- As the COVID-19 pandemic gathers momentum, history offers too few data points

- The Spanish Flu is the nearest comparison – similarities are matched by differences

- Clinical trials have started, but the rise in new cases is slowing in China already

- Global economic growth will suffer, but monetary and fiscal stimulus should support stocks

As I write this article I am conscious that the Coronavirus is a very real and global tragedy. In all that follows I do not wish to detract from the dreadful human cost of this disaster in any way.

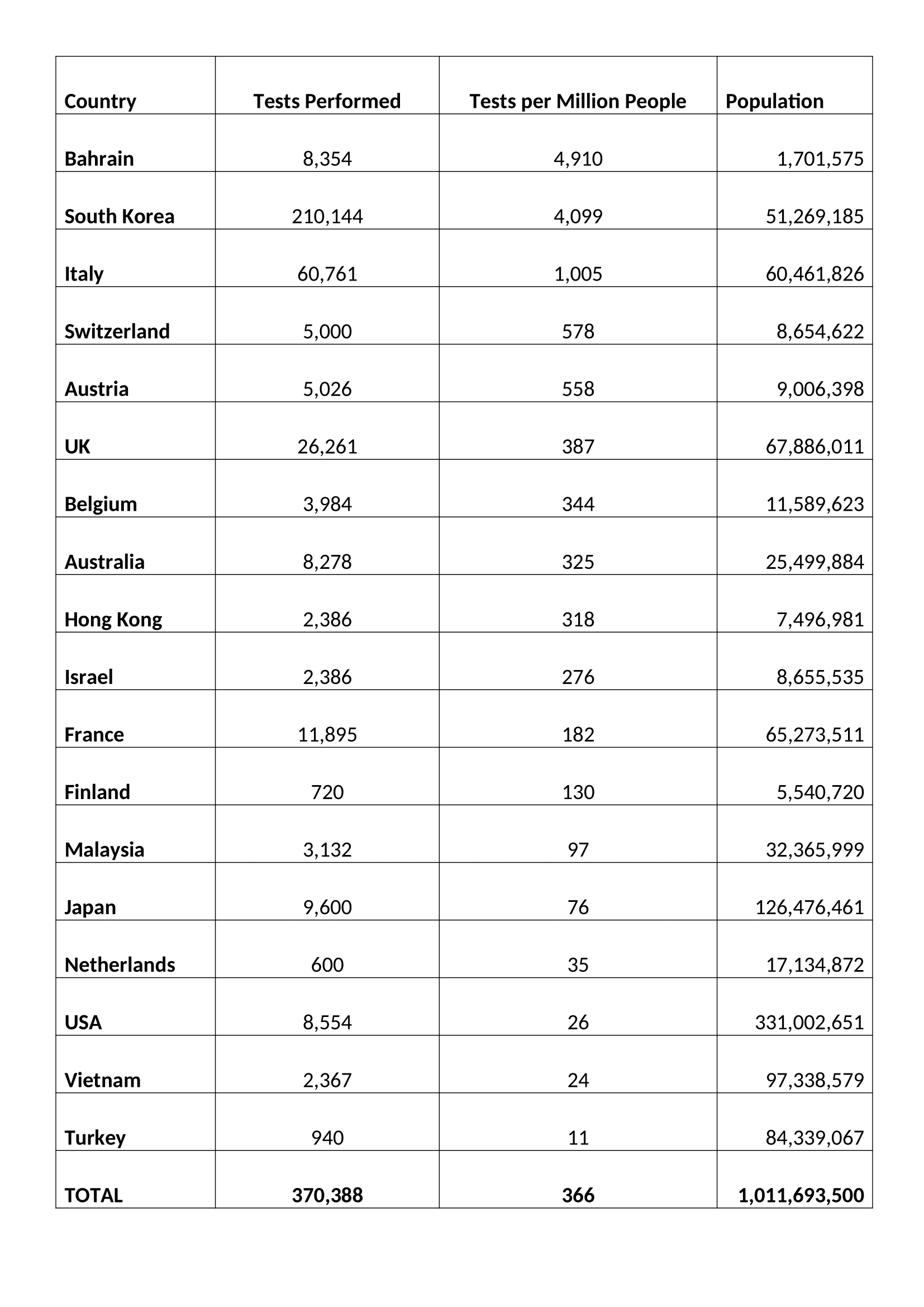

Putting the current pandemic in perspective, according to a 2017 estimate from the US Center for Disease Control, in a normal year, seasonal flu kills 291,000 to 646,000 globally. By contrast, the fatality rate for coronavirus seems to have stabilised at around 3.6% of those diagnosed. Of course, a more heartening figure of 0.79% can be found in South Korea which has tested almost 10 times more of its population than other country:-

Source: Worldometer.com

Suffice to say the current statistics are still confusing at best, but they are all we have to work with.

In a recent interview Dr Soumaya Swaminathan of the World Health Organisation (WHO) provided some insights (emphasis is mine): –

Of 44,000 Wuhan patients 80% had very mild symptoms, 15% of cases are severe and 5% critical. In terms of transmission rates, the R0 is still just an estimate of between 2 and 3 – in other words for every carrier between two and three people are infected.

…Two drugs, an antiretroviral called Lopinavir-ritonavir and an experimental drug used in the treatment of Ebola – Remdesivir, manufactured by Gilead (GILD) – are being tested in China where more than 80 clinical trials are already underway. The development of an effective vaccine it several months away.

It was reported today (11-3-2020) that Gilead has begun trails with US nationals and signed a deal with the US military.

Market Impact

Given the continued lack of clarity about COVID-19 in terms of numbers infected and numbers suffering, it may seem futile to attempt to gauge the potential economic impact of the current Coronavirus outbreak. History, however, may be able to provide some guidance to investors who might otherwise be tempted to liquidate and hibernate, especially after the dramatic decline this week in the wake of Saudi Arabia’s decision to turn its back on the OPEC cartel.

