This article is the sixth in a nine-part series on credit.

The other great class of credit whose extinction is not to be trembled at, but instead warmly welcomed, is the otiose round of ‘pig on pork’ interbank (and inter-‘shadow’ bank) lending and borrowing. This is an activity which serves little useful purpose beyond the basic one of allowing a limited series of transfers from a depository with preternaturally cash rich clients and atypically few cash poor ones, so that it may fruitfully collaborate with a sister institution in the converse situation, to the shared benefit of all. Outside of this, for Bank A to lend to Bank B so that B can buy the paper issued by Bank C which then deposits the funds with Bank A, each hoping to extract a few basis points advantage from the deal in their turn, is a gross exercise of financial incest, needlessly tying up resources and capital, both.

In fact, if we look at the instance of Europe, the truth is that, for all the undoubted pain and dislocation being suffered as we transition from an unsustainable whirl to something (hopefully) more sober and well-proportioned, this has been exactly what has been taking place.

In the three-and-a-quarter years since Fannie, Freddie, Fuld and AIG FP exploded our mass delusion that we had reached the Land of Cockaigne simply by pooling, slicing, and layering in upon itself more and more debt, granted on easier and easier terms to worse and worse borrowers, European banks have actually increased their aggregate lending to households and private non-banks in the Zone by €760 billion and they have extended €350 billion more in credit to EZ governments (not an unmitigated benefit, this, of course). In marked contrast, they have reduced lending to one another by over €310 billion, withdrawing another €500 billion or so from non-Eurozone banks along the way. [There are, naturally, exceptions to this broad generalization, notably in Spain – where business lending is a hefty €100 billion below its April’09 peak. The point, nonetheless, remains a valid one].

None of this is to argue that the stresses are not very elevated, nor to pretend that the inevitable differences in the applied microstructure of such vast sums have not thrown up large numbers of winners and losers – whether deserving or undeserving – but it cannot be overlooked that with 35% of their total Eurozone assets consisting of exposures to one another (and 55% of the extra-EZ loans and non-equity securities on their balance sheets funding banks outside the single-currency area), they still have €11 trillion – some five times their combined capital – to go, if they are to shrink back to a less leveraged footing without doing more harm than is necessary to the world of work it is supposedly their primary purpose to serve.

Back in the day, arch Eurocrat, Jean-Claude Juncker, boasted that he and his fellow King Canutes vouched to ‘fully assure’ that no ‘systemically-important financial institution’ in their fiefdom would be ‘allowed to fail’ – the arrogant aside being that all the Zone’s 6,000-plus credit institutions fell into that category of NTBTF – No-one Too Bad To Fail.

Such an exercise in Hubris inevitably called forth the savage shade of Nemesis and so, three years and more later, we have reached a pass where hardly a single SIFI can assure its peers that it can be saved, nor its sovereign’s rating with it.

Accordingly, many observers point to Europe as making the case that the crisis has finally vindicated Keynes and delivered us, not just to the zero-bound, but to a veritable absolute zero of economics where the ability of money to have any effect has been completely frozen out.

But, far from Europe being the exception that proves the rule, so hopelessly have its drowning banks and foundering governments come to clutch at one another as they sink that much of the ECB’s present intervention – vast as it is – may not be a means of direct inflation, at all, and so cannot be deemed to have ‘failed’. You see, what is mostly afoot in Europe is that the national components of the system are simply being drawn into inserting themselves – providing a credit wrap if you will – between former correspondent banks in the different member states who have come to harbour unallayable suspicions about each other’s true standing and so will not deal directly with one another as was their wont.

If we imagine that, in the good old days, a Spanish house-buyer might have borrowed from his local bank to stock his house with shiny, new German, kitchen appliances, this would have led to their export manufacturer adding to his monetary holdings at a German bank, with this last being happy to ‘recycle’ this fraction of the Great Teutonic Current Account Surplus by lending it back to the original Iberian agent of inflation.

Nowadays, alas, such insouciant laissez passer has become unthinkable, forcing the Spanish lender to close the gap by repoing or selling some of its securities holdings to the Banca de Espana. The German creditor likewise prefers to place his funds on deposit with the Buba and the transmission is completed between the two via the TARGET system. ECB assets – and the portion involving government bonds – will thereby have risen without any new monetization of debt whatsoever having taken place.

To see some evidence of this putative exchange in action, note that the Bundesbank’s intra-ECSB exposures rose €360 billion in the three years after September’08, the Netherlands’ by €80 billion (the pair having put on another €90 billion between them in the following two months), while German bank claims on other EZ members declined €180 billion and Dutch ones by €35 billion. A further leakage was to be found in whatever part of their €245 billion combined cutback of exposures to EU banks outside the single currency it was which related to the three English clearers who access the system via the DNB.

