As noted in my preceding column Dr. Paul Krugman’s reflections, as published in the UK Guardian at the end of 2012, Paul Krugman: Asimov’s Foundation novels grounded my economics, are of keen interest. Prof. Krugman there wrote, “I grew up wanting to be Hari Seldon, using my understanding of the mathematics of human behaviour to save civilisation.”

As noted, Nobel laureate Frederick Hayek, in his 1974 Nobel Prize Lecture, indicted such pretensions on the part of the economics profession of the era as the “Pretence of Knowledge.”

Hayek is not the only Nobel Economics Prize winner with something to say about matters which, boiled to their essence, are a tug of war between believers in mathematical modeling and believers in common sense. One also can cast this as a war between elitists (i.e believers in the ability of an elite to manage society’s affairs better than can the society itself) and populists (i.e. believers in the ability of society to manage its own affairs better than an elite can do so for it).

Prof. Robert Mundell in delivering his own Nobel Economics Prize lecture, in 1999, A Reconsideration of the Twentieth Century, started with a discussion, echoing Hayek, of “in the explosion of our science how in some respects we fall short.” Mundell then goes on to provide an erudite history of money, especially a history of the gold standard. Prof. Mundells’ speech is, in its way, a perfect contra to Keynes’s own Auri Sacra Fames (an argument for the superiority of “representative” money to “commodity” money) and to Krugman’s frequent, albeit sloppy and unconvincing, attacks the gold standard.

The classical gold standard appears to offend, deeply, Prof. Krugman’s pretensions. In the speech as delivered Prof. Mundell observed (around minute 9’30”) that the gold standard “did not require a great theoretical genius to run gold standards… It was automatic. All that mattered is that countries would export or import gold, they’d fix their currencies to gold, and their exports or imports automatically changed the money supply, and the changes in the money supply brought about changes in expenditure which brought balance of payments into equilibrium.”

As economic historian Prof. Brian Domitrovic, like Prof. Mundell a populist, has observed:

The idea that monetary policy takes the enormous exertions of immensely smart and credentialed people is mistaken. Good monetary policy by definition takes virtually no exertions by anybody. John Taylor’s monetary policy rule is 7th-grade algebra. The gold standard that supervised the second industrial revolution, 1871-1914, the greatest period in the economic history of the world, was “so simple a monkey could run it….”

The prepared text of Mundell’s Nobel lecture may be the most thoughtful brief recapitulation of the dynamics of the gold standard, and of the key axioms of monetary economics, in our era. Mundell observes:

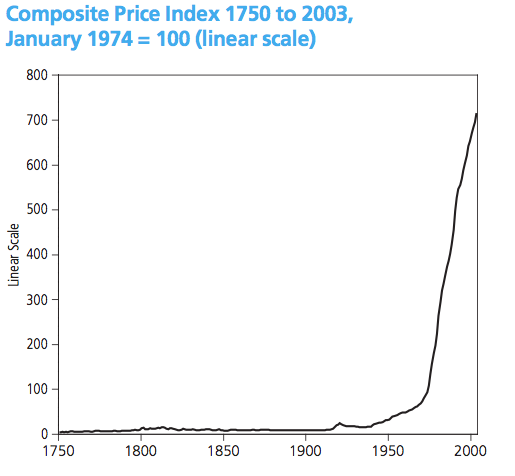

The international gold standard at the beginning of the 20th century operated smoothly to facilitate trade, payments and capital movements. Balance of payments were kept in equilibrium at fixed exchange rates by an adjustment mechanism that had a high degree of automaticity. The world price level may have been subject to long-terms trends but annual inflation or deflation rates were low, tended to cancel out, and preserve the value of money in the long run. The system gave the world a high degree of monetary integration and stability.

International monetary systems, however, are not static. They have to be consistent and evolve with the power configuration of the world economy. Gold, silver and bimetallic monetary standards had prospered best in a decentralized world where adjustment policies were automatic. But in the decades leading up to World War I, the central banks of the great powers had emerged as oligopolists in the system. The efficiency and stability of the gold standard came to be increasingly dependent on the discretionary policies of a few significant central banks. This tendency was magnified by an order of magnitude with the creation of the Federal Reserve System in the United States in 1913. The Federal Reserve Board, which ran the system, centralized the money power of an economy that had become three times larger than either of its nearest rivals, Britain and Germany. The story of the gold standard therefore became increasingly the story of the Federal Reserve System.