In order to begin this assessment, there are a vast array of factors which need to be considered. Here are just a few: –

- Speed of spread – higher in urban areas due to population density

- Urban versus rural population – generally a function of GDP per capita

- Likelihood of a cure or vaccine – the majority of estimates range from three months to a year (hopefully it was be sooner)

- Health of demographic cohorts by country – a function of average age and GDP per capita

- Average income – also a function of GDP per capita

- Extent of healthcare coverage – generally a function of GDP (although European welfare arrangements are more developed than those of the US)

Each of these factors are complex and warrant an essay to themselves. Suffice to say, the economic impact is already becoming evident. Schools, factories and offices are closing. Those workers that can are beginning to work remotely. At the extreme, entire cities, towns and countries are being subjected to lock-downs. In these conditions, economic activity inevitably suffers, this is a supply and demand shock combined. The price of crude oil has already responded, encouraged by the actions of Saudi Arabia, it has collapsed. Transportation activity has been substantially reduced. Economic indicators from China point to a pronounced contraction in 2020 GDP growth. Will the pattern seen in China be repeated elsewhere? Are the nascent indications of a resumption of economic activity now evident in China a reliable indication of the speed of recovery to be expected elsewhere? The jury is still out.

For G20 countries the effect of the 2008/2009 financial crisis still lingers. According to a BIS report more than 12% of developed nation firms generate too little income to cover their interest payments. Meanwhile, at the individual level, the Federal Reserve estimates that more than 10% of American adults would be unable to meet a $400 unexpected expense, equivalent to around two days’ work at average earnings. There is concern among governments that people may start to hoard cash if the crisis deepens.

