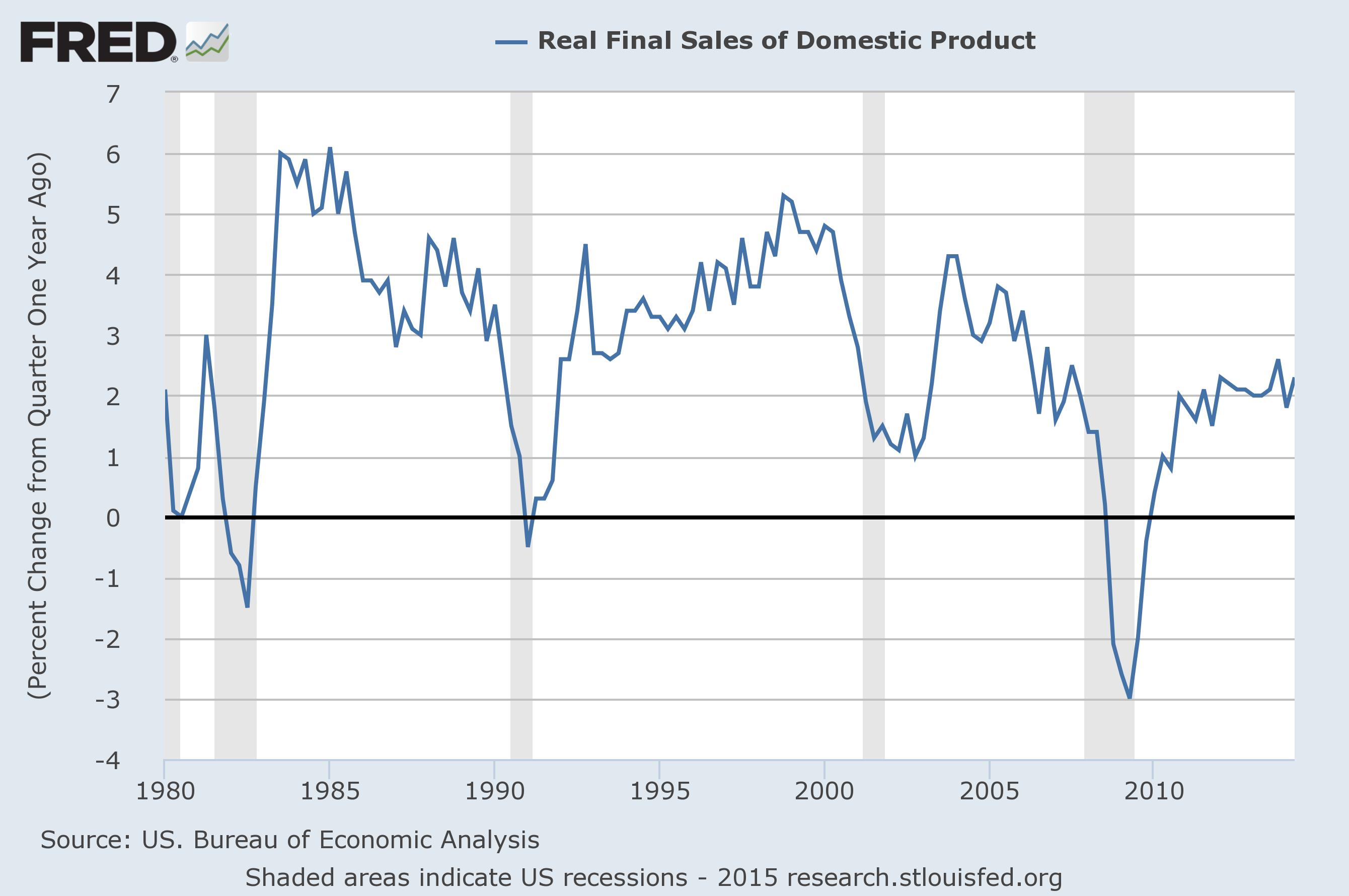

For most experts a key factor that policy makers should be watching is the ratio between actual real output and potential real output. The potential output is the maximum output that the economy could attain if all resources are used efficiently. In Q3 2020, the US real GDP to potential US real GDP ratio stood at 0.965 against 1.01 in Q3 2019.

A strong ratio above 1 can be of concern because according to experts it can set in motion inflationary pressures. To prevent the possible escalation of inflation, experts tend to recommend tighter monetary and fiscal policies. Their preferential policy would be to soften aggregate demand, which is considered as the key driving factor behind the rise in the ratio above 1.

However, of greater concern to most experts is if the ratio falls below 1, which is associated with an economic slump. Most commentators are of the view that with the emergence of a ratio below 1, the most effective policy to lift the ratio above this figure is by means of aggressive fiscal stimulus i.e. the lowering of taxes and increasing government outlays – a policy of large government deficit.

This way of thinking follows the ideas of John Maynard Keynes. Briefly, Keynes held that one could not have complete trust in a market economy, which is inherently unstable. If left free, the market economy could lead to self-destruction.

Hence, there is the need for governments and central banks to manage the economy. Successful management in the Keynesian framework can be achieved by influencing the overall spending in an economy. It is spending that generates income. Spending by one individual becomes income for another individual according to the Keynesian framework of thinking.

