“Marketing is what you do when your product is no good.”

– Edwin Land.

Rosser Reeves was one of the most celebrated American advertising executives from the 50s onwards – he helped define the era of ‘Mad Men’. There’s a story about him, now many times retold; the version that Daniel H. Pink tells (in his book ‘To sell is human’) goes as follows. Reeves and a colleague were having lunch one day in Central Park. On their way back to Madison Avenue, they came across a beggar. The man was holding a cup for donations and a handwritten cardboard sign, that read:

I AM BLIND.

Sadly, the man’s cup was almost empty. His plight, for some reason, was not moving people to donate. Reeves immediately told his colleague that he could see what the problem was; he bet his colleague that he could dramatically increase the money in the beggar’s cup, simply by adding four words to his sign. His colleague, intrigued, took him up on the bet. Reeves then introduced himself to the man, explained that he was in advertising, and offered to change his sign slightly to increase people’s willingness to give. The man agreed. Reeves took out a pen, added his four words, and with his colleague stepped back to watch. Almost immediately, passers-by started to drop coins into the blind man’s cup. Others came by, began talking to the man, and took dollar bills from out of their wallets. Pretty soon, the man’s cup was overflowing with cash. What four words did Rosser Reeves add to the sign ?

IT IS SPRINGTIME AND

The new sign, that captured the sympathy and triggered the generosity of passers-by, read:

IT IS SPRINGTIME AND I AM BLIND.

By nudging people to put themselves in the position of the beggar, Reeves was exploiting something psychologists call “the contrast principle”. He was arguably “guilting” people into giving. But most observers would conclude that, assuming this story isn’t apocryphal, the end justified the means.

Asset gathering businesses don’t need to be as subtle when it comes to their own marketing. Given that the business of investing implicitly assumes the generation of positive returns, fund marketers can simply appeal to their customers’ self-interest. That said, as the author Guy Fraser-Sampson points out, people’s investment decisions are driven by emotion, not numbers, so expecting logical decision-making on the part of prospective customers may be a step too far. The rational investor is a myth.

Ben Graham wrote in 1934 about the bull market of the Roaring Twenties that met its fateful toreador in 1929:

“The notion that the desirability of a common stock was entirely independent of its price seems incredibly absurd. Yet the new-era theory led directly to this thesis. If a…stock was selling at 35 times its maximum recorded earnings, instead of 10 times its average earnings, which was the pre-boom standard, the conclusion to be drawn was not that the stock was now too high but merely that the standard of value had been raised. Instead of judging the market price by established standards of value, the new era based its standards of value upon the market price. Hence all upper limits disappeared, not only upon the price at which a stock could sell but even upon the price at which it would deserve to sell. This fantastic reasoning actually led to the purchase at $100 a share of common stocks earning $2.50 a share. The identical reasoning would support the purchase of these same shares at $200, at $1,000, or at any conceivable price.”

Walter Bagehot wrote that people are most credulous when they are most happy. Given that many stock (and bond) markets are now trading at record highs, we must assume that there are plenty of happy people out there. But as Lord Overstone also counselled:

“No warning can save people determined to grow suddenly rich.”

It is in the nature of people to extrapolate from the recent past. In the recent past, stocks have been a one-way bet. Such is life under a regime of limitless liquidity and zero percent interest rates (or even lower). As for bonds, there is probably not a trader still toiling in a dealing room who has experienced anything other than declining rates during the entire duration of their career. This is not an environment conducive to the future stability of asset prices.

Jason Zweig has written nicely of the stark differences between asset gathering firms and asset management firms. We highlighted them in January. We highlight them again today. Among the differences:

- “The marketing firm has a mad scientists’ lab to “incubate” new funds and kill them if they don’t work. The investment firm does not.

- The marketing firm charges a flat management fee, no matter how large its funds grow, and it keeps its expenses unacceptably high. The investment firm does not.

- The marketing firm refuses to close its funds to new investors no matter how large and unwieldy they get. The investment firm does not.

- The marketing firm hypes the track records of its tiniest funds, even though it knows their returns will shrink as the funds grow. The investment firm does not.

- The marketing firm creates new funds because they will sell, rather than because they are good investments. The investment firm does not.

- The marketing firm promotes its bond funds on their yield, it flashes “NUMBER ONE” for some time period in all its stock fund ads, and it uses mountain charts as steep as the Alps in all its promotional material. The investment firm does none of those things.

- The marketing firm pays its portfolio managers on the basis not just of their investment performance but also the assets and cash flow of the funds. The investment firm does not.

- The marketing firm is eager for its existing customers to pay any price, and bear any burden, so that an infinite number of new customers can be rounded up through the so-called mutual fund supermarkets. The investment firm sets limits.

- The marketing firm does little or nothing to warn its clients that markets do not always go up, that past performance is almost meaningless, and that the markets are riskiest precisely when they seem to be the safest. The investment firm tells its customers these things over and over and over again.

- The marketing firm simply wants to git while the gittin’ is good. The investment firm asks, “What would happen to every aspect of our operations if the markets fell by 67% tomorrow, and what would we do about it? What plans do we need in place to survive it?”