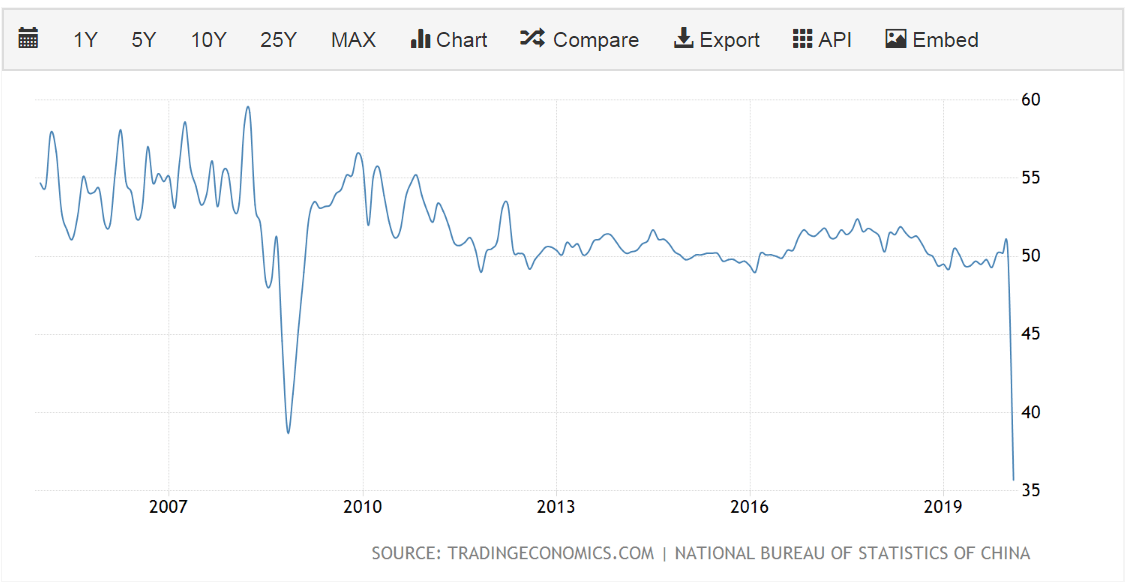

Where the viral epidemic began, in China, the Purchasing Managers Index for February was the lowest since the series began in 2004. According to China Beige Book’s flash survey for February, 31% of companies were still closed and many of those that have reopened lacked staff or materials. Other estimates suggest that between 40% and 50% of the China’s truck fleet remains idle – those essential materials are unlikely to be delivered anytime soon. This supply-shock slowdown has inevitably fuelled expectations of an actual contraction in the size of the Chinese economy, the first shrinkage since the death of Mao Zedong in 1976: –

Source: Trading Economics

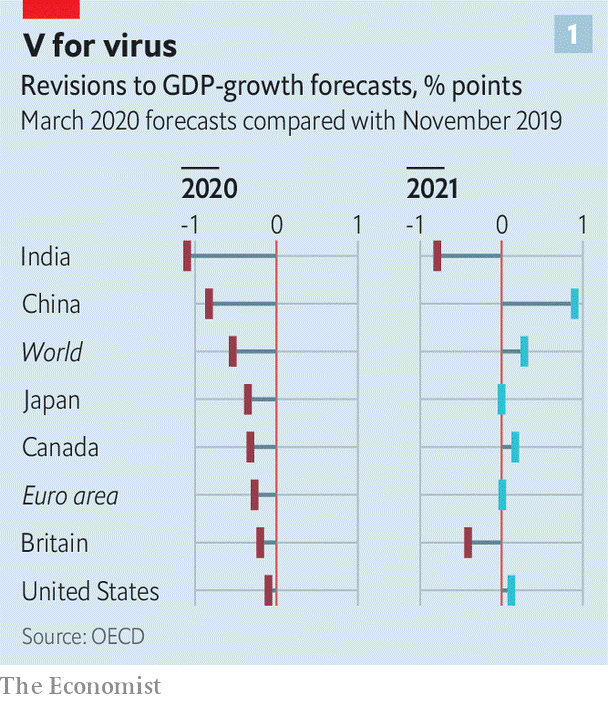

Everywhere GDP forecasts are being revised lower: –

Source: Economist

Policy Response

For the world’s governments there are essentially three policy responses: –

- Provision of credit via banks and money markets – central banks are doing what they can