What ultimately drives the economy then is spending. If, during a recession, consumers fail to spend then it is the role of the government to step in and boost overall spending in order to grow the economy.

If for whatever reasons the demand for the goods produced is not strong enough this could lead to an economic slump. (Inadequate demand for goods leads to only a partial use of existent labour and capital goods). What is overlooked in this way of thinking is the importance of savings in funding real economic growth. In fact, savings is regarded as detrimental in this way of thinking for economic growth.

Relation between saving and money

Saving as such has nothing to do with money. It is the amount of final consumer goods produced in excess of present consumption.

The producers of final consumer goods can trade saved goods with each other or for intermediate goods such as raw materials and services. Observe that the saved goods support all the stages of production, from the producers of final consumer goods down to the producers of raw materials, services and all other intermediate stages.

Support means that these savings enable all these producers to maintain their lives and wellbeing whilst they are busy producing things. Also, note that if the production of final consumer goods were to rise, all other things being equal, this would expand the pool of real savings and would increase the ability to further produce a greater variety of consumer goods i.e. wealth.

Note that people do not want various means as such but rather final consumer goods. This means that in order to maintain their life people require an access to consumer goods. Only once there has been a sufficient increase in the pool of consumer goods, people may aim at enhancing their wellbeing by seeking other things such as entertainment and services related products – such as medical treatment etc.

Without savings increase in demand is not possible

Note that what matters for economic growth is not just tools and machinery and the pool of labour, but the adequate flow of final consumer goods that maintains individual’s life and wellbeing.

For instance, a baker produces ten loaves of bread out of which he consumes two loaves and exchanges eight loaves for a pair of shoes with a shoemaker. In this example, the baker funds the purchase of shoes by means of the eight saved loaves of bread.

Note that the bread maintains the shoemaker’s life and wellbeing. Likewise, the shoemaker has funded the purchase of bread by means of shoes that maintains the baker’s life and wellbeing.

Consider the event that the baker decides to invest in another oven in order to increase the production of bread. In order to implement his plan, the baker hires the services of the oven maker.

He pays the oven maker with some of the bread he is producing.

What we have here is a situation where the building of the oven is funded by the production of a final consumer good – bread. If for whatever reasons the flow of bread production is disrupted the baker would not be able to pay the oven maker. As a result, the making of the oven would have to be aborted. Now, even if we were to accept that the potential output is above the actual output, it does not follow that the increase in government outlays will lead to an increase in the economy’s actual output.

It is not possible to lift overall production without the necessary support from final consumer goods or the flow of real savings. Observe that by means of a final consumer good – the bread – the baker was able to fund the expansion of his production structure.

Similarly, other producers must have final saved consumer goods – real savings – to fund the purchase of goods and services they require. Note that the introduction of money does not alter the essence of what funding is. Money is just the medium of exchange. It is only used to facilitate the flow of goods it however cannot replace the final consumer goods.

Once real savings are exchanged for money, it is of no consequence what the holder of the money does with it. Whether he uses it immediately in exchange for other goods or puts it under the mattress, it will not alter the given pool of real savings.

How individuals decide to employ their money will only alter their demand for money, this however, has nothing to do with real savings.

Individuals can exercise their demand for money either by holding it themselves or by placing it in the custody of a bank in a demand deposit or in a safe deposit box.

Fiscal stimulus and economic growth

Since the government is not a wealth generating entity, how can an increase in government outlays revive the economy? Various individuals who will be employed by the government will expect compensation for their work. Note that the government can pay these individuals by taxing others who are still generating real wealth. By doing this, the government weakens the wealth-generating process and undermines prospects for economic recovery. (We ignore here borrowings from foreigners).

Now, fiscal stimulus could “work” if the flow of real savings is expanding to support i.e. fund, government activities whilst still permitting a positive growth rate in the activities of wealth generators. If however the flow of real savings is declining then regardless of any increase in government outlays overall real economic activity cannot be revived. In this case the more the government spends i.e. the more it takes from wealth generators, the more it weakens prospects for a recovery.

Thus when the government by means of taxes diverts bread to its own activities the baker will have less bread at his disposal. Consequently, the baker will not be able to secure the services of the oven maker. As a result, it will not be possible to boost the production of bread, all other things being equal.

As the pace of government spending increases, a situation could emerge that the baker will not have enough bread to even maintain the workability of the existing oven. (The baker will not have enough bread to pay for the services of a technician to maintain the existing oven). Consequently, his production of bread will actually decline.

Similarly, as a result of the increase in government outlays other wealth generators will have less real funding at their disposal. This in turn will hamper the production of their goods and services and in turn will retard and not promote overall real economic growth. In this scenario the increase in government outlays leads to the weakening in the process of wealth generation in general.

The above claim that “without savings increase in demand is not possible” is nonsense. I’d have thought it obvious that if government and central bank simply print tons of £10 notes, $100 bills etc and hand them out, the effect will be an increase in demand. Whether that extra money and demand raise inflation too far is an entirely separate matter. They may or may not do. If a large majority of the money is simply hoarded rather than spent, then clearly there’ll be little effect on demand or inflation.