The parallels between the last few years and those at the end of the 1990’s are striking. There was a few years ago the monetary intrusion of the “rising dollar” which at its worst seriously depressed the global economy. Oil prices crashed, as did several key currencies, and deflationary pressures that often accompany a significant downturn were manifest.

Starting in 1997, there was all of that, too. Oil prices though much lower to begin with were crushed, overseas the “dollar” “rose”, and currency problems were everywhere particularly in Asia (Japan both times, China only the later). And there were asset bubbles in both.

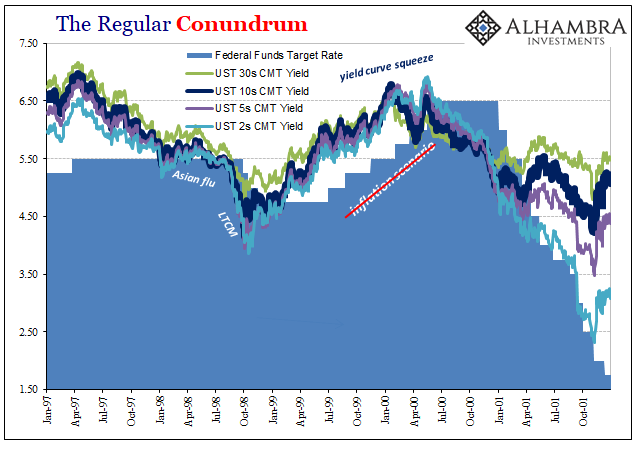

In terms of consumer price inflation, the similarities did not end. In 1999, the Federal Reserve having failed to account for the reasons behind the Asian flu began to act in anticipation of rising inflation. Ignoring bond market warnings, as Economists always do, the Fed took the excuse of oil price effects and their impacts on consumer price indices as justification.

Raising rates throughout 1999 and 2000, the central bank was eventually stopped by the collapse of the dot-com bubble and the deflationary pressures of recession as well as finance it did not foresee even though the bond market had been trading against them all along. Inflation, as a necessary consequence, fell back, too.

At its apex, the PCE Deflator in early 2001 reached a high of 2.87% and went no further. What was missing from the episode was every indication of broad-based consumer price inflation that might have suggested their concerns over acceleration or related imbalance. The so-called core rate never really moved all that much, indicating that oil prices off the 1999 lows were entirely responsible for the rise in the rate (WTI was up more than 60% year-over-year when the PCE Deflator registered that 2.87%).

Again, the parallels are pretty clear. And yet, it’s as if there is no history by which to judge current conditions. If anything, there was every reason to suspect accelerating consumer inflation in the late 1990’s that isn’t available now. At least at that time, the economy was actually growing and the labor market robust. If it didn’t happen then over the bond market’s disagreeing, what basis is there to expect it will today as the yield curve similarly objects?

So far, of, course, it isn’t. Inflation either is or it isn’t, there is no in between like we have found now two years past the trough of the last downturn. It has moved on oil prices almost exclusively, where once more the core rate(s) suggest little movement in any direction.

If anything, these indications show more downside risks than upside, consistent with actual weakness as opposed to the constantly imagined labor market strength.

I have no doubt that the majority of policymakers voting at the FOMC believe that price pressures are picking up. More than those, a few additional Committee members probably hope for it. There is, however, not the slightest indication you should believe them.

If it was just a few months of misbehaving figures, then it might be understandable to perhaps give them some benefit of the doubt. But we are talking about years upon years now, and not just the last six years, either. It is a constant theme throughout the activist central bank program. The other constant theme, the one where all this is easily explained, is what Alan Greenspan was talking about way back then (and doing nothing to rectify the grave deficiency in theory as well as practice):

CHAIRMAN GREENSPAN. I must say that I have not changed my view that inflation is fundamentally a monetary phenomenon. But I am becoming far more skeptical that we can define a proxy that actually captures what money is, either in terms of transaction balances or those elements in the economic decisionmaking process which represent money. We are struggling here. I think we have to be careful not to assume by definition that M1, M2, or M3 or anything is money. They are all proxies for the underlying conceptual variable that we all employ in our generic evaluation of the impact of money on the economy. Now, what this suggests to me is that money is hiding itself very well.

It’s not hiding at all, he just never really tried looking. The only thing missing is economy and recovery, the processes that if they were monetarily possible just might produce what the Fed is once again changing its policies for.

Source: http://www.alhambrapartners.com/2018/03/01/still-none-and-even-more-reasons-to-expect-none/