- Aid to corporates to meet fixed costs, such as rent and tax bills

- Protection of workers by subsidising wage costs

Central banks are limited in their ability to lend directly to firms, meanwhile the banking system, petrified by the recent widening of credit spreads for sub-investment grade debt, is likely to become a bottleneck. It will take more than gentle persuasion to force banks to lend new funds and reschedule existing non-performing loans. Other aid to corporates and individuals requires varying degrees of fiscal stimulus. Governments need to act quickly (today’s UK budget is an indication of the largesse to follow) it would also help if there were a coordinated global policy response.

The Peterson Institute – Designing an effective US policy response to coronavirus make the following suggestions: –

A first step is to lock in adequate public funding. In 2014, emergency funding of about $5.4 billion was provided to fight the Ebola outbreak. Much more than that should be provided today, given the apparently greater transmissibility of COVID-19 and the fact that it has already appeared in many locations around the United States and more than 60 countries around the globe.

…A classic recession involves a shortfall of demand relative to supply. In that more ordinary situation, economic policymakers know how to help fill in the missing demand. But this case is more complicated because it involves negative hits to both supply and demand.

…No one knows how serious the economic damage from COVID-19 will be, so a key challenge is to design a fiscal countermeasure that clicks on when it’s needed and clicks off when it’s not. One approach that would fit that description would be to move immediately to pre-position a temporary cut in the payroll taxes that fund the Social Security and Medicare programs…

The final suggestion is a US-centric proposal, it is different from the income tax cut alluded to by President Trump and will directly benefit lower-income families, since healthcare costs will be a larger proportion of their after tax income. The authors’ propose a similar mechanism to click in when the unemployment rates rises and click off when re-employment kicks back in.

