Dr Fox gave his speech on honest money to the IEA last week. The video can also be viewed here: http://www.iea.org.uk/multimedia/video/rt-hon-liam-fox-on-honest-money

It is almost universally accepted that the first duty of government is the protection of its citizens. As a former Secretary of State for Defence I am only too aware of the external threats to the safety of our people and our country.

But there are other threats that I believe we have a right to be protected from – the debasement of our currency, the erosion of our earnings and the devaluation of our savings. I believe it is fundamentally wrong for governments to engage in structural profligacy, spending excessively across the economic cycle and passing ever larger amounts of debt onto future generations.

History is littered with examples of where economic failure led to compromised security. In my book, Rising Tides, I pointed out that by 1788, a year before the French Revolution, France was spending 62% of royal revenues on servicing its debt. The Ottoman Empire was spending 50% of its budget on debt interest payments by 1875 with the final repayment being made by the Republic of Turkey in 1954, even though the Empire had been abolished 36 years previously. The lessons from history are clear – if the destinations we wish to reach are security, prosperity, and honest money, then the road we must travel is that of fiscal restraint and monetary realism.

Today, I want to look at how close we are to those objectives, especially in the light of the great financial shock that came to the global economy following the events of 2008.

The policies of fiscal restraint imposed by the current government have seen our annual budget deficit fall from the terrifying heights of the 11.4% of GDP which we inherited from Labour in 2010, although at 5.7% of GDP it remains the third-highest in the EU.

As the U.K.’s national debt has grown from around £960 billion to over £1600 billion, so our debt interest has risen dramatically to around £50 billion per year, much more than we spend on our national defence and security. Despite the Chancellor’s drive for control over public spending, the job has been made more difficult by the government’s commitment to ring fence some of the largest areas of expenditure which has meant increased distortion in the shape of our spending patterns and priorities. The government should have our full support in what will have to be tough spending rounds in the years ahead if we are to meet our fiscal objectives.

We must, however, be clear that this is not a cyclical correction but a structural one and that we have passed, for all time, the high watermark of government spending as a share of our national income.

The financial crash of 2008 was one of the greatest warnings we have had about the interdependence we share in the era of globalisation and how quickly contagion in one part of the global economy will spread to the rest.

In medicine, we often say that the most useful instrument is a “retrospectoscope” but it is worth asking, even with the benefit of hindsight, whether we believe the response to the 2008 crash was the correct one? Even if we accept that a huge injection of liquidity at the start might have prevented the worst of the slump, which most would agree with but some would still dispute, what is the legacy that we have been left with? Even if we accept the best case, that extraordinary monetary and fiscal policy helped stave off the worst of the crisis, has enough thought been given to the causes of the crisis in the first place?

Specifically, have we ensured that we have changed the patterns of behaviour that were such a major contributory factor to the crash? Perhaps a little, but not to the extent that we should. What we have had on both sides of the Atlantic is more and more intended stimulus, the use of taxpayers’ money to featherbed the banks and a failure to fully address the remuneration system in which the temptation of short-term personal gain produced irresponsible risk-taking with other people’s money.

On top of this, a persistent low interest rate environment has boosted the stock market and created cheap capital that all too easily found its way into overseas adventurous investments, especially in real estate and commodities, at least until recent price downturns in these markets.

Back in 2011, Kevin Dowd, Martin Hutchinson and Gordon Kerr made a presentation to the 29th Cato Institute Annual Monetary Conference, entitled “The coming fiat money cataclysm – and after”. Beautifully understated! Every so often I read something that impresses me so greatly that it goes to a select pile at the side of my desk – and this was one such presentation. They argued that the US authorities had massively increased government intervention in the economy, before, but particularly in response to the crisis, and by doing so had produced a diminished ability of the financial system and the broader economy to correct themselves.

These policies “aggravated underlying moral hazards that were a major proximate cause of the crisis. They undermined accountability and generated massive transfers to those responsible for the crisis (who had already greatly enriched themselves in creating it) at the expense of everyone else. Even worse was the response of the political establishment, repeatedly bailing them out with taxpayer cash, with further bailouts likely to follow. This goes beyond mere cronyism and amounts to a takeover by the “banksters” of the political system itself.”

Simon Johnson, a former chief economist of the IMF went further in his criticism – “elite business interests—financiers, in the case of the U.S.—played a central role in creating the crisis, making ever-larger gambles, with the implicit backing of the government, until the inevitable collapse. More alarming, they are now using their influence to prevent precisely the sorts of reforms that are needed, and fast, to pull the economy out of its nosedive. The government seems helpless, or unwilling, to act against them.”

