I follow Steve Baker’s speeches in Hansard with interest, and there have been many good ones, but his recent discourse on the IMF stands apart. It was made in the debate of the Draft International Monetary Fund (Increase in Subscription) Order 2011 by the “Second Delegated Legislation Committee”.

The unexcitingly-named proposal before this obscure-sounding committee would commit an additional £10 billion of British taxpayers’ money to the IMF.

11.39 am – Steve Baker

…

I begin by welcoming the Minister’s resolve and composure in what are clearly historic and contentious circumstances. We have seen today that there is broad agreement across the Committee that what matters is human prosperity, and we are all deeply worried about our constituents. I am going to make three points. First, I do not believe that we have this money and that we cannot afford the liability. I do not think that my constituents will understand why they should pick up the liability. It seems to me that one way or another, this country will end up borrowing in order to lend to fund present consumption, and funding present consumption through borrowing is simply not a route to prosperity. I wish I felt that it was not necessary to expand on that point, but it seems these days that we forget. If we consume on credit, we are in fact making ourselves poorer.

I find the notion of getting the money back quite worrying. It seems to me that we will borrow some of this money, at least, from commercial banks, inevitably monetising the debt and debasing the currency further after 40 years of continuous debasement. That will involve inflation and further distortions in the structure of the economy. In short, this measure would simply kick the can down the road. We might argue that that is the job of the IMF these days, but the Greek people are already rioting and we have to ask ourselves whether they would be any more sympathetic to such austerity measures simply because they were brought forward by the IMF. I question the action itself.

Secondly, the IMF was created as part of the Bretton Woods system of currencies. We tend to talk as though our current monetary arrangements were a fixed point and had always been the same, but the present monetary orthodoxy has evolved over the years and centuries. Bretton Woods was constructed after the catastrophe of the second world war; the dollar was redeemable in gold, and all other currencies were pegged to the dollar. The job of the IMF was to stabilise exchange rates by bridging temporary gaps in nations’ balance of payments, but the IMF now seems to serve the purpose of ensuring the repayment of reckless financial institutions.

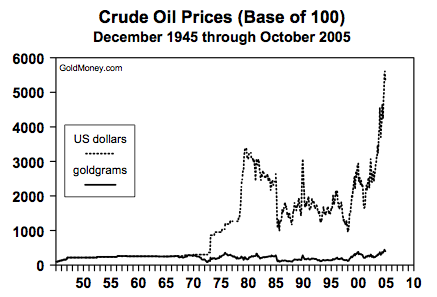

Above all, at all stages of its history the IMF has existed to bring financial stability, which I believe it has singularly failed to do. Turning to the monetary system and stability, I encourage Members to google a chart that I can make available, which shows the price of oil-index factor 1945, the origin of Bretton Woods-brought forward to today. It prices oil in dollars and in gold. I do not like to use the G-word, but I feel that since my hon. Friend the Member for Wellingborough has mentioned it already, I can continue. The price of oil has been high and volatile since 1971, but only when priced in dollars. If we price oil in gold, the price has been low and stable ever since the end of the second world war.

I simply make the point that our monetary arrangements are not fixed, that the IMF has not brought stability and that in fact many of our most important commodities are far more susceptible to the effects of our present, inflationary monetary arrangements than is generally considered. I would like to finish my point about the IMF with Hayek’s words. He said:

“monetary policy all over the world has followed the advice of the stabilisers. It is high time that their influence, which has already done harm enough, should be overthrown.”

He wrote that in 1932 in the preface to “Monetary Theory and the Trade Cycle“, which hon. Members can find by googling “prices and production.”

Thirdly, I want to talk about the contemporary mainstream. With great respect to hon. and right hon. Friends, although my right hon. Friend the Member for Wokingham foresaw many aspects of the crisis, the majority of the mainstream did not see this coming. I have sat at lunch with eminent economists who said that nobody saw this coming, to which I simply replied that they should read Huerta de Soto’s “Money, Bank Credit and Economic Cycles“. That book, which was written in 1998, clearly set out that this would happen and why, following in the footsteps of Hayek, Mises and others. The Queen asked why no one saw this coming. If she had asked me, I would have said that it was because economists pay too little attention to time-the simple matter of the importance of time. Production takes time and, in a market, interest rates should arise from people’s time preferences for consumption. In the jargon, the contemporary mainstream lacks an adequate theory of the inter-temporal structure of capital-that is, capital goods, or the means of production.

