Slovakia’s parliament recently voted against the proposed increase to the EFSF. The BBC’s Rob Cameron says “a second vote could be held soon and is likely to succeed”. This policy paper from INESS explains why Slovak politicians should stick to their first answer.

Slovakia should refuse an increase in the size of EFSF (European Financial Stability Facility) and enlargement of the scope of its competences for following reasons:

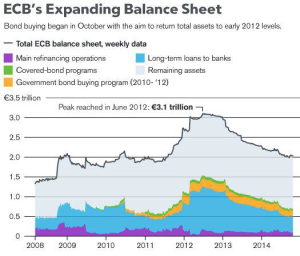

- The proposed solution to the sovereign debt crisis, based on redistribution of national debts in the form of EFSF, has proved ineffective throughout the 18 months since its inception. The “disease” continues to spread to other countries. Even the catastrophic scenario has come true – the European Central Bank has even had to come to the aid of Italy with its enormous debt. The crisis is not one of liquidity, but a problem caused by the insolvency of indebted countries and of many creditor financial institutions. Increasing the borrowings of insolvent nations will not address this crisis of insolvency, but will worsen the situation and will endanger the financial health of the other members of the Eurozone and weaken their access to financial markets (see the case of Italy).

- Political leaders have not been mandated by the voting public to bring about fiscal centralization, which naturally follows such a debt union.

- The suggested solution introduces the unsubstantiated transfers of wealth from taxpayers in one country to the owners and creditors of financial institutions who lent to the troubled countries.

- The EFSF and ECB operations are misleadingly described as a rescue of these countries. In reality they constitute a bailout of these countries’ creditors. If this proceeds it will lead to the growth of nationalistic tensions in the EU and so create risks for its long-term stability. In turn this will endanger the existence of the common market and its cornerstones, the free movement of goods, people and capital.

- Historical experience shows that the main precondition for long-term stability of monetary union is the maintenance of a credible commitment not to bail out any member. The long-term stability of the Eurozone and the euro currency would, contrary to the views expressed by the creators of EFSF, benefit from the bankruptcy of Greece. EU leaders are preventing this at any cost. For this reason, saying No to the increase of EFSF does not mean the end of the monetary union.

GDP is not the appropriate indicator to measure the wealth of Slovak population. Employee compensation and hence ability to pay taxes are substantially lower in Slovakia than in other Eurozone countries (with the exception of Estonia). Hypothetically, if all guarantees as per currently proposed EFSF were called (total amount: EUR 780 bn.; Slovakia’s share: EUR 7.7 bn.), our cost would reach 35% of total general government revenues – the highest share in the Eurozone. EUR 1000 of debt would burden the Slovak taxpayer twice to three times more than the German. To cover potential future costs brought about by membership of the EFSF, we would need to increase taxes twice as much as our neighbour, Austria.

The ‘solution’ to the European sovereign debt crisis via EFSF will therefore prove particularly expensive for Slovakia. Slovakia’s main competitive advantage is its relatively low tax rates compared to other members of EMU. The proposed expansion of EFSF will lower this competitive advantage. It will also hurt Slovakia with respect to the central European region, where few governments will be part of EFSF. The inability to keep Slovak taxes low will lead to lower economic growth, and slower catch up with the higher living standards of the more developed countries.

Slovakia has already passed costly reforms of social welfare system. Slovaks have also paid the bill for an extremely expensive (10% GDP) recapitalization of the Slovak banking sector just ten years ago. The acceptance of costs of bailout of wealthier countries with unreformed social systems and insolvent banking sectors would substantially eliminate the positive effects of these painful reforms. To accept the debts of wealthy and profligate countries will mean that the Slovak taxpayer has tightened his belt in vain.

Well said, good article. I love the evident bias in the BBC correspondent’s choice of words ”a second vote… is likely to succeed”. Rather depends what you call success, dear boy. On wha conceivable basis is the forced redistribution of wealth from Slovakian workers to owners of banks that gave Greece loans under the wrong terms a success?