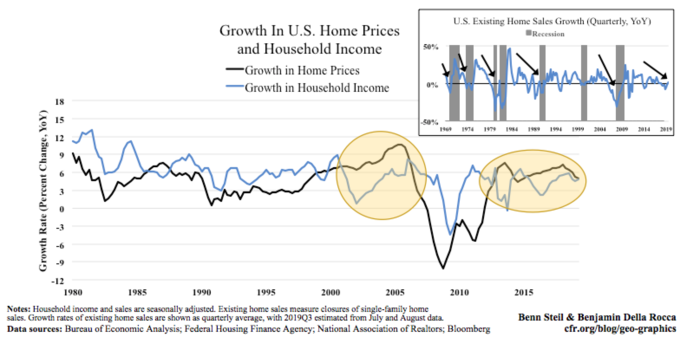

Looking back at the years preceding the 2008 financial crisis, a critical warning sign was the surging gap between the growth in home prices and household income—as can be seen in the main graphic above. When income fails to keep pace with home prices, the latter must fall back. Falling home prices, in turn, drive down household spending by way of the so-called wealth effect—that is, consumers cut spending when their assets fall in value. As one Federal Reserve study shows, consumption falls by $2.50-5.00 for every $100 decrease in housing-market net worth.

Today, a parallel dynamic is playing out—as can readily be seen in the graphic. A similar housing-income gap began opening in 2015. In 2018, as in 2005, housing-price growth began falling rapidly, with significant price drops occurring in several major markets. As the inset figure shows, the trend-line in existing-home sales growth has also been down since 2015, tipping into negative territory at the start of last year. Similar drops have preceded nearly every recession since 1970.

If these trends continue, we should expect broad falls in home prices beginning by mid-2020, which will in turn drag down household spending against a darkening economic backdrop. Growth has been slowing, with Trump’s tariff war hitting exports. Manufacturing is contracting. Retail sales, excluding autos, have stalled. Consumer confidence is falling.

What are the best hopes for avoiding recession, then? Well, we could see a U.S.-China trade deal, which would buoy business confidence. But all signs are that this is unlikely, given Chinese insistence that structural reforms are now off the table. A so-called narrow deal, with punitive tariffs eliminated in return for greater Chinese purchases of soybeans and LNG, would amount to a total victory for Beijing, given the country’s naturally rising demand for both. So our base-case is that the trade war continues.

The Fed? Well, if we are really on the cusp of a recession it will likely take more than 175 basis points of easing to prevent it—and that is all the central bank has to play with before we’re back to the zero lower bound. At that point, applying monetary stimulus becomes considerably more challenging.

In short, then, we think Trump will be entering the election homestretch with some strong economic headwinds against him. Most notable among them will be a declining housing market.

Source: https://www.cfr.org/blog/housing-market-points-recession-election-day