On Wednesday December 16 2015 Federal Reserve Bank policy makers raised the federal funds rate target by 0.25% to 0.5% for the first time since December 2008. There is the possibility that the target could be lifted gradually to 1.25% by December next year.

Fed policy makers have justified this increase on the view that the economy is strong enough and can stand on its own feet. “The Committee judges that there has been considerable improvement in labor market conditions this year, and it is reasonably confident the inflation will rise over the medium term to its 2 percent objective”, the Fed said in its policy statement.

Various key economic indicators such as industrial production don’t support this optimism. The yearly growth rate of production fell to minus 1.2% in November versus 4.5% in November last year.According to our model the yearly growth rate could fall to minus 3.4% by August.

Although the yearly growth rate of the CPI rose to 0.5% in November from 0.2% in October according to our model the CPI growth rate is likely to visibly weaken.

The yearly growth rate is forecast to fall to minus 0.1% by April before stabilizing at 0.1% by December next year.

So from this perspective Fed policy makers did not have much of a case to tighten their stance.

Fed policy makers seem to be of the view that the almost zero federal funds rate and their massive monetary pumping has cured the economy, which now seems to be approaching a path of stable economic growth and price stability, so it is held.

On this way of thinking the role of monetary policy is to make sure that the economy is kept at the “correct path” over time.

Deviations from the “correct path”, it is held, occur on account of various shocks, which are often seen as of a mysterious nature. We suggest that the present Fed is following the footpath of Greenspan’s Fed, which was instrumental in setting in motion the 2008 economic crisis.

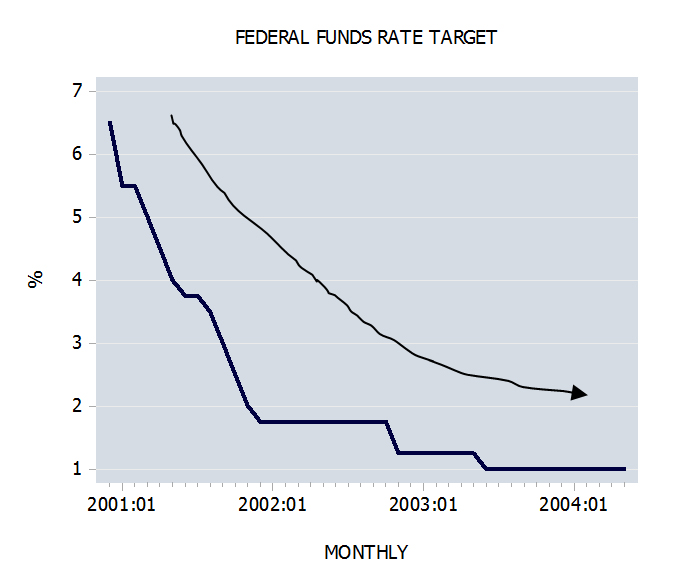

We hold that an important factor behind the 2008 economic crisis was the previous loose monetary stance of the Fed, headed at the time by Alan Greenspan. The federal funds rate target was lowered from 6.5% in December 2000 to 1% by May 2004.

This massive lowering of interest rates was instrumental in triggering the economic boom that followed suit, in particular in the property market.

Also, then Fed policy makers were arguing that the aggressive lowering of interest rates was necessary to stabilize the economy i.e. to bring it on the “right path”.

By June 2004 Fed policy makers have reached the conclusion that the economy doesn’t require more help from the Fed and can stand on its own feet. Consequently, the central bank has lifted the federal funds rate target by 0.25% by June 2004 to 1.25%. The Fed adopted a policy of a gradual tightening of interest rates until June 2006. Note that by June 2006 the target was set at 5.25% and kept at that level until August 2007.

The Fed’s view at the time was that a gradual tightening (each time by 0.25%) of the interest rate stance would prevent the unnecessary disruptions and would permit Fed policy makers to navigate the economy more accurately towards a path of stable economic growth and stable prices. The economic crisis of 2008 shattered all that.

We suggest that interest rate manipulations by the Fed cannot bring the economy onto a path of stability and prosperity but on the contrary sets in motion the menace of the boom- bust cycles.

By means of an artificial lowering of interest rates the central bank gives rise to various activities that cannot support themselves without the easy monetary stance of the central bank.

The lower interest rate stance, which is also accompanied by increases in the money supply growth, sets in motion the diversion of real wealth from wealth generators to various non productive or bubble activities. (These activities cannot support themselves and couldn’t have emerged in a free market environment).

The emerging economic boom, which is falsely labeled as an economic prosperity, leads to the weakening of the wealth generation process.

At some stage the central bank, which follows various economic indicators to justify interest rate manipulations, reaches the conclusion that the economy is starting to deviate from the “correct path”.

Consequently the loose interest rate stance is reversed. This begins to undermine the survival of various bubble activities – an economic bust ensues.

The magnitude of the bust is influenced by the extent of the previous loose monetary stance and by the state of the pool of real wealth. (Note that what permits economic growth is the pool of real wealth which funds economic activities).

Now, if the pool of real wealth is stagnating or shrinking then regardless of the Fed’s policy the economy couldn’t show a general economic growth.

A tighter interest rate stance coupled with a shrinking pool of real wealth will not only undermine bubble activities but also good activities, which couldn’t be introduced on account of the lack of real funding.

As time goes by though a tighter stance will eliminate bubble activities and will leave more real wealth at the disposal of wealth generators and will permit the introduction of various wealth generating activities.

We surmise that the prolonged low interest rate policy of the Fed, on top of the previous Fed’s loose monetary policies (during Greenspan’s era), has severely weakened the pool of real wealth, which could be currently in a dire state.

This raises the likelihood that the elimination of bubbles as a result of a tighter stance whilst good in the long term for wealth generators is likely to trigger a severe economic slump in the near to medium term.

Summary and conclusion

We suggest that the present Fed is following the footpath of Greenspan’s Fed, which was instrumental in setting in motion the 2008 economic crisis.

We surmise that the prolonged low interest rate policy of the Fed, on top of the previous Fed’s loose monetary policies (during Greenspan’s era), has severely weakened the pool of real wealth, which could be currently in a dire state.

This raises the likelihood that the elimination of bubbles as a result of a tighter stance whilst good in the long term for wealth generators is likely to trigger an economic bust in the near to medium term.