In all the economic mayhem ahead, no one is yet thinking of the consequences for trade imbalances. The twin deficit hypothesis informs us that skyrocketing US budget deficits will lead to increasing trade deficits, a situation with serious political consequences. Furthermore, with foreign interests already saturated with dollars and financial assets denominated in them, far from investing their growing surpluses in yet more dollars and dollar-denominated investments, they will become increasingly aggressive sellers.

This article walks the reader through the main issues of international trade in a developing slump and finds worrying parallels with the Wall Street crash and subsequent events. While the parallels are worrying, the major differences between then and now suggest that this time outcomes could be even more economically challenging.

Introduction

Following the presidential election this week, the new President of the United States will face an economic slump. Long before the covid-19 lockdowns, economic and financial developments threatened to undermine both the US economy and the dollar.

The similarities between the situation today and the end of the roaring twenties, and the depression that followed, are enormously concerning. Both periods have seen a stock market bubble, fuelled by bank credit and an artificial monetary stimulus by the Fed. Both periods have experienced an increase in trade protectionism: In October 1929, the month of the crash, after debating it for months Congress finally passed the Smoot Hawley Tariff Act, raising tariffs on all imported goods by an average of about 20%. In 2019, US trade protectionism against China put a stop to the expansion of international trade. These facts, which should continue to concern us, have been buried by the immediacy of the coronavirus crisis, which is an additional burden for the global economy today compared with the situation ninety years ago.

As is nearly always the case in the year of a presidential election, economic negatives get buried in waves of reflationary optimism. This time the optimism has in turn been buried by the virus, but the reflation relation is still there in spades. The American budget has soared from a previously planned trillion dollars or so to $3.3 trillion in the fiscal year that ended last month. Between March and September, the deficit increased over the first half of the fiscal year by $2.7 trillion, an annualised rate of $5.4 trillion. And given the resurgence of the virus and the US Government’s commitment to avoid the slump, not only is the budget deficit likely to be even greater in the current fiscal year, but all else being equal it will be out of control for several years to come. Money-printing as a source of finance has already overtaken tax receipts by a substantial margin.