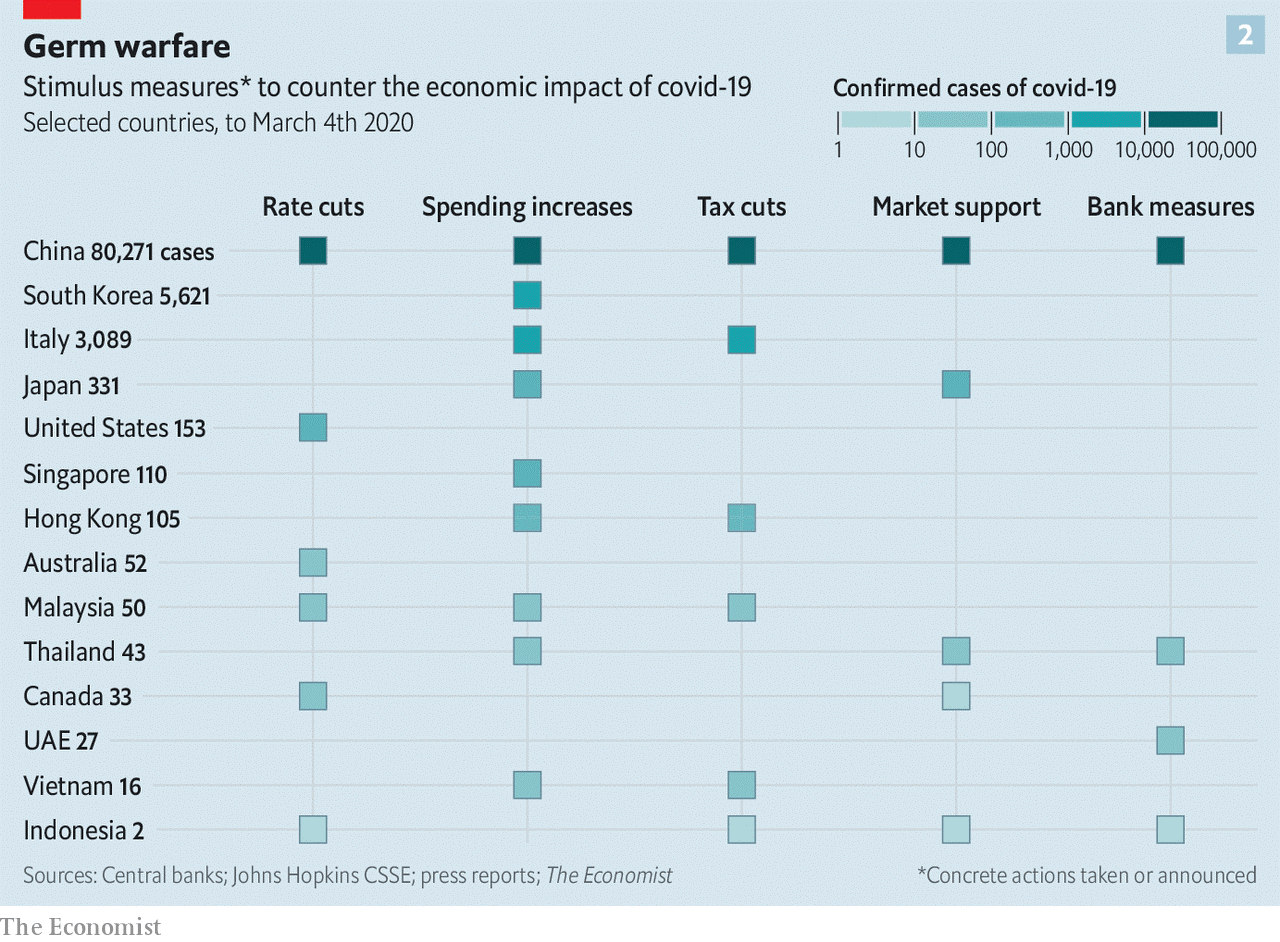

The table below shows actions taken by 4th March: –

Source: Economist

It is worth mentioning that Hong Kong, still reeling from the civil unrest of last year, has pressed ahead with ‘helicopter money’ sending cheques to every tax payer. This approach may be more widely adopted elsewhere over the coming weeks.

The Spanish Flu

In an attempt to find an historical parallel for the current Corona outbreak, there are only two episodes which are broadly similar, the Black Death of 1347 to 1351 and the Spanish Flu of 1918 to 1919. Data from the middle ages is difficult to extrapolate but it is thought that the Plague wiped out between 20% and 40% of Europe’s population. The world population is estimated to have fallen from 475mnl to between 350mln and 375mln. The world economy shrank, but, if data for England is any guide, per capita economic activity increased and the economic wellbeing of the average individual improved. For more on this topic I would recommend a working paper from the Federal Trade Commission – The English Economy Following the Black Death by Judith R. Gelman -1982.

The Spanish Flu of 1918 was the next global pandemic. It began in August of 1918, three month prior to the end of the First World War, and, by the time it had ended, in March of 1919, it had infected 500mln out of a global population of 1.8bln. The fatality rate was high, 40mln people lost their lives. Following the war, which cost almost 20mln lives, the combined loss of life was similar in absolute terms to the Black Death although in percentage terms the fatality rate was only 2%.

An excellent assessment of the Spanish epidemic can be found in the Economic Effects of the 1918 Influenza Pandemic – Thomas A. Garrett – Federal Reserve Bank of St Louis – 2007 – here are some key findings: –

The possibility of a worldwide influenza pandemic… is of growing concern for many countries around the globe. The World Bank estimates that a global influenza pandemic would cost the world economy $800 billion and kill tens-of-millions of people. Researchers at the U.S. Centers for Disease Control and Prevention calculate that deaths in the United States could reach 207,000 and the initial cost to the economy could approach $166 billion, or roughly 1.5 percent of the GDP. Longrun costs are expected to be much greater. The U.S. Department of Health and Human Services paints a more dire picture—up to 1.9 million dead in the United States and initial economic costs near $200 billion.