World War I made gold unstable. The instability began when deficit spending pushed the European belligerents off the gold standard, and gold came to the United States, where the newly-created Federal Reserve System monetized it, doubling the dollar price level and halving the real value of gold. The instability continued when, after the war, the Federal Reserve engineered a dramatic deflation in the recession of 1920-21, bringing the dollar (and gold) price level 60 percent of the way back toward the prewar equilibrium, a level at which the Federal Reserve kept it until 1929.

It was in this milieu that the rest of the world, led by Germany, Britain and France, returned to the gold standard. The problem was that, with world (dollar) prices still 40 percent above their prewar equilibrium, the real value of gold reserves and supplies was proportionately smaller. At the same time monetary gold was badly distributed, with half of it in the United States. In addition, uncertainty over exchange rates and reparations (which were fixed in gold) increased the demand for reserves. In the face of this situation would not the increased demand for gold brought about by a return to the gold standard bring on a deflation? A few economists, like Charles Rist of France, Ludwig von Mises of Austria and Gustav Cassel of Sweden, thought it would. …

Rist, Mises and Cassel proved to be right. Deflation was already in the air in the late 1920s with the fall in prices of agricultural products and raw materials. The Wall Street crash in 1929 was another symptom, and generalized deflation began in 1930.

In his recidivist attacks on the gold standard Prof. Krugman tediously resurrects and refutes straw man arguments drawn from marginal thinkers. Prof. Krugman sets his phaser on stun and points it at the ghost of Ayn Rand rather than tangling with at his peers. (A corollary, of which there appear none in the record, would be a neoclassical economist attacking Keynes by criticizing the novels of Danielle Steel.)

One might speculate that Prof. Krugman fears triggering the launch of a photon torpedo against him, one primed to evade his formidable deflector shields, by one of his intellectual peers. That said, Prof. Krugman’s introduction to theFoundation Trilogy perhaps reveals a deeper motive:

Now that I’m a social scientist myself, or at least as close to being one as we manage to get in these early days of human civilisation, what do I think of Asimov’s belief that we can, indeed, conquer that final frontier – that we can develop a social science that gives its acolytes a unique ability to understand and perhaps shape human destiny?

Well, on good days I do feel as if we’re making progress in that direction. And as an economist I’ve been having a fair number of such good days lately.

I know that sounds like a strange claim to make when the actual management of the economy has been a total disaster. But hey, Hari Seldon didn’t do his work by convincing the emperor to change his policies – he had to conceal his project under a false front and wait a thousand years for results.

“I’ve been having a fair number of good days lately?” Does sound, to me, “like a strange claim to make when the actual management of the economy has been a total disaster.” Prof. Krugman’s celebration of “a false front and wait a thousand years for results” is more appropriate to a pulp medium than to the policies for governing America.

In his Foundation Trilogy introduction Prof. Krugman seems to lay claim to having it both ways. He denigrates political science and sociology as “less developed” than economics: “[E]conomics is, after all, largely about greed, while other social sciences have to deal with more complex emotions.” Then Prof. Krugman stipulates: “If there eventually is a true, integrated social science, it will still be a science of complex, nonlinear systems – systems that are chaotic in the technical sense, and hence not susceptible to detailed long-run forecasts.” Well.

Why acknowledge repeated debacles, over the course of mere decades, when one is prepared to wait a thousand years for the results? Although it be uncharitable to say this, such a pose smacks more of faith than of science. Were Prof. Krugman not such an honored figure such a statement easily could be mistaken for a sort of fanaticism.

A Science Fiction Book Club copy of the Foundation Trilogy, autographed by Isaac Asimov, remains, less than half read, on my bookshelf. From Prof. Paul Krugman we learn that it was this very work that that would propel him beyond the twilight zone of the Neo-Keynesianism into an aspiration to emulate the mastermind behind an imagined galactic empire.

This has a certain grandeur. Still, I beg: have mercy on my bewilderment, Prof. Krugman. I cast my one little vote for common sense as the better approach by which to save civilization.

Originating at Forbes.com: http://www.forbes.com/sites/

The Almighty cheek of it! The assumption that I and my fellow are Krugman’s to guide and control. Words fail.