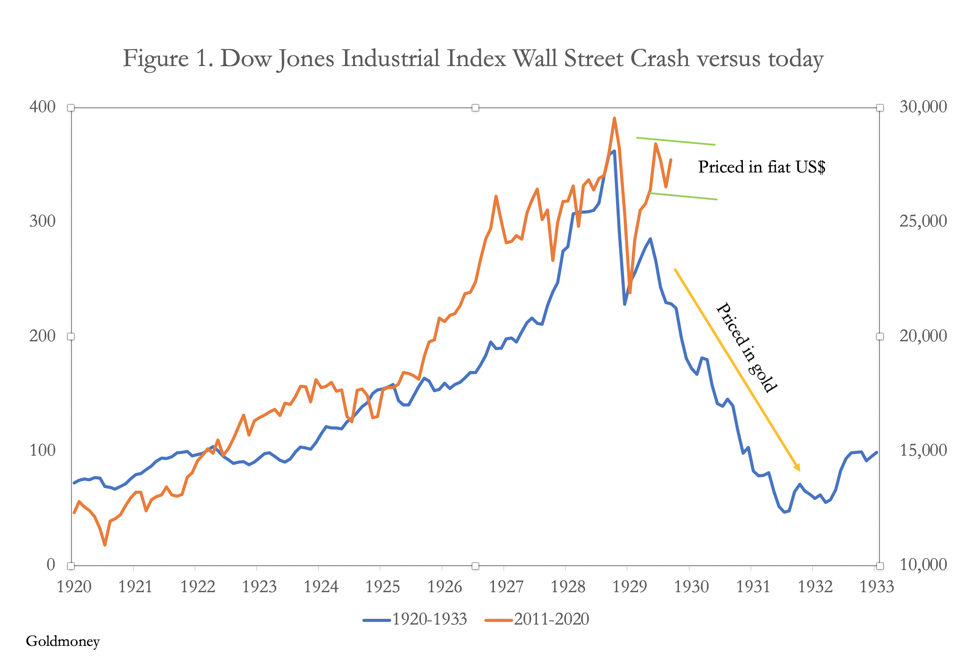

While the Wall Street Crash commenced in late September 1929, there was an initial consolidation that lasted until the following May, nearly eight months. The recent market collapse between last February and March and the initial recovery to September echoed the duration of the recovery in 1929—1930, as shown in Figure 1 below. Today’s Dow is superimposed on the that of 1920—1933.

The difference between the two periods is that between 1920—1933 the Dow was effectively priced in gold through the dollar at $20.67 to the ounce, while today it is priced in unbacked fiat dollars. It is a matter of fact that today’s dollars are issued by the Fed with a view to keeping the investment yardstick, US Treasuries, yielding as little as possible. And by flooding the financial markets with money, in relative valuation terms equity prices are artificially supported in defiance of economic fundamentals by current monetary policies.

It is a situation that cannot persist. Sooner or later, monetary inflation will undermine the purchasing power of the dollar as measured on the foreign exchanges, foreign selling of dollar portfolio assets is bound to escalate, the yields on US Treasuries will rise beyond the Fed’s control, and equities will adjust towards fundamentally derived values.

The twin deficits

There is an important question few analysts have so far considered. The US budget deficit soared to $3.3 trillion in the last fiscal year to end-September and looks like being even greater in this new fiscal year. Will this test, or even disprove the twin deficit hypothesis, whereby if the savings rate doesn’t change, a budget deficit leads to a matching trade deficit? Obviously, if the trade deficit soars with the budget deficit, there will be substantial political and economic issues.

The reason the two deficits are linked is because of the following accounting identity:

Net imports ≡ (Investment – Savings) + Budget deficit.

The simple explanation as to why it is the case is to follow the money. There are two sources of funding a budget deficit. Either savers put aside some of their spending to increase their savings in order to subscribe for government bonds, alternatively selling other investments to buy newly issued Treasury bonds. Or the banking system comes up with the money, in the form of money issued by the central bank or by commercial banks expanding credit — in both instances creating money which didn’t exist before.

The financing of a budget deficit by money printing and understanding the consequences should be relatively straightforward. The role of savings in the economy is more complex. An increase in savings is at the expense of consumption, which is why economists often refer to savings as consumption deferred. For consumption to remain deferred for a reasonable period requires it to be invested, either into production, or into government debt through the banks, pension funds, insurance companies or other financial channels acting on the savers’ behalf.

If the destination of additional savings is investment in government debt, little further analysis of flows is necessary, beyond commenting that savings are turned into consumption by the government. But alternatively, if savings go into production, after a time lag there is likely to be an increase in domestic production of goods and services, either increasing exports or alternatively diminishing imports.

Broadly, this is what happens in Japan. The Bank of Japan issues additional money by buying Japanese government bonds. Assuming for simplicity’s sake that the banknote issue is unchanged, all the new money goes into the banking system. From there the new money is allocated to the sellers of the bonds’ bank accounts, including those of the commercial banks themselves. It is also the fuel for the expansion of bank credit into other avenues, including consumer credit. But the average Japanese consumer is not interested in borrowing — since 2008 total credit to the non-financial private sector up to March this year expanded by only 5.6% in nominal terms over eleven years,[i] while M3 money supply expanded by 34%[ii]. Furthermore, of the increase in outstanding M3, only 0.4% ended up as increased consumer lending.

Measured in nominal monetary terms, demand for consumer goods in Japan hardly increased, while 99.6% of the increased broad money supply ended up being invested, and therefore explains why a large government deficit is not matched by a trade deficit but a trade surplus; the surplus arising from the consequences of investment in production by Japanese corporations both in Japan and abroad, the latter leading to additional inward remittances over time.

