just in case: before dreaming up new currency schemes it would be a good idea to read one or both of (a) Ludwig von Mises, “The Theory of Money and Credit”, and (b) Jesus Huerta de Soto, “Money, Bank Credit, and Economic Cycles”. As Prof. de Soto is a Cobden fellow, perhaps it would be particularly sensible in this context to read that one.

In any case, I fail to see what this has to do with the original subject of this thread.