…Despite technological advances in medicine and greater health coverage throughout the 20th century, deaths from a modern-day influenza pandemic are also likely to be related to race, income and place of residence.

The Spanish-flu was different from COVID-19 in that the highest mortality was among those aged 18 to 40 years and was often found among those with the strongest immune systems.

Garrett goes on to assess the economic impact with the aid stories from newspapers and the limited amount of previously published (and some unpublished) research. National statistics on unemployment and economic activity had yet to be compiled, but the simultaneous supply and demand shocks were broadly similar to the patterns we are witnessing today.

…One research paper examines the immediate (short-run) effect of influenza mortalities on manufacturing wages in U.S. cities and states for the period 1914 to 1919. The testable hypothesis of the paper is that

influenza mortalities had a direct impact on wage rates in the manufacturing sector in U.S. cities and states during and immediately after the 1918 influenza. The hypothesis is based on a simple economic model of the labor market: A decrease in the supply of manufacturing workers that resulted from influenza mortalities would have had the initial effect of reducing manufacturing labor supply, increasing the marginal product of labor and capital per worker, and thus increasing real wages. In the short term, labor immobility across cities and states is likely to have prevented wage equalization across the states, and a substitution away from relatively more expensive labor to capital is unlikely to have occurred.

The empirical results support the hypothesis: Cities and states having greater influenza mortalities experienced a greater increase in manufacturing wage growth over the period 1914 to 1919.

Another study explored state income growth for the decade after the influenza pandemic using a similar methodology. In their unpublished manuscript, the authors argue that states that experienced larger numbers of influenza deaths per capita would have experienced higher rates of growth in per capita income after the pandemic. Essentially, states with higher influenza mortality rates would have had a greater increase in capital per worker, and thus output per worker and higher incomes after the pandemic. Using state-level personal income estimates for 1919-1921 and 1930, the authors do find a positive and statistically significant relationship between state-wide influenza mortality rates and subsequent state per capita income growth.

Aside from wages, however the author concludes: –

…Most of the evidence indicates that the economic effects of the 1918 influenza pandemic were short-term. Many businesses, especially those in the service and entertainment industries, suffered double-digit losses in revenue. Other businesses that specialized in health care products experienced an increase in revenues.

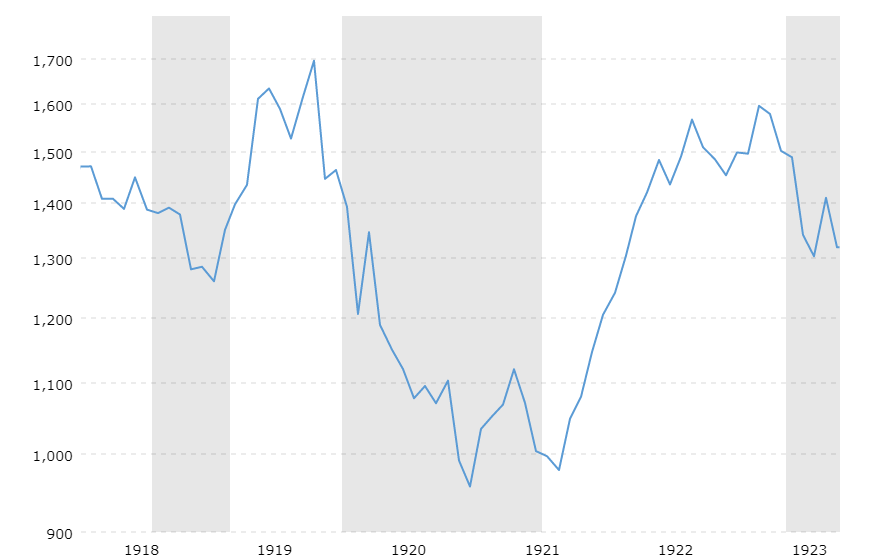

How did financial markets react? The chart below shows the Dow Jones Industrial Average over the period from 1918 to 1923. The shaded areas indicate recessions: –