Most seem to agree that, even if the situation was not as bad in the UK as in the US, we were certainly beset with some disastrous management, RBS being an obvious example, where the perpetrators made off with huge financial rewards leaving management, shareholders and taxpayers to pick up their mess with impunity.

These critics argue, as many others do, that the response of the authorities to the problems of 2008 was part of a pattern, repeated over time. They argue that lower interest rates were responsible for one boom and bust cycle after another since the late 1990s yet the response of the Federal Reserve, in particular, was to lower interest rates again and create an even bigger bubble next time round. They also argue that this interest rate policy inevitably reduces savings and in the long run decapitalises the economy. These arguments deserve a good deal more scrutiny, and I believe credibility, than they frequently receive.

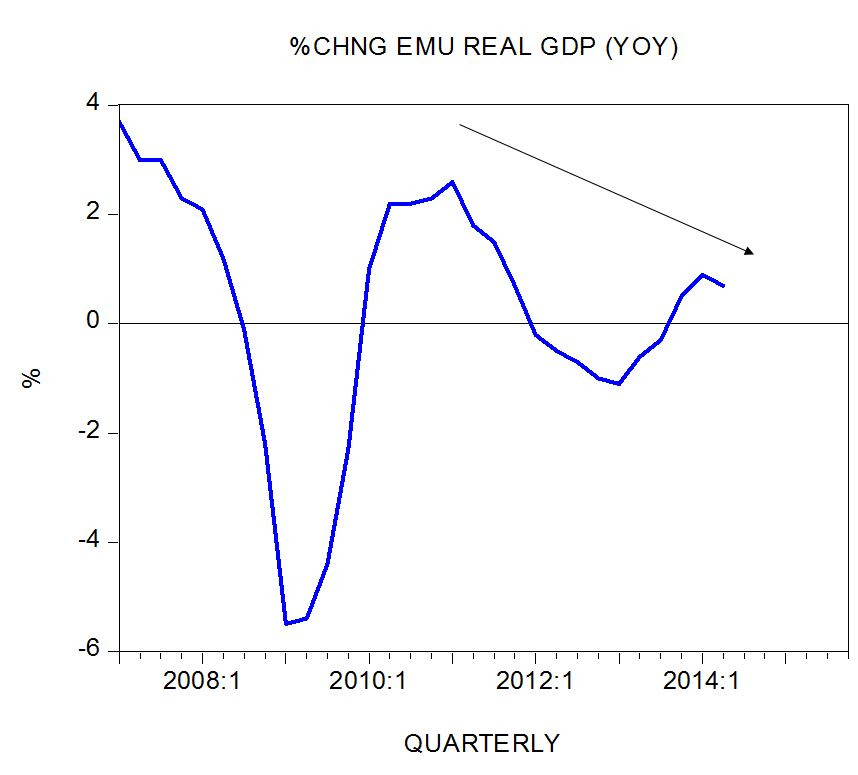

In the spring of 2009, the Bank of England introduced an emergency interest rate of 0.5% – the lowest rate in over 300 years. Over six years later, it remains exactly the same. Is this the longest economic emergency in our history, deserving of such prolonged divergence from financial orthodoxy or has it proved to an ineffective cure for our economic ills that we now find at a practical and political level, too difficult to unwind?

I want to look at what has happened since our emergency rates began, and perhaps more importantly, whether we might be repeating the behaviour that led to the crash in the first place.

Despite the lack of attention given to some critics, it is not as though distinguished commentators have been silent on the subject in the intervening period, although Liam Halligan regularly comments that many of them took their time!

Richard Dyson, of the Daily Telegraph, wrote in 2013, that there were a number of problems resulting from ultralow interest rates.

First, otherwise financially prudent young people were borrowing up to 95% of a property’s value, even though the mortgage rate could only go up, with all the implied accumulated financial problems for the future.

Second, cash rich depositors were turning to buy to let and purchasing rental properties, despite having no real desire to be landlords because the returns on savings were so poor.

Third, otherwise risk-averse savers were turning to new, potentially dangerous investments such as retail bonds (lending directly to companies) or peer-to-peer lending (lending to strangers over the Internet). The problem was simply that savers were unable to get the same yields anywhere else.