On the other side of the ledger, the data show also that the ECB’s balance sheet waxed €540 billion fatter, (to which not insubstantial total the NCBs added another €910 billion during the period in question), by way of the acquiring – among other ‘assets’ – €250 billion in Euro area governments and €690 billion in claims on the region’s banks and offsetting this with €1,040 billion in deposits accepted from the MFIs in their turn.

To gain a sense of the scale of these numbers, we may note that, in the year to last November, the Buba’s TARGET balance rose to 20% of German GDP and the change was equivalent to 125% of the whole twelvemonth’s current account surplus. For the DNB, the comparables were 25% of GDP and 100% of the surplus – and lest us not forget that the Bank’s dealings with Lloyds, HSBC, and Standard Chartered may make that a low-ball estimate, given the net drain likely to result from the UK’s own deficits.

Now we come to the nub of the matter. Note that, in the 22 months from August’08 to June’10, Eurozone government net liabilities increased by around €1.150 trillion. Of that total, no less than €573 billion – pretty much a half! – was bought (monetized) by the MFIs (+€443bln) and the ECSB (+€130bln) between them. In that same stretch, EZ M1 expanded at a rip-roaring 12.6% annualized pace, or by €920 billion – so the fiscal deficit alone was responsible for five-eighths of this significant inflationary impulse.

From that point on, it was downhill all the way, however, and while the next year-and-a-half saw the central bank increase its rate of accumulation (+€151bln), MFIs were now trying to dump some of the toxic waste they had been previously seduced into warehousing, cutting their total by €119 bln to leave a picayune, combined addition of €31bln (again giving some credence to our ideas of a shift between monetizers occurring, rather than an outright intensification of their joint efforts).

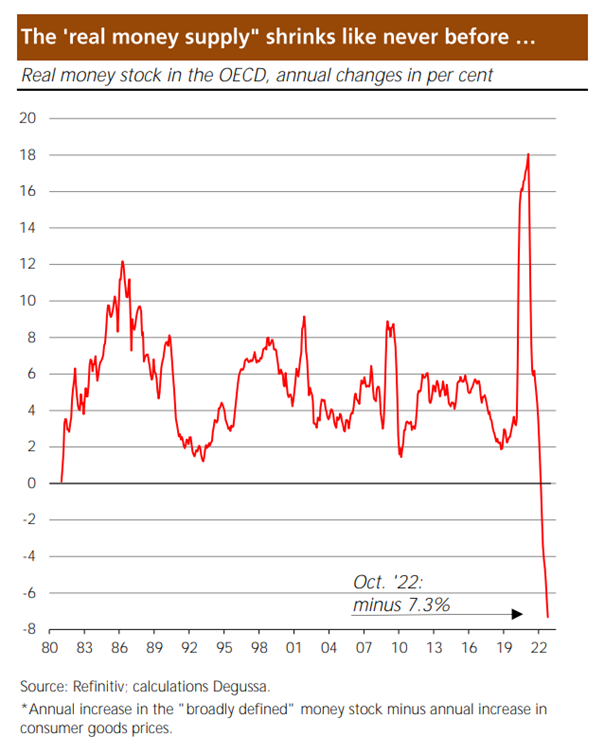

Guess what was the upshot? If you said money supply slowed to a recession-threatening stall, you qualify for a gold star. In contrast to the incipient Weimarian rush which went before it, M1 inched up by just €62bln, or less than 1% annualized – barely a twelfth of the increment per month which prevailed in the preceding spurt. Reversing from multi-year highs, this spurt just pipped the time-span to the LEH Crash itself to set a Euro-era record nadir for any like period.

Keeping in mind this direct, intuitive linkage, there is therefore no prima facie reason to bemoan the supposed inability of the modern, unanchored central bank to influence the money supply, no matter how firmly the course is set for a general retrenchment of borrowing: it simply needs to make up its mind to ruin the currency and act in a way which is consonant with its aims.

We re-iterate the point we have made over and over again throughout this episode, following the ideas of Leland Yeager: for as long as the national currency has not been totally repudiated by its habitual users, money does not have to be lent into existence, it can be spent into existence by the state. Should that state be temporarily indisposed – which may be the case in the ‘Zone – as our Lords and Masters at the central banks have gleefully discovered, they nonetheless enjoy a near unlimited scope to buy up existing, as well as newly-issued, non-money assets from the non-monetary sectors by writing cheques upon themselves and so, by this means can engineer any increase in demand deposits they wish – i.e., create as much new bank money as they will, even if it means they must nationalize the whole apparatus of finance along the way.

Thus, the issue is a matter of politics, not economics. As central banking insider par excellence, Charles Goodhart, aphoristically put it, long before the current turmoil erupted, ‘deflation is a policy choice’.