Source: Macrotrends

When reinvested dividends are included, the total return of the Dow Jones Industrial Average in 1918 was 10.5%, despite influenza wiping out 0.4% of the US population. Fears about a slowdown in economic activity, resulting from the end of WWI, were the underlying cause of the brief recession which coincided with the pandemic, the stock market had already reacted, dipping around 10% earlier in the year. The subsequent recession of 1920 had other causes.

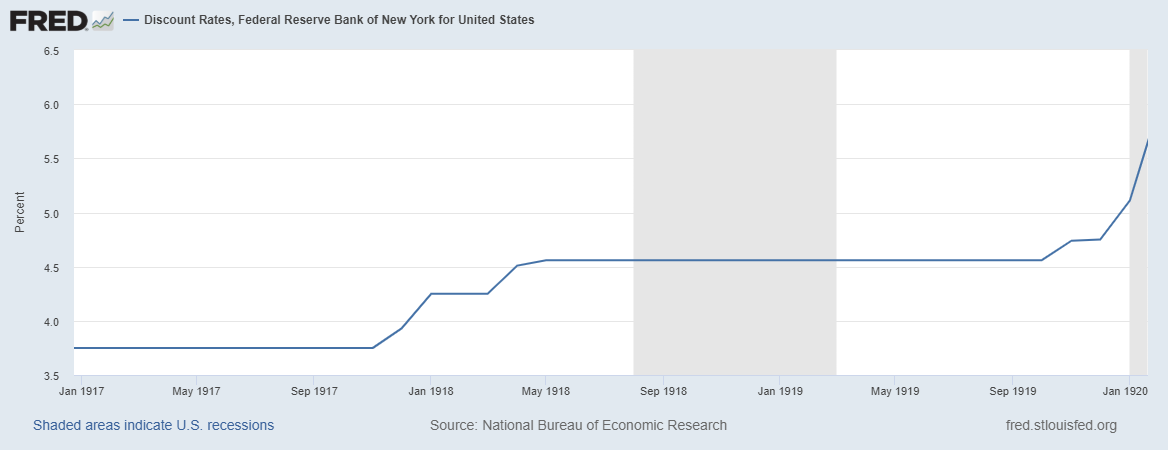

As is evident from the chart below, the newly created (1913) Federal Reserve felt no compunction to cut interest rates: –