Ros Altman, (now pensions minister, Baroness Altman) wrote in the Guardian, earlier in 2015, that although the emergency interest rate may have initially avoided catastrophic deflation, the policy had since failed to stimulate consumption across the whole economy in the way that the government had hoped.

Perhaps more importantly than the failure to stimulate consumption, she wrote, was the effect on savings and pensions with pensioners seeing their annuity incomes fall as interest was squeezed.

Additionally, companies had had to pour billions of pounds into making up the deficit in their employees pensions rather than reinvesting it and stimulatingly recovery. On top of this, while low official rates have lowered mortgage rates, the cost of borrowing in other ways, such as loans, credit cards and overdrafts has risen as lenders have sought to increase their margins to remain profitable.

The cost of these types of borrowing is now above 2008/9 levels. In other words, the transmission mechanism from low interest rates to increase consumption and economic growth is broken.

Finally, Merryn Somerset Webb, editor-in-chief of Money Week, writing in the FT in August 2015, wrote that low interest rates and cheap money are encouraging capital misallocation.

Companies are borrowing large sums of money but do not use it to expand or invest in R&D. Instead, they are pouring money into dubious investments. Since the crash of 2008, global corporate debt has more than doubled from 26% to 56% of GDP, according to McKinsey. When this driver to behaviour is combined with the increasing belief that governments will be there to provide bailouts, the ability to play fast and loose with other people’s money, and potentially avoid the consequences, is all too real – precisely one of the types of behaviour that led us into the 2008 crash in the first place.

Of course, there are those who believe that the addiction to monetary creation itself is a problem. In his informative and extremely readable book, “Paper Money Collapse: the folly of elastic money and the coming monetary breakdown”, Detlev Schlicter wrote “it is apparent that most commentators, politicians, and central bankers do not want to give up the comforting belief that the government can always fix the economy with injections of more money. This means that ever more money needs to be ejected, to buy the system time and to manufacture another round of money induced and thus temporary growth.”

He continued, “we have already reached a point at which ever more extreme measures are being taken. Over the 2 ½ years following the collapse of Lehman Bros, the Fed expanded the part of the money supply, that it controls directly – the monetary base – by more than $1.5 trillion, thus creating almost twice the amount of money of this type that the Fed had created, in aggregate, up to this point since its inception in 1913”.

And what has happened to the Feds M2 measure since then? It has risen from $7.498 trillion in January 2008 to just over $12 trillion by August 2015. Similarly, the Bank of England’s increase has been from £1.045 billion in January 2008 to £1,549 billion in August 2015. UK base money supply has quadrupled since 2009 as % of GDP. US base money supply has tripled.

Those who take a Hayekian view, those of the Austrian school, would argue that money creation in our present system is simply carried out for political goals. Injections of new money always change economic processes and, in modern economies, these injections of money happen almost continuously. This process has reached its zenith in recent years. If we believe that deflation is most likely to occur when an economy is imbalanced by excessive levels of debt and inflated asset prices, then we should be attempting to rein-in the supply of credit. Instead, we seem to be doing precisely the reverse: we are blowing bubbles rather than preventing them.

Two questions which immediately spring to mind are, firstly, whether or not QE has actually worked, and secondly what the current policy approach tells us about the relationship of our central banks to government. Recently there has been an increasing chorus questioning whether QE has actually brought tangible benefits to the real economy. A growing number of bankers and economists have openly begun to question whether having lower long run government interest rates actually feeds through to some key parts of the economy, especially small businesses.

Large companies are able to borrow in the bond market but small companies, on whom long-term economic viability depends, can face cripplingly high borrowing costs. Critics also point to research done by the Bank of England itself which suggests that QE has boosted asset prices and household financial wealth, which is “heavily skewed with the top 5% of households holding 40% of these assets”.

This has all brought a renewed focus on the relationship between central banks and central government –and rightly so. When state policy is assumed to be having such large economic and distributional consequences, what is surprising is that more scrutiny has not been applied to central bank actions. The government has a major say in the appointment of Bank officials and the regulatory environment in which the bank functions.

Since governments, especially those who are spending far more than they raise in revenue, have an interest in low borrowing costs, there is an added incentive for the central bank to keep interest rates down. In essence, central banks have become the government’s lender of first resort and, however independent they remain on the surface, will always keep their obligation to have the government adequately financed top of their agenda. It is not just that facilitating public finance is a key task of central banks, but history suggests that it is always the pre-eminent concern when push comes to shove.