The same is true of any economy where there is a government deficit while at the same time there is a propensity in the population to save rather than spend. It is also the driving force behind China’s export surpluses, because the Chinese are the biggest savers on the planet.

The position of nations whose economic policies have been to tax savings heavily and to encourage immediate consumption is correspondingly different. In the US, over the same time frame as that in the Japanese example above, broad money supply has increased by 125%[iii] and consumer credit by 58.7%[iv]. Of the increase in broad money, 22% of its was directed into consumer credit. Of the remaining 78% increase, only $1.26 trillion of expanded bank credit was recorded as increased commercial and industrial bank loans,[v] representing just 16% of the increase in broad money. Clearly, the proportions of the increase in the quantity of money have been strongly skewed in favour of consumption relative to domestic production.

It is this excess of consumption, reflected in balances arising from the expansion of money and credit which were not invested in production but spent on consumer goods that has led to persistent US trade deficits over the period considered.

The evidence is that a savings driven economy is more successful than a consumption driven economy. Not only does the former protect the currency’s purchasing power by reducing the need for reliance on foreign capital inflows to finance internal deficits, but empirical evidence clearly shows savings-driven economies are more successful at creating wealth for their citizens, which is retained by a stronger currency, than those with inadequate savings whose values are further eroded by the weaker currency’s purchasing power.

It’s about the requirements for the division of labour

There are two routes to establishing the roles of savings and consumption in setting trade balances at a time of budget deficits. One can look at it through the lens of the financing of government deficits by government bonds, or one can look at it through the expansion of money and credit. The latter encompasses the wider aspects of the investment relationship in the equation, which is why this article has pursued this route. Additionally, it allows for a confirmation of this analysis, through Say’s law, with the objective of exploring the prospects for the relationships between the twin deficits at a time of increasing economic stress, such as we are likely to see in the coming months.

Discarded by modern macroeconomists, Say’s law is fundamental to understanding the issues around the division of labour. It cannot be denied that in the absence of distortions introduced by state intervention that the human race maximises its economic efficiency through the division of labour, whereby individuals apply their knowledge and personal skills to maximise their output measured by the goods and services they subsequently acquire in order to satisfy their needs and wants. The exchange role of money is merely to make efficient the transfer of labour into consumption. This is what Say’s law describes, and it is nonsense for any macroeconomist to deny it.

Having established this truism as unarguable fact, we can proceed to describe the effects on the relationship between production and consumption of additional money produced out of thin air. Obviously, the source of that money, or credit, is not someone else’s production. If it ends up in consumers’ pockets, this extra money, not being immediately matched by production, will lead to extra demand for imported goods in preference to bidding up prices for domestic production that is now temporarily scarce relative to the expanded stock of money. Of course, if the monetary expansion then ceases, the fuel for extra imports will have been consumed and a balance will then return.

But in addition to the effects of changes in the quantity of money and credit being issued, there is a further factor rarely considered — changes in the relationship between the quantity of money held in possession relative to goods — sometimes referred to as hoarded money. More than changes in the quantity of circulating currency, shifts in the amount of money held in reserve for purchases in the near future have a major impact on the purchasing power of money. Stability in the money relation only exists in money chosen by its users and beyond state manipulation: metallic money, principally gold and silver circulating as coins and their fully backed substitutes.

The discipline of metallic money

Ever since the invention of bank notes, not all the money in circulation was gold or silver substitutes. Even with a gold exchange standard, which is what bank notes unconditionally exchangeable for gold purported to be, public confidence in the issuer of bank note money is fundamental to its acceptance.

Typically, a note issuing authority did not back every note issued with bullion. When the Bank of England became the principal note issuer following the Bank Charter Act of 1844, its note issue was only 50% backed by gold, the rest was backed by consolidated loan stock issued by the government. But all subsequent note issues were backed by gold, and exchangeable for gold sovereigns, still legal tender today. Additionally, commercial banks issued credit created out of thin air, leading to periodic boom and bust cycles. But in general terms the restraints against over-issuance worked well enough.

