I was asked recently why it is that market forces do not push down the wages of the top earners in financial services. The answer, it would seem to me, is that the profitability of the financial services sector is based on privilege, rather than normal economic activity, and it is this that drives hiring behaviour.

In a normal industry, where there is a profitable project, a number of different entrepreneurs have the ability to invest in this area. The act of investing produces a good that a consumer buys. The more of these goods produced, the lower the price that consumers will pay such that the profit making opportunity diminishes and the ability to pay higher wages/expand the business diminishes. This process is good for society since it provides more goods demanded by the public at lower prices. The entrepreneurs are motivated to hire additional people in order to invest in these areas increases profits to themselves. A beautiful system, I’m sure you’ll agree.

However, the profits of the financial service industry are far in excess of where they would be in a true market economy without fractional reserve banking/fiat currency/central banks. Profits within the industry are essentially a product of the net interest margin (difference between interest rates at the short and long end of the curve) and the outstanding liabilities (more credit lent means more profit).

The central bank’s action keeps the net interest margin wide since it buys government debt at the short end of the curve and has an inflationary bias. In addition, the ability of the central bank to continue to bail out the industry should it get into “liquidity” trouble encourages more risky behaviour – both in taking on additional leverage and taking additional duration risk. Hence the product of net interest margin and liabilities is artificially kept high by central bank action. These excess profits are paid for by the rest of society through higher inflation.

Given that the vast majority of the banking sector’s profitability is dependent on privilege, it makes no sense for a firm to hire additional people in order to exploit profit making opportunities – there are no opportunities. The rational response is to hire no one at all, except in the case where hiring defends and extends this privilege. This explains the army of remuneration consultants, the bank-funded pro-central bank economists, the lobbyists, the symbiotic relationship between government and banks particularly evident in the higher echelons of the US government where officials seem to pass between top positions in government and on Wall Street so easily.

Some hiring of people of course is inevitable in order that administrative work is done, and this is also beneficial in defending privilege since the industry can argue to the government, from whence its privilege comes, that it is an importnant provider of jobs. However, the insiders with the top positions are very reluctant to hire additional people since this would not increase their wealth though providing additional goods with demand, but rather dilute their privilege through more heads.

Hello Mr Lucas, thank you very much for the interesting and stimulating article. However, I have one question. Could you please explain what you mean by “The central bank’s action keeps the net interest margin wide since it buys government debt at the short end of the curve and has an inflationary bias.” This isn’t a challenge, simply a request for clarification. How does buying government debt at the short end of the curve keep the net interest margin wide?

Hi Thomas.