We are at the end of an extremely long credit expansion. I depart from my right hon. Friend the Member for Wokingham, but that is because I follow that particular theory of capital. Hayek, it is not often known, was a socialist and confesses as much in the preface to Mises’ book, “Socialism“, but he and Mises together worked out the theory of the trade cycle. Mises wrote:

“The wavelike movement affecting the economic system, the recurrence of periods of boom which are followed by periods of depression, is the unavoidable outcome of the attempts, repeated again and again, to lower the gross market rate of interest by means of credit expansion.

There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.”

That is from “Human Action“, page 572.

At this point came an intervention to delight Cobden Centre readers:

Mr Cash: My hon. Friend’s contribution is very thoughtful; he knows a great deal about such things, in the tradition of Cobden. However, is the real problem one of human nature as well as of economics? People are competing in an environment in which there is no real or comparative advantage because the new world-if I may use that expression-of the Brits has a huge advantage over the others. Good money is being thrown after bad unless the real problem is tackled: cheap credit that is not based on real, tangible economic advantage.

Steve Baker: I absolutely agree with my hon. Friend. He makes an excellent point with which I am in full agreement.

Mr Redwood: Before my hon. Friend sits down, I hope that he will give the Committee the benefit of his advice on the order, because we are not yet quite clear what he would do about the £9.5 billion sub.

Steve’s concluding remarks pull no punches (emphasis mine):

The Government should avoid committing that sum of money; my view is that it will not help. I made a second point about the IMF and our monetary arrangements. If this is not the time of all times to question the fundamental basis of our financial system, I do not know when we ever shall. My third point was that I am afraid that the contemporary mainstream of economics is missing some vital information, which leads it to justify the very measures that we are discussing today. As I explained, as Mises set out, as Hayek followed in his steps and as others have predicted, we risk a final and total catastrophe for our currency system.

To conclude, we are in danger of simply kicking a can down the road and, as my hon. Friend the Member for Clacton said, ladling water into the boat. We are looking at further credit expansion, further monetisation of debts and further socialisation of risk. Throughout the western world, we are in danger of appearing as King Canute, trying to use politics to hold back the realities of social co-operation, which we usually describe as economics. The IMF is an institutional legacy from a monetary system that failed 40 years ago, and the successor to which is even now failing as well.

I looked at IFRS and how it boosts bank capital, and we found that RBS is possibly overstating its capital by £25 billion. That must meant that RBS at least is far more susceptible to financial shocks than is generally thought. It is my view, because of the weaknesses of IFRS, that all banks are substantially more susceptible to financial shocks than is generally understood. I therefore offer three points. First, the Government should please look at cross-cancellation of debt held by sovereign nations-I refer the Government to work by ESCP Europe and Dr Anthony Evans. Secondly, let us face the reality-not optional-and look at how we restructure outstanding debt. Thirdly, at this time of all times, rather than merely increasing our liability to the IMF, let us seriously rethink the foundations of the international financial system and, in particular, start planning for how to protect the payments system.

{kind=link}

Great speech by Steve Baker. It is almost certain, however that he may as well be whistling in the wind. The narrative has already been lost, and the voter in the street believes (because that is what the media and ‘thinking opinion’ tells him) that the financial crises of the last few years are the result of the failings of capitalism, not the failings of state intervention in money supply etc. Ironically, the parties of the Left across the free world are flailing around for new ideas, and the lower-income families that should be their natural constituency are the most shafted by the state-controlled debt and inflation system. Will they ever join the dots and stand on the basis of re-structuring the banking system, limited state economic control plus sound, asset-backed money? Not a chance.

The situation reminds me of a scene from a great movie about the last days of Hitler, Downfall (no not that scene!). I am talking about the scene where Hitler’s cohorts and their wives are having a party, drinking and dancing, while Allied bombs are falling all around and the Soviet Army is mere kilometres away. The problem is that most people, whether our leaders or the population at large, don’t want to face the truth until they are staring at it down the barrel of a loaded gun.

Unfortunately, at that point its too late to do anything about it. Reality is dull, fantasy is so much more exciting.

@Robert Sadler

Whilst I agree with your general point, I don’t think that you’re right about that Downfall scene. There’s a similar scene in one of the Titanic movies where someone sits at the bar drinking whilst outside all is chaos. He doesn’t drink because he refuses to face the truth. He drinks because he does. The same is true about the people partying in Downfall. They can’t leave Berlin, they would be shot, and they know the Germans won’t win. This may be a form of escapism but it isn’t about perpetuating a fantasy.