So long as the fiat-based monetary system continues with accelerated money-printing, the US trade deficit will continue to widen. This is due to the lack of a propensity among Americans to save printed dollars, now credited directly into their bank accounts. This will almost certainly lead to demands for further import controls with disruptive consequences for prices.

The continuing deferral of a dollar collapse seems increasingly difficult to achieve, given current and prospective accelerations of monetary inflation. This is coupled with an exceptionally high level of market mispricing, based on current underassessments of price inflation, and heavily suppressed interest rates. While these two distortions have been ignored in the foreign exchanges so far, an increasingly obvious hyperinflation of the dollar will almost certainly lead to markets wresting control of prices from the state in both financial and non-financial elements of the US economy.

Before coming to its conclusions, this article looks closely at the numbers involved, recasting them to last March, when the Fed went all-in on quantitative easing. International trade will be hampered by the progression of a fiat currency collapse, adding to product shortages in America and elsewhere while at the same time consumers will become increasingly desperate rid themselves from excess dollars.

Introduction

With covid lockdowns continuing into the spring and increasingly likely beyond, the economic damage worsens. People everywhere are simply not getting out to spend their money, and businesses which can only plan for their survival under normal trade conditions are pushed back and have lost commercial momentum. Faced with increasing lending risks, their bankers do what they always do in times of trouble — they work to repossess their loans, and any business applying for loan extensions is routinely refused.

Governments have attempted to forestall these problems with special schemes and loan guarantees. In order to save private sector actors from their follies, they are incurring massive debts themselves. The advantage a government has is it can borrow when others cannot, and with its monopoly over the production of money it can create funds through monetary debasement. But even governments have bitten off more than they can chew.

It had become inevitable. When a socialising government takes on cradle-to-grave responsibilities for its citizens it creates a moral responsibility for itself which comes with unlimited cost. Politically, in the choice between protecting the economy and protecting its own system of delivering public services, there can only be one outcome. To protect the government’s administration and bureaucracy, people must give up their freedom to facilitate the government’s crisis management. And oh boy, do we have a crisis!

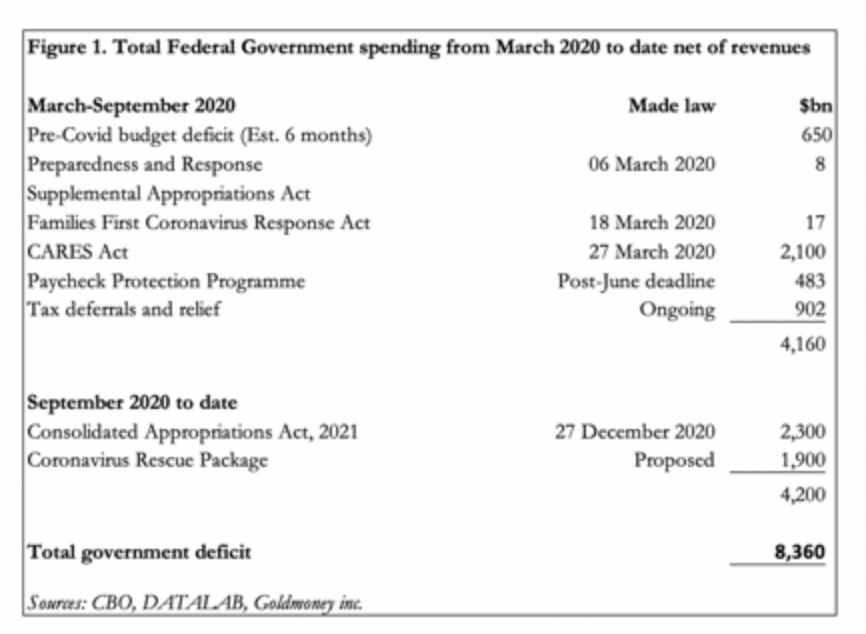

Navigating and financing their way through it, governments are creating numerous economic distortions, which are bound to be unwound by markets at some point. Through quantitative easing financial markets are now awash with money, inflating asset values. And rocketing government deficits have begun to flood money into non-financial markets at an increased pace, while whole industrial sectors are being wiped out by shutdowns. In the US, we can identify budget deficits and ongoing obligations in excess of tax revenue of least $8.36 trillion for the period between March 2020 and today, which is being funded by bond sales. The make-up of these deficits is shown in Figure 1 below.

These deficits are approximately 360% of total on-budget revenues of $2,330bn, all the excess is to be raised in debt markets, almost entirely through quantitative easing by the Fed.

In other words, as fiscal 2021 progresses, it will become increasingly clear the largest economy on earth is in the grip of a hyperinflation of its money supply.

