Statistics have become very misleading: in particular we are being badly misled into believing that the US is teetering on the edge of price deflation, because the US official rate of inflation is barely positive, a level that US bonds and therefore all other financial markets have priced in without accepting it is actually significantly higher.

There are two possible approaches to assessing the true rate of price inflation. You can either reverse all the tweaks government statisticians have implemented over the decades to reduce the apparent rate, or you can collect a statistically significant sample of price data independently and turn that into an index. John Williams of Shadowstats.com is well known for his work on the former approach, but until recently I was unaware that anyone was attempting the latter. That is until Simon Hunt of Simon Hunt Strategic Services drew my attention to the Chapwood Index, which deserves wider publicity.

This is from the website: “The Chapwood Index reflects the true cost-of-living increase in America. Updated and released twice a year, it reports the unadjusted actual cost and price fluctuation of the top 500 items on which Americans spend their after-tax dollars in the 50 largest cities in the nation.” It is, therefore, statistically significant, and it consistently shows price inflation to be much higher than that indicated by the Consumer Price Index (CPI).

The table below shows this difference since 2011, and how it affects real GDP.

Sources: Chapwood Index, US Bureau of Labor Statistics and Bureau of Economic Analysis. Figures may not total due to rounding.

The Chapwood number in the table is the simple arithmetic average of the 50 cities. The year-in, year-out 10% inflation rate is notable. Furthermore, Chapwood shows cumulative inflation rate as shown by the CPI for the four years to be understated by 39.9%, and using Chapwood numbers in place of the GDP deflator, real GDP has slumped a cumulative total of 21.4% over the four years.

No wonder the poor in America are suffering: when their wages and benefit increases have been aligned to the CPI, they have fallen nearly 40% in real terms over the last four years. The resulting decline in business on Main Street revealed by these figures explains why Wal-Mart are laying people off and closing stores, and why trade associations continually issue disappointing trading assessments.

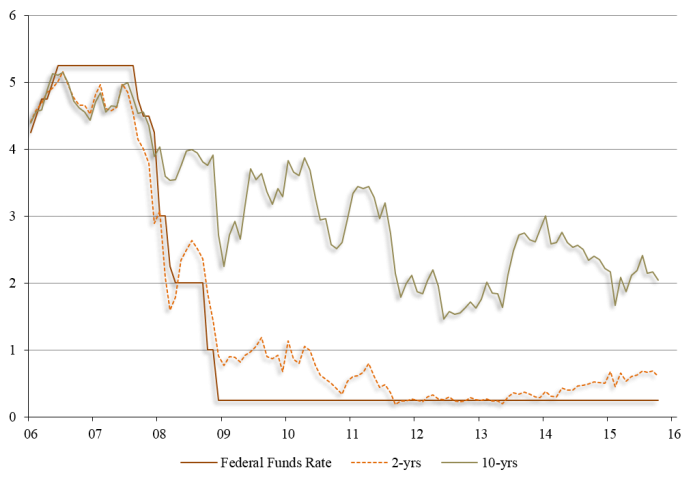

Understated price inflation fundamentally distorts everything that is macroeconomic, from monetary policy to economic commentary. It misleads central bankers into thinking they are missing their inflation targets when they are in fact exceeding them by a dangerously wide margin. It misleads analysts into thinking we are on the brink of a deflationary slump with prices maybe about to collapse. And most worryingly of all, bond markets have become more mispriced than even hardened bears realise, something that’s very likely to be corrected through a financial shock.

Just think of all those bonds that the banks have acquired as zero risk investments under Basel III rules 1. If bond markets discounted, as the Chapwood Index suggests they should, a US inflation rate consistently around 10%, the 10-year US Treasury bond should yield at least that, possibly more. The price would halve to meet those redemption yields, and lesser credit-worthy bonds would fall even more, a development for which all financial markets are wholly unprepared, not to mention the knock-on effects on stocks, derivatives and of course, mortgage rates.

1Basel III (or the Third Basel Accord) is a global, voluntary regulatory framework on bank capital adequacy, stress testing and market liquidity risk