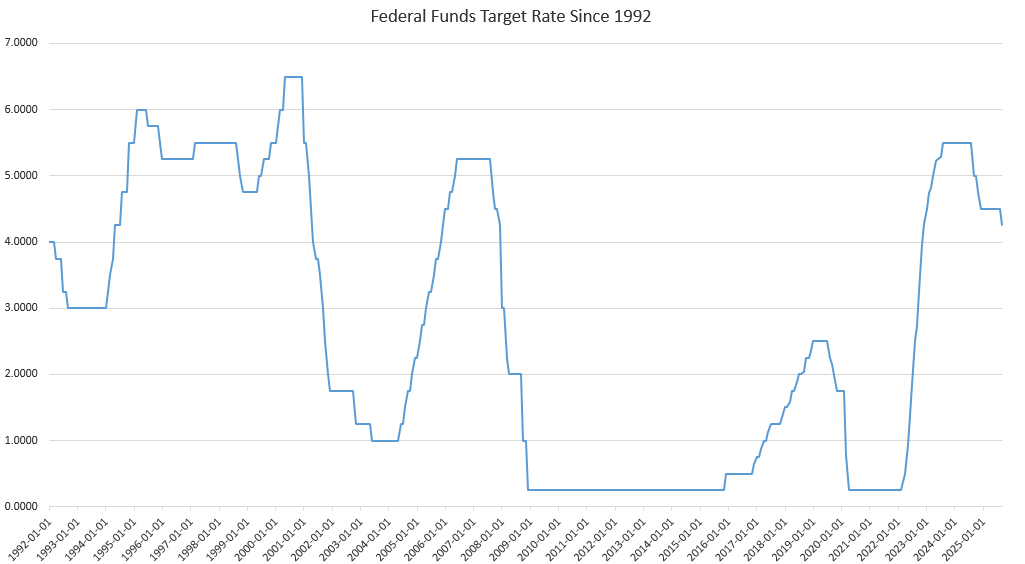

The central bank sets short term interbank interest rates (in the US, called the Fed Funds rate, and in the UK the BoE base rate). The method through which it does this is principally through making and withdrawing short-term loans to the banks. This trade is called the repo. A government bond of any duration may be bought or sold for a short period of time, mainly overnight (although the Federal Reserve will do repos for up to 2 months). After the term of the repo is finished, the loan is reversed and the bond is returned.

The cash that the central bank finds to make these repos is created from nowhere – it is entered on its balance sheet as a loan to itself. Since the central bank has an inflation mandate, it sets short-term interest rates such that enough new money is lent into this short-term loan market to give a positive inflation number over a given period of time. This ensures that it always makes ever more loans into the short term loan market as time goes on. It means that this short-term interest rate, the overnight rate, is permanently lower than where it would be in the absence of central bank action. It also means that commercial banks can take advantage of this where others cannot, borrowing from the central bank for the short-term at a lower rate than would otherwise be possible. This in turn allows them to make greater net interest margins, as the banks tend to lend this short-term money for longer durations. Lending for longer durations carries a higher interest rate, partly as it is risky to lend for longer periods of time, but mainly because the central bank does not interfere as much at longer durations – interest rates are set at the overnight level.

I hope that this helps.

Tim, are you talking about the BoE “base” rate or “bank” rate?

Sorry – it should be LIBOR, the interbank rate, which is targeted with reference to the BoE base rate.

I don’t mean to be pedantic – I think what you’re calling the “base” rate is more commonly known as “bank” rate, and there’s important differences in how the Fed targets the Fed Funds Rate and how the BoE affect LIBOR. As you say, the FFR is an interbank rate, the Bank rate isn’t.

Hello aje.

Apologies, you are quite right. So the system I describe above is more-or-less what happens in the US, where monetary policy is conducted through open market operations and the Fed Funds Rate is targeted. This is true except in the relatively few cases where commericial banks borrow directly from the central bank through the “discount window” at the discount rate, which is usually set higher than the interbank rate. I remember that that this form of borrowing became more common during the credit crunch, presumably because the the FFR was higher than target due to increased credit risk in the interbank market….I don’t know how much borrowing at the discount window currently occurs.

I think that the BoE simply sets the overnight rate, the base rate, and the quantity of cash supplied into the market is a derivative of this and the reserve requirements of the commercial banks.

In either case, I hope you’d agree that it is at the short that the central banks primarily target monetary policy and it is this that has allowed high net interest margins to be earned by the commercial banks, such that the premise of the article above is fair.

Yup – although the reserve requirements in the UK are voluntarily set so aren’t really “requirements”. Indeed the decision to pay interest on reserves, and thus adopt a separate interest rate that policymakers can manipulate, is a really interesting part of the credit crunch. I don’t think it’s a coincidence that the BoE began paying interest on reserves in 2006 (and the Fed in 2008) which is when they lost control of the monetary aggregates.

Ironically the purpose of a “corridor” system is to reduce central bank credit risk…

Also, you’re right that conventional policy targets short term rates. I was in the US when operation twist was announced by the Fed, and am not sure if it was discussed much in the UK. But I see QE as an implicit attempt to alter longer term rates, and operation twist as an explicit one. I also believe the consensus view was that it didn’t have much impact when initially attempted by Kennedy. I’m not sure whether it was deemed to have been a success this time around.