It’s not just the US. All socialising governments, which is more or less all the G20 membership, excepting perhaps China and Russia, are doing the same thing — deliberately creating enormous financial deficits while locking down their economies. What started as a one-off support bridging from a pre-covid normal to a post-covid resumption of normality, the covid crisis is turning out to be an infinite and escalating commitment with an uncertain ending. It is not something that governments can abandon easily because of those cradle-to-grave welfare commitments.

We have not yet started the Keynesian stimulus to rescue the global economy from a seemingly inevitable slump, and the promised spending on pet projects such as green energy. Even the IMF is exhorting all governments to throw all caution to the winds and to spend, spend, and spend again.

The slide into this hyperinflationary condition started last March, when European countries, including the UK, first went into lockdowns. America was only a short step behind, and the Fed was forced into an inevitable response by cutting its funds rate to zero and instituting monthly QE of at least $120bn. Consequently, the US Treasury’s account at the Fed has accumulated a balance of unspent funds totalling $1.6 trillion to be offset against future spending, and therefore future funding requirements.[i]

Even allowing for this reserve, financial markets will now need to find $325bn every month to invest in Treasury bonds to cover the remaining unfunded budget deficit to the end of the current fiscal year. Any of this funding which is not obtained through QE will divert funds from the private sector, crowding it out of financial markets and collapsing much of production in the highly indebted non-financial economy. That cannot be permitted, so we can assume the entire burden of government deficit funding will fall directly or indirectly on the Fed’s shoulders. And together with monthly QE for agency debt, this means that QE is likely to rise to a monthly average of over $360bn from now on until the fiscal year-end.

Goodness only knows the scale of funding required after that. The Keynesians hope that additional monetary stimulus (not yet factored into these figures — they are just to rescue Americans from covid lockdowns) will turn the US economy round and encourage investment inflows. They fail to allow for the fact that rapidly accelerating monetary inflation is a debilitating wealth transfer from the productive economy to generally unproductive government spending. Instead of stimulating the economy, debauching the currency bankrupts it. And no foreigner will contemplate investing in a currency which is being so obviously debased against the commodities they are accustomed to purchase with it for their production. If anything, they will reduce their holdings of dollars for something that to them is needed and better retains its value.

Led by China, foreigners are now stockpiling commodities

We see this with the Chinese state stockpiling and hoarding commodities, a policy implemented soon after the Fed announced its inflationary policies last March. China also changed its exchange rate policy of suppressing its currency’s exchange rate against the dollar to advance the competitiveness of its exports, to one of allowing the yuan to increase relative to the dollar. We can take this as evidence China is abandoning the dollar as a currency with renewed vigour, though it will take some time to fully do so. In yuan terms, the cost of buying essential commodities such as copper and agricultural produce such as soybeans has been reduced thereby by nearly 10%.

Commodities are being more widely stockpiled, as the evidence of prices listed in Figure 2 below confirms. China has already cornered the physical gold market and, we can therefore believe, possesses enormous undeclared reserves of sound money and needs to take little further action. That being the case, she has ample insurance against a dollar collapse, which is why her hoarding is now of commodities. The wisdom of this policy is illustrated in Figure 2, which shows how prices for commodities and other inflation hedges have moved measured in dollars from the time the Fed accelerated its inflationary policies.

Clearly, it’s not just the Chinese government rejecting depreciating dollars. Cryptocurrencies, commodities, equities and other currencies are all finding favour from private sector actors ditching dollars, even though they are mostly unaware that that is in effect what they are doing.

Impact on trade

With a low and stable level of savings, the US budget deficit remains broadly matched by a trade deficit. But in coronavirus lockdowns, the savings rate has at least temporarily risen. This is a reflection of the fall in consumer spending and the helicopter drop of $600 per adult approved by congress last month and distributed recently, as well as the previous one of $1200. President Biden has proposed a further $1400 helicopter drop as part of his $1.9 trillion coronavirus relief package, which initially will boost the savings rate. These payments will total $3,200 per adult, a direct injection into consumers hands of about $670bn. On top of these payments, Congress’s December relief package adds a further $300 per week to the jobless, which Biden intends to increase to $400.

If that money stays saved, then relative to the budget deficit the trade deficit will fall, though in absolute terms it would almost certainly rise, because the helicopter drops amount to significantly less that the total budget deficit shown in Figure 1.

What happens to that $3,200 of money, which is additional to consumer earnings from their production, is important. If some of it is saved, then it should find its way into predominantly non-fixed interest financial securities, perhaps evidenced by the extraordinary price activity in stocks currently targeted by small investors. Some of it will pay off debt, reducing outstanding consumer credit. The remainder will be spent following lockdowns, because consumers naturally maintain a balance between liquidity and spending, disposing excess cash. And when that cash is spent it can be expected to lead to a surge in imports.