None of which is to denigrate either stock or bond markets in isolation – just expensivestock and bond markets. How do you tell when a stock market is expensive ? Well, John Hussman wrote at the beginning of March that

“Last week, the cyclically-adjusted P/E of the S&P 500 Index surpassed 27, versus a historical norm of just 15 prior to the late-1990’s market bubble. The S&P 500 price/revenue ratio surpassed 1.8, versus a pre-bubble norm of just 0.8. On a wide range of historically reliable measures (having a nearly 90% correlation with actual subsequentS&P 500 total returns), we estimate current valuations to be fully 118% above levels associated with historically normal subsequent returns in stocks. Advisory bullishness (Investors Intelligence) shot to 59.5%, compared with only 14.1% bears – one of the most lopsided sentiment extremes on record. The S&P 500 registered a record high after an advancing half-cycle since 2009 that is historically long-in-the-tooth and already exceeds the valuation peaks set at every cyclical extreme in history but 2000 on the S&P 500 (across all stocks, current median price/earnings, price/revenue and enterprise value/EBITDA multiples already exceed the 2000 extreme). Equally important, our measures of market internals and credit spreads, despite moderate improvement in recent weeks, continue to suggest a shift toward risk-aversion among investors. An environment of compressed risk premiums coupled with increasing risk-aversion is without question the most hostile set of features one can identify in the historical record.”

That sounds a little like the broad US market might be expensive. What about bonds ? Investors have historically bought bonds for two main reasons: capital preservation, and yield. At current prices and interest rates, many sovereign bond markets now offer neither. All the way out to seven years, German government bonds now offer negative yields to maturity. Investors who buy those bonds today are guaranteed to lose money if they hold to term. They will be paying a premium to par to earn a derisory annual coupon and they will only be paid par on redemption. That sounds a little like German government bonds, for example, might be expensive.

Only a cretin would be buying supposedly safe bonds (which clearly aren’t) with negative yields. Who is likely to be buying these bonds ? To paraphrase Die Hard villain Hans Gruber:

“You asked for miracles, Theo; I give you the ECB.”

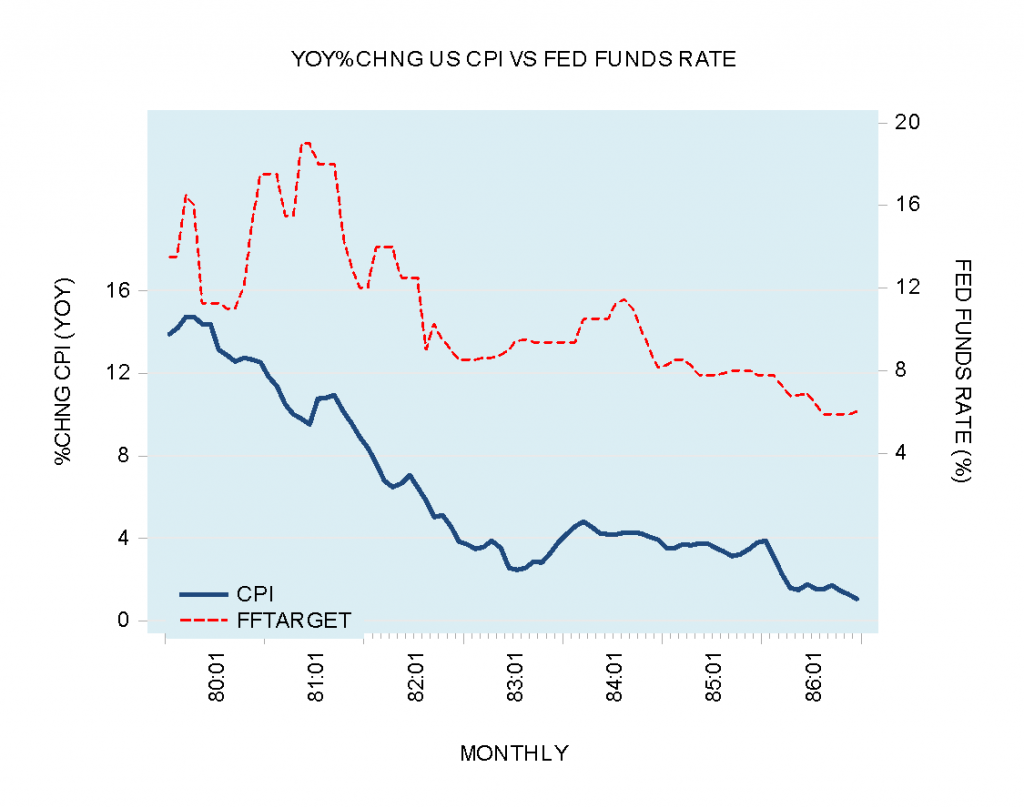

Dr Robert Gay of Fenwick Advisers, formerly a Senior Economist with the Board of Governors of the Fed during the chairmanship of Paul Volcker, suggests that there are three problems with Mario Draghi’s just-begun Quantitative Easing Programme at the ECB:

1) It’s too big – relative to the size of the euro zone economy.

2) It’s too late – with nominal yields already low, deflation already entrenched, and it’s unmatched with any fiscal stimulus.

3) It’s entirely ineffectual – it throws sand in the wheels of bank deleveraging by punitively paying negative interest on excess reserves; it hurts savers with negative deposit rates; there’s no direct transmission to the real economy; and it’s likely to postpone deleveraging by the large debtor countries of the euro zone (i.e. all of them).

Other than that, it’s an entirely sound plan with every chance of success.

Conclusions, given the above ?

- Avoid the major indices, both for stocks and bonds. Do not pursue cheap, broad market exposure – specialise.

- Seek selective, bottom-up, compelling value wherever it exists (hint: Asia, especially Japan).

- Give asset gathering firms an unusually wide berth.

- Ignore marketing that puts an emphasis on past performance. What matters most today is current valuation.

- Some of you may wish to pray.