Finally, whilst we’re on the topic, be careful not to overattribute the role of the Fed. They are targetting the interbank rate but there’s lots of plausible evidence that they are essentially a noise trader that has little impact on the market rate. I believe the Fed’s marketshare of US Treasuries was falling throughout the supposed Great Moderation, suggesting other factors were causing the low interest rates.

Hi Anthony.

Yes – operation twist is widely seen as an effort to control long-term rates here too – though their hasn’t been much commentary on it of late.

You wrote: “Finally, whilst we’re on the topic, be careful not to overattribute the role of the Fed. They are targetting the interbank rate but there’s lots of plausible evidence that they are essentially a noise trader that has little impact on the market rate. ”

I wondered if you’d seen this paper? It provides evidence that it was the European banking system that was providing excess liquidity to the US banking system during the great moderation and was thus responsible for low rates. It makes a good deal of sense to me:

http://www.princeton.edu/~hsshin/www/mundell_fleming_lecture.pdf

If this is right, then it still makes sense to finger central banks as the culprits for low rates in the US – just European ones through their banking system rather than the Fed. As a result of the unprecedented quantity of cross-border flows, it seems that analysing a single economy without considering its position in world is fraught with danger.

I hadn’t seen that paper, thanks. I think you’re right that more attention needs to be given to cross-border flows.

Any idiot can make a fortune if they are allowed to print money out of thin air and charge interest on it!

This really is a no brainer. No competition no new entrants and no risk of failure. FM what else do you need for a business plan that excludes risk?

Hi Waramess – what you say isn’t quite true. There are new entrants into banking and there are plenty of banks which can compete against each other. While they are in receipt of a subsidy and an implicit government guarantee, there are plenty of industries that receive subsidies that are still cut-throat and even unprofitable. Airlines – for example – are notoriously unprofitable and yet every national carrier is favoured by its own government.

I think that what makes banks special in this regard is that virtually ALL their profit comes about as a result of privilege, so most time and money is devoted to protecting and extending this.

Hi Tim,

Fundamentally, I agree with you that banks as a group benefit enormously from the legal privilege extended to them by governments. However, I am not sure your assertion about the hiring of employees at banks has any basis in fact. As someone who sadly, works in the banking industry there are historically, considerable opportunities for employment for people of various backgrounds – and as profits increased the demand for people with specific skillsets (credit analysis for example) grew also. I have not experienced this “reluctance” you speak of. Do you have any research that demonstrates your argument?

Also, some areas of banking (i.e. trust and administration) make all of their revenue from fees. You suggest that vitually all of banks income derives from the legal privilege in respect of the net interest margin. What proportion of an average bank’s income comes from NIM versus fees?

Hi Robert.

“Do you have any research that demonstrates your argument?”

I just find it odd that financial services people earn so much and trying to think of why this might be. That banks are given a subsidy explains why the overall industry size is large, but not why the benefits of this are spread over a smaller number of people than in other industries. The fact that wages are so much higher in the financial services industry is I think evidence that there is a natural limit to the number of people required to do a given job. Normally where there are excess profits/wages, this results in more hiring. In this case it does not. Why not? The above argument cannot be proven, I’m just trying to puzzle as to why it might be so.

I see that banks do attempt to poach each others’ staff, but that the reputation of the “star” who is poached seems to matter more than sheer manpower.

You wrote: “What proportion of an average bank’s income comes from NIM versus fees?”

I’m not sure how much of profit comes from NIM vs other areas – it’s pretty hard to disaggregate from most banks. However, I would note that the fees you speak of are also likely distorted by central bank action as the value of the assets under management, which ultimately pay the fees in a wide variety of areas is also kept artificially high since they are priced off the market interest rate, which is kept too low by the central bank.