Excessive consumer liquidity leads to demand for imported goods for two reasons. First, consumer spending is artificially boosted while production does not immediately respond. In a closed economy, the effect on prices from this imbalance can be dramatic. Secondly, in an open economy demand for imported substitutes increases, because of higher prices for goods in short supply from domestic producers. It follows therefore that political attempts to restrict the level of imports simply drives up the general level of prices.

The origin of those imports is a separate matter. Until last March, the Chinese were content to manage their currency lower against the dollar, making them always the preferred source of imported goods for American consumers. But the table in Figure 2 above shows that the only major currency to rise less against the dollar than the yuan since March is the Japanese yen. So long as that relationship holds, Japanese exporters will have gained a marginal price advantage.

The difference so far is unlikely to make a huge difference to the profitability of China’s exports to the US, so an exploding US budget deficit will still lead to a substantial increase in imports from China. This trend is bound to result in more protectionist measures from the American government, which will have the effect of increasing domestic prices of goods and services even more. The role of tariffs and other means of trying to control imports is economically destructive, proved by the depression following the Smoot-Hawley Tariff Act and the Wall Street crash in 1929—32. Yet, like price controls, tariffs always prove irresistible to politicians.

The difference from the great depression this time is in the pricing: ninety years ago, prices were in sound money — gold, through the medium of the dollar. This time it is in unbacked fiat. Combine the inflationary flood of fiat and the collapse of domestic productive capacity relative to consumer demand, and the inevitable consequences will be a radical loss in the purchasing power of the currency.

This outcome appears to be totally unexpected by the inflationists, who insist that stimulating demand by money-printing is the go-to solution. Unwisely, they rejected Say’s law, which explains that the role of money in transactions is to simply act as the facilitator for turning everyone’s production into their desired consumption. It follows that any attempt to interfere with this vital function by substantial monetary expansion is doomed to be economically disruptive.

This analysis conforms with the Austrian school’s text-book progression of inflation-driven events, theorised and written before and during the European inflations in the early 1920s. Despite the dominance of inflationary monetary policies today, the writings of economists such as Ludwig von Mises, Eugen Böhm-Bawerk and Friedrich Hayek still resonate. But we might not have the dubious luxury of seeing events play out in the manner they described. Instead, monetary policy today has been targeted at inflating financial assets to produce an artificial wealth effect, hyping things up to seem better than they really are. But it is simply market mispricing. And when it occurs, the fall from the promise of statist management of asset values into the depths of market reality is always rapid. At the end of the day markets always win, and the state always loses.

It is possible to find that at any time complacent presumptions that tomorrow’s outlook will be unchanged from yesterday’s events will be expensively wrong. Instead, everything can rapidly move from stability onto the verge of collapse. Have we forgotten the moment when Hank Paulson got down on one knee before Nancy Pelosi, and begged her to allow his $700bn bail-out plan to save the financial system?

That was in September 2008. Today the situation is immeasurably worse, with very little of the market distortions that led to that crisis resolved in the last ten years. Zombie corporations have multiplied along with their debts. Despite socialist accusations of austerity, government spending has continued to increase. The inflation of asset prices by printing money has only served to cover up the cracks.

If the financial and economic distortions fail under pressure from market reality, we can expect international trade to more or less cease, because no one will want payment in a collapsing value of the global trade settlement currency. Foreign holders of dollar-denominated assets will then rapidly turn sellers and attempts to raise their dollar cash balances to add to their existing bank deposits of roughly $6.5 trillion will only accelerate a stampede out of the dollar.

The consequences of the Fed’s loss of control over markets

If we should remind ourselves of one aphorism about markets, it is that when the state embarks on a policy of managing markets, it will eventually fail. The distortions created by the state are then unwound uncontrollably. The greater the distortions, the greater and more sudden the readjustment. The world saw this when the iron curtain across Europe was dramatically demolished by ordinary people. That event ended seventy years of communist control over the people in only a few days. While it must be admitted that government control over people and their economic actions can persist for many decades, there is always a time when it must end.

The rapid acceleration of money printing by the Fed, and the growing realisation it will accelerate even further, gives us an indication that the current fiat regime is now close to an end. The violence of the return to market-driven prices becomes the outstanding issue. And echoing communism, the state has controlled both the statistical information and the prices of financial assets. To assess the height of these distortions we must ignore those government statistics which we know to be incorrect.

Key among these is the manipulation of consumer price indices upon which monetary policy is based. Independent compilers of price inflation statistics confirm that prices have been rising in the US at closer to 10% annually than the current 1.4% as stated by government statistics. And that is before the impact on prices of current inflationary financing of the government deficit.