Before the First World War governments were small in relation to their private sectors, and they generally accepted the right of its users to decide what money to use. The idea of running budget deficits, beyond small imbalances from time to time was confined to war finance. With gold as the monetary medium, differences in the general level of prices that arose as a result of variations of the quantities of gold in circulation were ironed out through arbitrage. A country with a higher level of gold stocks and substitutes in private hands, and therefore higher unit prices for goods than in another centre with less gold stocks and therefore lower unit prices, would see gold outflows to purchase the lower priced goods available abroad.

Irrespective of changes in the relationship between gold, gold substitutes and fiat masquerading as gold substitutes, the system worked, so long as the gold substitutes and the indistinguishable fiat were confidently accepted. The key to that confidence was to always ensure that gold and silver coinage circulated, and that paper money was exchangeable for coinage at the official conversion rate without limitation.

Under a pure gold standard where there is no unbacked fiat in circulation, with gold substitutes being fully backed there can be no trade imbalance beyond very short-term settlement considerations. If a government fails to balance its books, any deficit is paid for through gold outflows. And if it is a persistent problem, its gold reserves become drained. Presumably, this was the difficulty anticipated by the Roosevelt administration in 1933, which led to the suspension of gold convertibility for domestic purposes, followed by a monetary reset in January 1934.

In effect, the US Government was determined to remove the constraints of sound money in order to use monetary inflation as a tool of economic management. By undervaluing the dollar relative to gold by changing the exchange rate from $20.67 to $35, foreigners bought dollars by selling gold. At the time, budget deficits were rapidly increasing — in 1933 the deficit was $3.6bn, a record for peacetime, representing 6.4% of GDP. But the trade balance was a surplus of $1bn, indicating that the deficit was financed by savings and foreign monetary inflows. And indeed, we find that over the decade, US gold monetary reserves increased from 6,358 tonnes to 19,543 tonnes.[vi] At the same time, the cumulative budget deficit for the decade was $14.5bn, the equivalent of 12,886 tonnes of gold at $35 per ounce which compares with the increase of 13,185 tonnes in monetary reserves, a portion of which would have accumulated from domestic mining.

Notwithstanding the ban on public ownership of gold from 1933 onwards there was no doubt that the habit of regarding the dollar as a gold substitute fooled both domestic and foreign users into continuing to believe in it as such. Despite the expansion of the dollar quantity in foreign hands, which continued to expand through the Second World War and following Bretton Woods, the dollar was accepted as good as gold until the early 1960s, when America’s gold stock began to be depleted. Consequently, the effects of monetary inflation on prices were minimal, until the system collapsed in 1971.

The 1970s decade was the first in modern times which saw the formally gold-backed dollar lose its anchor. The move from internationally backed gold pricing to pure fiat led to progressively greater trade imbalances, and economists began to advocate “competitive” exchange rates to correct them, ignoring the fundamental differences between a monetary system based on gold and unbacked fiat. Unbacked fiat has now been the rule for forty-nine years, and the loss of the dollar’s purchasing power, from when it was first driven off the $35 exchange rate with gold, is now 98.2%, measured in gold.

We have now entered a period that rhymes strongly with the Wall Street Crash of 1929—1932 and the subsequent slump in the global economy. According to the equation which identifies the relationship between budget and trade deficits, we can presume the US trade deficit to increase significantly; in which case we can expect Washington to double down in its attempts to contain it. Whether by further tariff increases or by import controls, prices of imported goods and services are bound to rise for American consumers. At the same time, the absence of domestic production to match the expansion of circulating currency is bound to push up the general level of prices substantially.

The fate of the dollar’s purchasing power will initially depend heavily on the desire, or lack of it, on the part of foreigners to reinvest their rapidly expanding quantities of dollars in dollar denominated securities. But given their current position, whereby over $20 trillion are already invested in financial securities with a further $5.6 trillion in T-bills commercial bills and bank deposits, a continuing balance of payments can be ruled out. In difficult economic times, foreigners are bound to have other priorities to increasing their already massive stockpile of dollars.