Supposedly, the lender of last resort is defined as “the discretionary provision of liquidity to a financial institution, or the market as a whole, by the central bank in reaction to an adverse shock which causes an abnormal increase in demand for liquidity which cannot be met by an alternative source”.

Many would argue that classical financial doctrine would suggest that this concept should be applied to only a single distressed financial institution, only if it is solvent and then at penal rates of interest on first-class security.

Yet increasingly, critics claim that central banks are attempting to bail out large parts of the financial system, even elements that are clearly insolvent, and all at below market interest rates against the flimsiest collateral.

In the presentation to the Cato Institute, Kevin Dowd and his colleagues gave a wonderful historical perspective, quoting President Andrew Jackson, whose presidency was characterised by his personal crusade against the concept of a central bank.

As many of you will know his arguments held sway until the Civil War when interventionism led to the forces that would create the Federal Reserve in 1913. In 1836, writing about the Second Bank of the United States, a predecessor of the Fed, he said that

“the immense capital and peculiar privileges bestowed upon it enabled it to exercise despotic sway upon the other banks in every part of the country. From its superior strength it could seriously injure, if not destroy, the business of any one of them which might encourage its resentment; and it openly claimed for itself the power of regulating the currency throughout the United States… The other banking institutions were sensible of its strength and soon became its obedient instruments…… In the hands of this formidable power, thus perfectly organised, was also placed unlimited dominion over the amount of the circulating medium, giving it the power to regulate the value of property and the fruits of labour in every quarter of the Union and to bestow prosperity or bring ruin upon any city or section of the country as might best comport with its own interest or policy”.

Today, almost 200 years later, there are still legitimate, and perhaps even greater arguments to be had about the power and powers of the central banks, how independent they really are and whether targets, such as the 2% inflation rate target that guides Bank of England policy are appropriate at all times and in all financial circumstances. It would be to the general good of our political discourse and our financial approach to consider these arguments further. This is not to question the concept of independence of central banks, as the left would love to do, but to ensure that this independence is real and not a mirage.

The final point I wish to raise today is whether, in the midst of all these uncertainties, we are setting the correct metrics by which we measure our economic performance, in particular, whether we are sufficiently geared to the concept of wealth creation.

We have long been fixated on the concept of GDP growth as the determinant of economic success, particularly in the political arena. It is taken as read that a good GDP number is, in itself, a sign of economic success while a drop is immediately an excuse for political finger-pointing.

Of course, we would much rather be living in an economy with a growing GDP, yet, as I and many others have often said, there is a difference between GDP and wealth creation and it is the latter that ultimately determines our national prosperity.

We create wealth when we take an individual’s ideas, their unique IP, and turn it into a good or a service for someone else to buy.

Consider the Keynesian idea of burying £5 notes in bottles in mineshafts and having the private sector dig them up, or

Krugman’s proposal to stage a fake alien invasion to boost anti-alien defence spending.

Both would boost GDP but neither would add anything to worthwhile economic activity. So, are there other, better, ways to measure whether our policies are conducive to wealth creation itself? I suggest there is. If we take total government expenditure out of our GDP calculations then the resulting measure, GPP or Gross private product, gives us a much better idea of worthwhile economic activity.

In order to get a British perspective on this I decided to take a look at the relationship between GPP and GDP over recent decades. The pattern is extremely interesting and, I believe, largely predictable. How easy would it be to look at these figures and, from them, predict which political party was in power?

If we construct a ratio between the annual percentage growth of GDP and GPP for the past 35 years, then it becomes surprisingly easy to predict who was running the economy. Since 1979, the Conservative Party has been in office for 23 years. Despite steering Britain through two recessions and inheriting the financial disaster of the 2008 crash, under Conservative management GPP grew at a faster rate than GDP for 19 of those 23 years.

By contrast, of the 13 years that Labour was in power between 1997 and 2010, 11 of them are characterised either by stagnation or contraction in the percentage of growth that originated in the private sector. In other words, Labour achieved their growth rates by pumping public money into the economy, with the net effect of crowding out the private sector wealth generation.

We can also see the alternative – how the private sector is able to grow when it is given the space. The only surprise to me is that anyone would be surprised at all.

I am not an economist, but I am a stakeholder – a taxpayer, a mortgage holder and a saver. If not a policymaker, I am, as a parliamentarian, a policy scrutineer. In none of these roles, am I content with what I see. The current British government is making a valiant attempt to reduce our deficit with the aim of eventually creating the surplus required to reduce our debt and with it the burden of debt interest which makes the reduction of the deficit itself all the more politically difficult.