Source: Federal Reserve Bank of St Louis

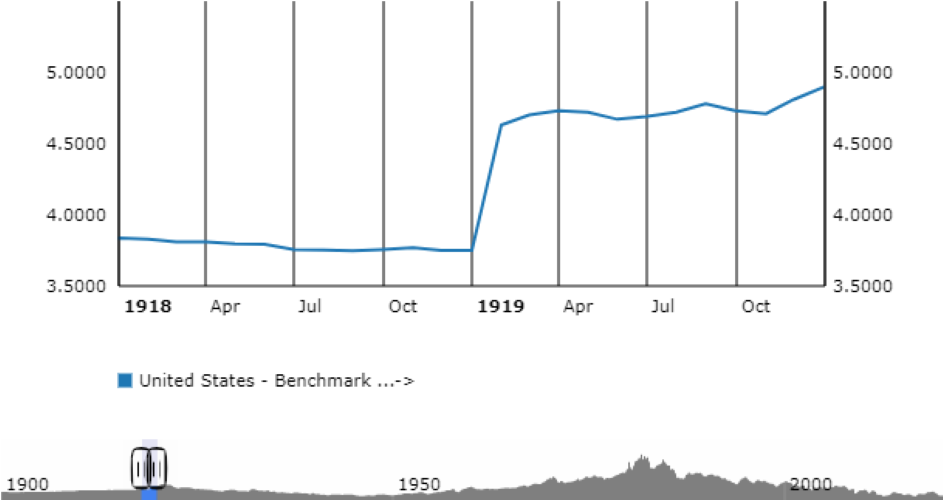

US 10 year Treasury Bonds simply reflected the actions of the Federal Reserve: –

Source: ECB

One is forced to concede, financial markets behaved in a very different manner 100 years ago, but they may yet have something to teach us about the global impact of a pandemic – that it is an economic interruption rather than a permanent impediment to progress.

Conclusions and investment opportunities

Whilst there are similarities between the Spanish Flu of 1918 and the COVID-19 pandemic of today, there are also profound differences. Urban areas, for example, are expected to suffer higher fatalities than rural areas today. In 1919 only 51% of the population of the US was urban, today it is above 80%. Population density has also increased three-fold over the last century, if 500mln were infected in 2018/2019 then the comparable figure today would be 1.5bln. Changes in the ease of transportation mean that the spread of a pandemic will be much more rapid today than in the first quarter of the 20th century. Tempering this gloom, for many people, communications have transformed the nature of work. Many aspect of business can now be transacted remotely. Unlike in 1918 self-isolation will not bring commerce to a standstill.

The economic impact will also be felt more rapidly. Supply chains have been optimised for efficiency, they lack resilience. Central banks have already begun to cut interest rates (where they can) and provide liquidity. Governments have picked up the gauntlet with a range of fiscal measures including tax cuts and benefit payments.

Many commentators are calling the COVID-19 pandemic a Black Swan event, yet SARS (2003), H1N1 (2009), and MERS (2012) preceded this outbreak. Predictions that just such an event would occur have been circulating for more than a decade.

Financial markets have behaved predictably. The oil price has collapsed as Saudi Arabia has broken with the OPEC cartel, stocks have fallen (especially those related to oil) and government bonds have rallied. Gold, which saw significant inflows during the last few years, has vacillated as holders have liquidated to meet commitments elsewhere even as new buyers have embraced the time-honoured ‘safe haven.’ Looking ahead, we do not know how long this pandemic will last nor how widespread it will become. The two prior pandemics of a similar stature provide little useful guidance, the Spanish Flu lasted seven months, the Black Death, by contrast, spread over more than four years and was still flaring up into the 17th century.

Expectations of a cure and a vaccine remain a matter of conjecture, but epidemiologists suggest that within a year we will have a viable solution. At the time of writing (Wednesday 11th March) the total number of infections has reached 120,588, there have been 4,365 deaths while 66,894 patients have recovered – a 55.47% recovery rate, although the Chinese recovery rate has been steadily rising and now stands at 76.22%. The global fatality rate is 3.62%, whilst individual country fatality rates range from Italy at 6.22% to South Korea (where 210,000 people have been tested – ten times the per capita global average) at a heartening 0.79%. The WHO still expect the fatality rate to stabilise at around 1% which implies that 99% should eventually recover.

Whilst a larger correction in stocks should not be ruled out, the relative lack of selling pressure suggests that investors are prepared to reappraise their estimates of what price to earnings they will accept – remember interest rates have been cut and will probably be cut again. Where rates can be lowered no further, quantitative easing (including the purchase of stocks) and fiscal stimulus will aim to preserve value.

The historical evidence of the Spanish Flu suggests this pandemic will be short-lived. The recent market correction may prove sufficient but, with only two data points in more than 600 years, it is unwise to assume that it will not be different this time. Defensive equity strategies which focus on long-term value have been out of favour for more than a decade. Good companies with strong balance sheets and low levels of debt are well placed to weather any protracted disruption. They may also benefit from rotation out of index funds. When markets stabilise, the reduced level of interest rates will see a renewed wave of capital pouring into stocks. The only question today is whether there will be another correction or whether now is the time to buy.