“There’s always something to do.”

- The late Peter Cundill, philanthropist and value investor.

A happy new year to all readers !

Having entered the capital markets in 1991, it always felt like having just missed out on some giant party, or a little like having suddenly arrived at a wake. (One didn’t realise at the time that the “something” that had died was the Japanese stock market, and that it would take a quarter-century to be reanimated.) The one consistent aspect of the financial culture for the past 25 years or so has been the stubborn resistance of the stockbrokerage firm to respond to the messages of the marketplace telling it to die. In 1998, the journalist and author Michael Lewis wrote a column for Bloomberg entitled The slow death of the Anglo-Saxon stockbroker which started thus:

When historians of everyday life look back on 20th-century American capitalism they will be astonished by the role played by our stockbrokers. Certainly, it will be hard for them to explain to their readers the willingness of a prosperous American to hand his life savings over to a more or less perfect stranger in the mistaken belief that a) their interests are identical and b) the stranger has some special insight into the stock market. The reader will regard us with the same awe that we now regard those brave and seemingly mad souls who rode in wagon trains and fought Indians simply to get to California.

Lewis’ dry wit manages to obscure the dark truth at the heart of his observation. This dark truth, often glimpsed dimly if at all, by customers as well as financial providers, is that the real value added by most practitioners of financial services is dubious at best. Many who toil in the financial services arena have been one step away from creative destruction for their entire career. The launch of MIFID II – seven years in the making and running to over 1.4 million paragraphs of rules – is likely to drive even more of a wedge between ever-larger asset gathering rent-seekers and the boutique players who do actually manage to bring something to the party.

This writer remembers very distinctly the day in the 1990s on which the market capitalisation of Merrill Lynch – his then employer – with its “thundering herd” of 13,000 stockbrokers stateside was overtaken by the market capitalisation of Charles Schwab, the leading discount broker of the time. You could practically hear the grinding of the market’s tectonic plates. What the ubiquity of the Internet has brought in its wake has not abated, as this piece for Bloomberg Businessweek makes clear.

The future of fund management ?

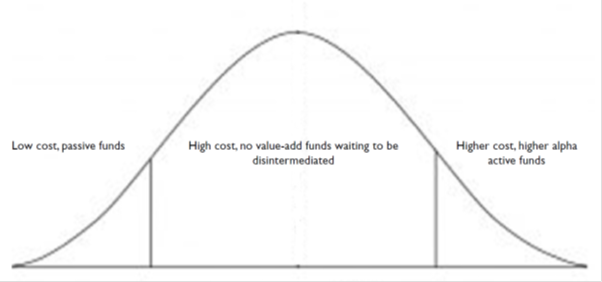

We suggested last year that the future of fund management could well be represented by the bell curve above. On the left of the bell curve are those passive providers that, by offering broad market exposure at the cheapest possible price, are eating just about everybody else’s lunch. There is a word for them: Vanguard.

Not every investor, of course, is content with “merely” the market return. Some investors, and we think notably high net worth investors, will wish to adopt a capital preservation mindset consistent with the avoidance of overly expensive markets representing an unacceptably high risk to their capital. Other investors, some of them again high net worth investors, being tolerant of risk, will seek to outperform the market. Those investors will, or should be, well served by high quality providers at the right hand side of the bell curve.

This leaves a large and awkward rump around the middle. We’ve uncharitably though probably correctly described them as “high cost, no value-add funds waiting to be disintermediated”. This is where the financial services wars of the years to come will be fought and, in most cases, lost.

Whatever else MIFID II achieves, it is destined to make life more difficult for research analysts, smaller players in the financial markets, boutique investment banks and fund managers, stock exchanges within the EU, and small to medium sized businesses full stop. One doubts whether that is exactly what the EU originally wanted, but given the nature of the biggest lobbyists for the UK to remain in the EU, perhaps it is exactly what the EU originally wanted.

Either way, McKinsey expect banks on the back of MIFID II to trim research costs to the tune of $1.2 billion or so. (As fund managers, we ourselves have never paid for research, on the quaint grounds that we think our clients pay us to conduct that activity ourselves, and we certainly don’t intend to start paying for it now.) A smaller research budget means less capital to support smaller and micro-cap businesses, an area of the market where dealing costs are now likely to rise, not fall, making the raising of new capital for new enterprises far more difficult. Well done, EU.

But as Peter Cundill pointed out, there’s always something to do. More to the point, there’s always value to be found somewhere in the world. The perversity of the rise of low cost index-trackers is that their very success in asset gathering compels the creation of value opportunities for those (by definition, smaller) fund managers not constrained by benchmarks. To us that includes smaller and mid-cap companies largely untouched by ETF adventuring and by Wall Street research analysts, and also entire markets – like Vietnam – with tremendous valuations and growth prospects, but which happen to not yet enjoy membership of the major developed market indices. All the more money on the table for the rest of us. By the time the industry’s lumbering giants have woken up to the story, the easy money will have been made.

It’s difficult not to see MIFID II as the creation of a bureaucratic, anti-competitive monster driving out the little guy and sharing the spoils amongst its rent-seeking, anti-competitive paymasters. But it partly depends on which side of the bell curve you want to end up. We suspect many of the presumed winners from MIFID will end up right in the middle of the road. And if their lowest common denominator juggernaut competitors don’t drive right over them, perhaps new digital technologies will.