By Dr Frank Shostak

For most commentators lending is associated with money. However, is this the case? We suggest that a lender lends savings to a borrower and not money as such. When a saver lends money, what he/she in fact lends to a borrower is final consumer goods that he/she did not consume.

Take a farmer Joe that produced two kg of potatoes. For his own consumption, he requires one kg, and the rest he agrees to lend for one year to a farmer Bob. The unconsumed one kg of potatoes that he agrees to lend is his savings.

By lending one kg of potatoes to Bob, Joe has agreed to give up for one year the ownership over these potatoes. In return, Bob provides Joe with a written promise that after one year he will repay 1.1kg of potatoes. The 0.1kg constitutes an interest. Note that the existence of savings is the precondition for lending (there must be savings first). Savings must fully back up lending.

What we have here is an exchange of one kg of present potatoes for 1.1kg of potatoes in one-years’ time. Both Joe and Bob have entered this transaction voluntarily because they both have reached the conclusion that it would serve their objectives.

The introduction of money will not alter the essence of what lending is all about. Instead of lending directly the one kg of potatoes Joe can first exchange these potatoes for money, let us say for $10. Joe then lends the $10 to Bob for one year at the going interest rate of 10%. Note that money here fulfills not only the role of the medium of exchange but also the role of the medium of savings. Joe’s savings of one kg of potatoes is stored so to speak in the form of money of $10.

Observe that the introduction of money did not change the fact that savings precede the act of lending. Note that savings support individuals in the various stages of production. Hence, savings are the heart of economic growth. It follows then that the lending of savings fulfills an important role in the process of wealth generation. By means of lending his savings to Bob, the lender Joe provides the means of sustenance to Bob the borrower. This in turn makes it possible for Bob to engage in a wealth generating activity.

Introducing banking

Rather than searching by himself for potential borrowers, Joe could approach an organization that specializes in finding borrowers. This organization is a bank. The bank specializes in finding borrowers to individuals that are willing to lend their savings. Bank also specializes in finding lenders to individuals that are willing to borrow. From this, we can infer that bank fulfills the role of an intermediary. (Note that banks rather than fulfilling the mediator’s role could also engage in direct lending by using their own equity funds or by borrowing the required funds).

In addition, the bank also provides facility for storing money in demand deposits. An individual can exercise his/her demand for money by holding the money in his/her wallet, holding it at home or storing it in a demand deposit, which was provided by the bank. By storing, his/her money in a demand deposit an individual retains an unlimited claim over the deposited money – it is his possession. (Note that the saved one kg of potatoes is stored in the form of $10 in demand deposit).

If the owner of the demand deposit were to decide to lend part of the stored money then he/she is likely to inform the bank in this regard by transferring part of the money stored in the demand deposit to a term deposit. (Note that what effectively is transferred here is part of the saved quantity of potatoes that was stored in the form of money in the demand deposit).

Banks are offering various lending selections to potential lenders such as Joe through various term deposits. The bank can offer Joe to lend his money from a very short period to a very long period by allowing Joe to place his money in corresponding term deposits. For instance, if Joe decides to lend $5 for one year at the market interest rate he could transfer this amount to the one-year term deposit. This also, means that Joe has agreed to relinquish the ownership over the $5 for one year. Now, it is up to the bank to find a suitable borrower. Observe that savings are fully back up lending here. Trouble however, emerges once banks are starting to engage in lending without the support from savings.

Lending unbacked by savings results in economic impoverishment

Again, if Joe were to decide to lend $5 for one year, we would have a transfer of $5 from Joe’s demand deposit to a one-year term deposit. The money in the one-year term deposit can be lent out for one year. (The one-year term deposit of $5 backs the one-year loan of $5 here).

Let us consider a case when Bob approaches Bank A for a loan of $5 for one year. Bank A accommodates this request and lends Bob the $5 by placing the money in the newly established demand deposit. Also, note that we did not have a transfer of $5 from the holders of demand deposits such as Joe to the one-year term deposit. As a result the loan to Bob is unbacked by savings. What we have here is that Bank A has generated the $5 loan out of “thin air”. The bank here established a demand deposit to the tune of $5 without the backing from savings. Contrast this with the case when Bank A opened a demand deposit to Joe who has placed his saved $10 in the demand deposit.

Once Bob the borrower of the $5 uses the unbacked by savings money, which Bank A generated out of “thin air”, Bob is engaging in an exchange of nothing for something. This is because savings do not back up the $5 – it is empty money. In an unhampered market economy, a bank runs the risk of bankruptcy if it were to issue loans out of “thin air”. According to Rothbard,

As soon as the new money ripples out to other banks – the issuing bank is in big trouble. For the sooner and the more intensely clients of other banks come into picture, the sooner will severe redemption pressure, even unto bankruptcy, hit the expanding bank.