Clearly, from the authorities’ point of view the acceleration of monetary inflation should be exceptionally dangerous, with the potential to collapse the state’s pricing illusions and bring about a return to market reality. And given that the calculation methods for the CPI are in an internationally standardised framework, what is true for fiat dollars becomes true for other fiat currencies as well.

For now, we must confine our analysis to the US dollar and its markets, because they are the standard for everything else. The overriding issue facing all holders of dollars is current interest rates, and of what should be the dollar’s rate of time preference. If tomorrow’s dollar buys goods and services that are genuinely rising at the BLS’s CPI estimated 1.4%, then its time-preference gives a future approximate annualised value of 98.6 cents to the dollar assuming that that is the rate of loss of purchasing power for dollars in the foreseeable future. That 13-week Treasury bills yield only 0.068% is a further distortion on the CPI-suggested rate of loss of the dollar’s purchasing power.

But we know from independent analysis that the true rate at which the dollar’s purchasing power is changing and has been for most, if not all of the last decade, is in the region of losing ten per cent for every year. That being the case, the annualised level of time preference becomes 90 cents on the dollar, before other considerations are taken into account. It now becomes easier to anticipate the scale of damage to financial values that will occur when this discovery takes place.

Those likely to be most sensitive to this discovery are foreign investors and other temporary holders of the dollar. But pressure to increase interest rates are bound to be strongly resisted by the US authorities, which can only accelerate the fall in the dollar’s purchasing power even further. The rate at which this is reflected on the foreign exchanges depends on the extent to which similar statist distortions apply to the other currencies. But we can now see that interest rates are the crucial link between a fall in financial asset values and a collapse in the purchasing power of fiat currencies.

Government finances are also severely affected, and the Fed’s ability to fund them through QE, which is taken for granted, becomes questioned. Once markets become forward looking again, as opposed to complacently assuming what was good yesterday holds for tomorrow, the state’s dependency upon hyperinflationary financing will rapidly undermine the dollar even further. An annualised rate of time preference of 90 cents for today’s dollar will change to both the currency’s detriment and to those of all dollar-based financial assets.

Meanwhile, the rolling over of private sector corporate debt in an economy that has supported corporate zombies for at least the last two bank credit cycles creates an additional crisis, certain to undermine stock market values beyond those implied by rising interest rates alone.

In these conditions, international trade, which is the only offset to rapidly rising domestic prices for the US consumer, will become restricted by importers’ reluctance to accept dollars without selling them for forward settlement on the exchanges. For this to happen requires the fiat-based financial system to continue to function normally, despite a dollar collapse. This takes us into an analysis of the global banking system, which we must leave for another day. But suffice to say, not only are global banks trying to reduce their exposure to covid-suffering borrowers, but some banking systems, notably that of the Eurozone, are unlikely to survive the rise in interest rates and therefore the collapse in financial asset values that will accompany them.

The relationship between gold and fiat

It is a mistake to view gold in terms of fiat currency prices, which will become obvious when fiat money loses its role as the objective value in transations. As the only empirically confirmed sound money selected by its users, metallic money, which can also be taken to include silver and copper, is the only form of money to which everyone will revert after the death of fiat. It is therefore more appropriate to price fiat currencies in terms of gold, which exposes more obviously the collapse in their purchasing power.

Instead of suggesting, perhaps, that the price of gold might double, it becomes easier conceptionally to understand that the purchasing power of a fiat currency halves. We can illustrate the point by looking at the relationship between sound money, gold, and fiat money over time. When President Nixon abandoned the gold peg in August 1971, gold was priced at just under $36. Today it is $1840, having risen fifty times. This is meaningless. But turn the relationship the other way round, and we can say that relative to gold the dollar has lost over 98% of its purchasing power, and then an understanding of the true state of affairs between sound and fiat money emerges.

Conclusion

The acceleration of monetary inflation for the US dollar identified in this article comes on top of the long-established suppression of evidence of price inflation and the clampdown on interest rates. Inevitably, this will bring forward the day when markets take back control of both financial asset values and interest rates from the authorities. The consequences are both many and catastrophic. Government finances, already dependent on the hyperinflation of the dollar, will rapidly deteriorate even further and markets will then compound the authorities’ difficulties by trying to discount further falls in purchasing power.

Just as the ending of communist control of markets ended with the fall of the iron curtain in a matter of only days, the height of fiat money distortions is so far above market reality that the effects are likely to be equally profound. It is increasingly certain to lead to the rapid ending of the fiat currency regime, and the collapse of international trade for lack of a payments medium.