Yet, what if the fear of rising rates and the impact on short-term political fortunes are holding us back from decisions that might actually improve our chances of economic success and with it, the revenues that will help close the deficit gap without the need for future tax rises or even deeper spending cuts? What if, in terms of interest rates, we have got ourselves in the “pusher and addict” relationship?

What if, addicted to the drug of cheap money, policymakers, especially central bankers are unwilling to cause pain for their political masters with a population and electorate (or at least a part of them) hooked on cheap credit.

And politically, this is without even considering the lunatic ideas of the current socialist resurgence in the British Labour Party that would create a whole new wave of excessive monetary expansionism. Their so-called People’s QE would be better termed an economic RIP.

So what am I suggesting? In short, I believe we need to see a rise in interest rates as soon as possible, – I would personally like to see base rate rise by half a percent to put the Bank on the front foot – and for them to remain at levels more appropriate to a properly functioning capitalist economy.

Only in this way can we rebalance the economy between borrowers and savers.

An economy entirely geared towards borrowers, which is seen in some quarters as politically expedient, will not only become imbalanced, but will have a higher price to be paid in terms of increasingly angry savers the longer a decision on interest rates is put off.

Also, we need to stop the mindset in which cheap capital can be used as a gambling tool at the expense of the long term and prudent. Not only is this sending the wrong signals about economic behaviour but it risks the twin perils of underinvestment at home with the export of capability abroad, undermining our own competitiveness over time.

We also need to avoid the scenario where, in the case of a further global slowdown, policymakers have no short-term options. If we continue on our current trajectory of ultra-cheap credit and maxing out QE, then, should an economic slowdown arrive, as it will at some point, then policymakers would be no better than rollercoaster riders, without seatbelts, holding their hands in the air.

The current government is absolutely correct in its resolve to achieve fiscal consolidation and the Chancellor must continue to confront those who claim to share this end but continually challenge his means of achieving it. Many economists argue that it simply suffices to get the debt-to-GDP ratio on a downward path by running modest deficits.

Fortunately, the government has learned the most important lesson from the last crisis, that assuming growth will always continue unabated and that we will not be hit by adverse shocks in the future is not a good base for policy. As I often say, in relation to foreign and security policy, wishful thinking is a poor substitute for critical analysis. Of course, we have yet to confront the much longer term drivers of debt for the government: the unsustainable promises made to future generations on health and pensions, with an ageing population and all that this implies. These fiscal headwinds we know are coming down the track and will require us to have a fundamental rethink about how, as a nation, we are able to provide the pensions and healthcare the public expect.

For all the action we have seen on the fiscal front, therefore, longer term challenges await but thankfully we have time to think about and to deal with those. Today, my focus has been overwhelmingly on the potentially unforeseen consequences of monetary policy and whether, in fact, current policy is damaging our prospects. Our current approach is designed to deal with the bust. The real challenge is to create a system that does not encourage the boom in the first place.

For a non economist this is a brilliant essay.

AND I am proud to say that ALL of these issues can be addressed by readers /policy makers of my forthcoming book.

I am also glad to say that there are a few people ear the top who are reading the drafts.

Would anyone like to join them?

Send me your email address to get a copy.

The front cover reads:

A Tract on Financial Stability

By Edward C D Ingram

A science-based approach to the elusive quest for financial stability across the board. Based upon long accepted norms and principles, and two key observations made by John Maynard Keynes, this tract is a follow-on to his landmark paper ‘A Tract on Monetary Policy’, first published in 1923. It is thought by many academics and others to be on a level with Keynes’ own tract in terms of its potential long term influence.

The key point that Keynes observed was to quote two of the things he wrote right up front in his Tract on Monetary Policy are:

“If the value of money halves in such a way that a person both earns twice as much and spends twice as much on the purchase of the same things, then he is basically unaffected.”

In his Tract, Keynes also wrote that this is not what happens when the value of money halves. The distribution [of effects] is not uniform and the result is that it “affects different classes unequally, transfers wealth from one to another, bestows affluence here and embarrassment there, and redistributes Fortune’s favours so as to frustrate design and disappoint expectations.”

Keynes jumped the wrong way – to managing the dog that leads the economy – monetary policy instead of tackling the tail that is wagging the dog – the way that financial framework works.

And he got that wrong as well.

Too much credit and too little printed (permanent) money is just not a good idea.

Managing prices (interest rates) is not the dog, it is the tail.