The reason being for the likely bank bankruptcy is because the bank issuing loans out of “thin air” does not have enough money to clear its checks during the interbank settlements. Consequently, in an unhampered market economy, without the central bank, competition between banks is likely to minimize the lending out of “thin air”. On this Mises wrote that,

People often refer to the dictum of an anonymous American quoted by Tooke: “Free trade in banking is free trade in swindling”. However, freedom in the issuance of banknotes would have narrowed down the use of banknotes considerably if it had not entirely suppressed it. It was this idea which Cernuschi advanced in the hearings of the French Banking Inquiry on October 24,1865: “I believe that what is called freedom of banking would result in a total suppression of banknotes in France. I want to give everybody the right to issue banknotes so that nobody should take any banknotes any longer’.

It must be realized that the likelihood of bankruptcy increases when there are many competitive banks. As the number of banks increases and the number of clients per bank declines, the chances that clients will spend money on goods from individuals that are banking with other banks will increase. This in turn will increase the risk of the bank not being able to clear its checks once the bank begins the practice of issuing loans out of “thin air”. Conversely, as the number of competitive banks declines, that is as the number of clients per bank rises, the likelihood of bankruptcy diminishes. In the extreme case of one bank, it can practice the lending out of “thin air” without any fear of bankruptcy.

We suggest that the act of lending out of “thin air” is likely to become sustainable occurrence in the framework of the central bank. The central bank by means of the daily money supply management i.e. monetary pumping prevents banks bankrupting each other.

According to Rothbard,

The Central Bank can see to it that all banks in the country can inflate harmoniously and uniformly together……In short, the Central Bank functions as a government cartelizing device to coordinate the banks so that they can evade the restrictions of free markets and free banking and inflate uniformly together.

Lending out of “thin air” causes the disappearance of money and sets platform for non-productive activities

When loaned money is fully backed by savings on the day of the loan’s maturity, it is returned to the original lender. Bob – the borrower of $5 – will pay back on the maturity date the borrowed sum and interest to the bank. The bank in turn will pass to Joe the lender his $5 plus interest adjusted for bank fees. The money makes a full circle and goes back to the original lender. Note again that the bank here is just a facilitator; it is not a lender so the borrowed money is returned to the original lender.

In contrast, when lending originates out of “thin air” and is returned on the maturity date to the bank, this leads to a withdrawal of money from the economy i.e. to the decline in the money supply. The reason being because in this case we never had a saver/lender, since this lending emerged out of “thin air”. Note that savings do not support the newly formed demand deposits here. Now, when Bob repays the $5, the money leaves the economy since there is no original lender to whom the loaned money should be returned – the bank has created the $5 loan out of “thin air”.

Observe that the $5 loan out of “thin air” is a catalyst for an exchange of nothing for something. This provides a platform for various non-productive activities that prior to the generation of lending out of “thin air” would not have emerged. As long as banks continue to expand lending out of “thin air”, various non-productive activities continue to flourish. Because of the continuous expansion in the lending out of “thin air”, the pace of wealth consumption is starting to increase above the pace of wealth production. The positive flow of savings is arrested and a decline in the pool of savings is set in motion.

Consequently, the performance of various activities starts to deteriorate and banks’ bad loans start to increase. In response to this, banks curtail their lending out of “thin air” and this in turn triggers a decline in the money supply. A decline in the money supply begins to undermine various non-productive activities i.e. an economic recession emerges. According to a popular view championed by Milton Friedman, a severe economic slump also known as economic depression emerges because of the strong decline in the money supply.

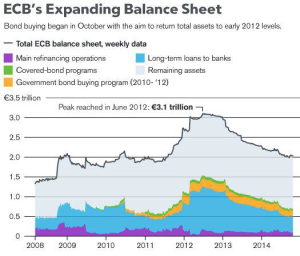

Therefore, it is the duty of the central bank to pump massive amount of money to prevent the economic depression. In fact, this is what the Bernanke’s Fed did during the 2008 economic crisis.

We suggest that an economic depression is not caused by the decline in the money supply as such, but comes in response to the shrinking pool of savings because of the previous easy monetary policies. The shrinking pool of savings leads to the decline in economic activity and in turn to the decline in the lending out of “thin air”. This in turn results in the decline in the money supply.

Consequently, even if the central bank were to be successful in preventing the decline in the money supply, this cannot prevent an economic depression if the pool of savings is declining. (Note, the heart of economic growth is the expanding pool of savings).

Again, we hold that banks’ ability to generate lending out of “thin air” is on account of the central bank easy monetary policies. In the absence of such institution, the likelihood of banks practicing lending out of “thin air” is going to be very low.

Conclusions

Banks facilitate the flow of savings by introducing the ‘suppliers’ of savings to the ‘demanders’. In this sense by fulfilling the role of the intermediary, banks are an important factor in the process of wealth formation. Once however, banks abandon their role as intermediary and starting to lend money not backed up by savings this sets in motion the menace of the boom-bust cycle and an economic impoverishment.