The Fed and US Treasury are drifting helplessly into a perfect storm. While attempting to fund a budget deficit currently running at an annualised $5.4 trillion, instead of being able to rely on foreigners reinvesting their trade surplus dollars the Fed will have to replace foreign demand for dollar denominated financial assets with additional QE. Worse still, a wholesale liquidation of dollar assets and dollar deposits by foreign holders is becoming increasingly likely, a fundamental difference from the situation in the 1930s, when foreigners were prepared to buy a sharply devalued dollar.

Summary

Putting the extra problems of the coronavirus to one side, there are a number of worrying parallels between the situation today and that of early 1930. Both periods came after a prolonged period of bank credit expansion on top of increases in the money supply. Both periods have seen trade tariffs weaponised, which combined with the unwinding of excessive bank credit has a synergistically negative effect on stock markets as well as the underlying economy. To the extent that this is true, a slump in business conditions in the next few years was certain even before covid-19 struck.

The economic conditions we face in the next year or two will have many similarities with those of the 1930s. The most important difference was in the money. Ninety years ago, the dollar was convertible into gold on demand, which meant that prices were effectively in gold. When Roosevelt devalued the dollar in January 1934, the consequence was foreigners were happy to buy dollars for gold, and US gold reserves increased. The dollars created for gold helped finance the budget deficits. Furthermore, imports and exports roughly balanced, telling us that US citizens tended at the margin to save their money, allowing the government ample funding room. The reluctance to spend was seen by Keynes and other inflationists as the greatest hurdle to economic recovery, which led to the neo-Keynesian policies of today.

Consequently, after decades of eviscerating the US private sector of savings and removing the obstacle of sound money, today the dollar has no backing and a diminished savings habit. Unlike the situation in 1930, today’s unbacked dollar is already over-owned by foreigners, and savers rarely put money aside, apart from mandatory savings such as pensions and life insurance.

Assuming governments are not prepared to cut their spending, the forthcoming slump will lead to even greater budget deficits for welfare-driven governments than we have seen so far in this calendar year. Inevitably, nations such as the US will find that under the twin deficit hypothesis trade deficits will tend to increase as well, becoming politically destabilising, and likely to lead to yet more trade protectionism. But that will be a dangerous game. In the case of the US, the dollar is already over-owned by foreign interests, the recycling of surplus dollars having made a major contribution to funding the budget deficit in recent decades. In a slump, foreign interests are bound to shift away from having large dollar balances.

There is still to properly address the political problem of the tendency for trade deficits to escalate with budget deficits. Escalating US trade deficits at a time of economic contraction are bound to put further selling pressure on the dollar, and the political class — whoever is president — is almost certain to blame foreigners for America’s plight. It is therefore likely that yet more tariffs and import controls will be imposed. This was how with the Smoot-Hawley Tariff Act America exported its slump around the world in the 1930s, and we can begin to see how it will happen again; only this time the forces are far greater because in the 1930s the US had a modest balance on its trade.

The only solution is not one concocted by the state’s inflationists: empirical evidence is that when a monetary reset has been tried in the past it always failed. By the course events, the statists will be made to understand that the only solution is metallic money, gold, silver and even copper for the smallest transactions. For millennia, when the state’s money failed, that is what people always returned to. They will again.

[i] See https://fred.stlouisfed.org/series/CRDQJPAPABIS

[ii] See https://fred.stlouisfed.org/series/MABMM301JPM189S

[iii]https://fred.stlouisfed.org/series/MABMM301USM189S

[iv] See https://fred.stlouisfed.org/series/TOTALSL

[v] See https://fred.stlouisfed.org/series/TOTCI

[vi] See Table 1: Central Bank Reserves — An historical perspective since 1845; Timothy Green published by the World Gold Council, November 1999.