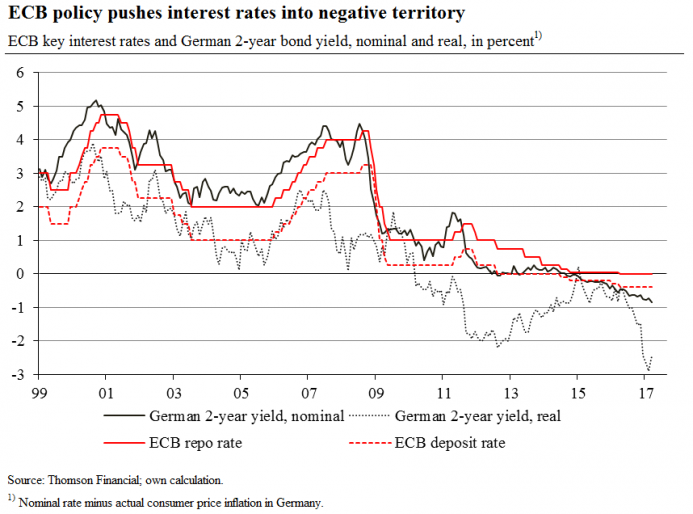

The violent exchange-rate fluctuations in pound sterling raise a host of issues that are causes for concern. Increased inflation is one of the primary concerns since this will eat away into the peoples’ real purchasing power and the real value of debt (personal, corporate and sovereign); the Bank of England reacted in a way that signaled their anxiety (through expanding QE and cutting the interest rate further) and, though these measures are well-intentioned, they will likely work to inadvertently further exacerbate the fallout from a catastrophic financial crisis (which many have argued is long overdue). This stark concern regarding inflation for institutions is further exemplified most obviously by pension funds’ demands for inflation-linked bonds. However, one can wonder whether the situation would have been significantly different had we lived in a truly free market with Free Banking (where agents of all varieties have a genuine choice of trading in multiple monies and where imposed institutional factors do not de facto privilege certain monies over others for various purposes)?

In a Free Banking regime, even as the pound dropped in value, agents would have the ability to switch (whether that be pre-emptively or after the fact) to monies that they had more confidence in – currently, most peoples around the world are essentially forced to live economic life according to the imposed expectations-management preference profiles of governments. That means that all peoples are subjected to and are at the mercy of increasingly restricted financial markets even when these speculations and/or (dis)investments are unjustified.

In a Free Banking regime, although some would still choose to stick with GBP for practical reasons, many would choose to reallocate and optimise their currency portfolios accordingly and, therefore, help mitigate the detrimental consequences associated with inflation and (geopolitical) uncertainty more broadly. This would, furthermore, ensure that people have greater incentive to become educated about the financial markets and system more generally which would help tackle the information asymmetries that led to the previous financial crisis (which we continue to suffer from, to this day). With multiple monies, there would be multiple exchange rates, interest rates, various commodities backing those differing monies, and so on. This allows agents to optimise their expectations-management preferences accordingly.

Nevertheless, even though governments and public perception may be largely averse to Free Banking (despite their misunderstanding and misreading of the term), the benefits of the choice of monies as opposed to a monetary monopoly cannot be understated and it may be that, initially, pragmatic liberalisations are needed with the end goal of genuine, authentic Free Banking. Introducing public-private partnership monies is one way in which to do this to improve investment, stimulate trade, obtain credit market benefits and alleviate unemployment both in the UK and with its trading partners.

In any case, Britain (and the world more broadly) would be able to reduce this dimension of uncertainty and turmoil after political events (political risks having been present throughout history and which, for the foreseeable future, will continue to play a crucial role) if there was a truly Free Banking system in place and it is still not too late for such policies to be announced and developed since Free(r) Banking systems are increasingly seen as serious contenders in the ongoing, heated debate for significant, much-needed monetary reform.

Why on Earth does free banking “help mitigate the detrimental consequences associated with inflation..”? The basic unit of currency under free banking is exactly the same as it is under the existing system, i.e. a pound, dollar, or whatever. So if pounds or dollars lose value, those with money in “free banking banks” lose out just like those with money in conventional banks.

Of course if you want to broaden the definition of money from “a liability of a bank” to a “liability of any other corporation”, then people are free to buy those liabilities under the existing system. E.g. I can buy bonds in any one of hundreds of stock exchange quoted corporations, or I can buy shares in those corporations.