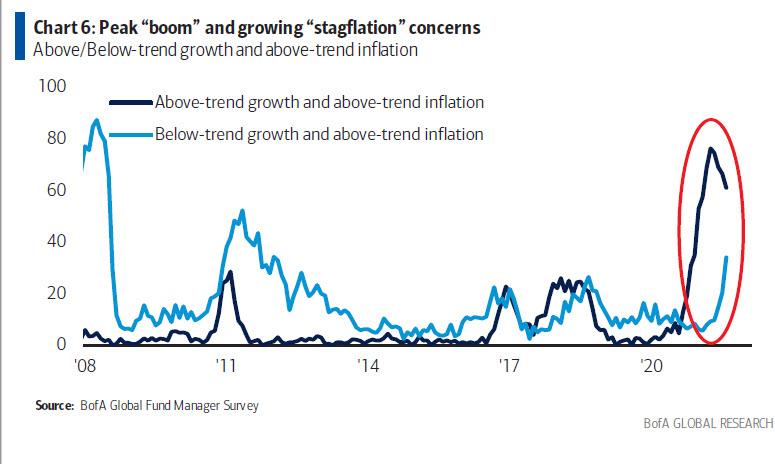

Now that the fear of stagflation is a growing concern on Wall Street as the latest BofA Fund Manager Survey showed…

… as the inflation debate – at a time of shrinking global growth – has taken on renewed vigor given the latest commodity price surge over recent weeks, the energy shocks and discussions around stagflation have led many to make the comparison to the 1970s not just on this site…https://platform.twitter.com/embed/Tweet.html?dnt=false&embedId=twitter-widget-0&features=eyJ0ZndfZXhwZXJpbWVudHNfY29va2llX2V4cGlyYXRpb24iOnsiYnVja2V0IjoxMjA5NjAwLCJ2ZXJzaW9uIjpudWxsfSwidGZ3X2hvcml6b25fdHdlZXRfZW1iZWRfOTU1NSI6eyJidWNrZXQiOiJodGUiLCJ2ZXJzaW9uIjpudWxsfSwidGZ3X3NwYWNlX2NhcmQiOnsiYnVja2V0Ijoib2ZmIiwidmVyc2lvbiI6bnVsbH19&frame=false&hideCard=false&hideThread=false&id=1387217537700671491&lang=en&origin=https%3A%2F%2Fwww.zerohedge.com%2Fmarkets%2Fstagflation-here-comparing-2020s-1970s&sessionId=867fbcc0bca7a50f70d12f2886ab7c8643d4e7ca&siteScreenName=zerohedge&theme=light&widgetsVersion=f001879%3A1634581029404&width=550px

… but elsewhere:

- Paul Tudor Jones, CEO of Tudor Investment Corp., tells CNBC that inflation is the single biggest threat to the economy: “The inflation genie is out of the bottle and we run the risk of returning to the 1970s” – CNBC

- Is Stagflation Coming Back? Economist Sees Parallels With the 1970s—and Big Differences – Barrons

- Is the world economy going back to the 1970s? – The Economist

- What the Inflation of the 1970s Can Teach Us Today – WSJ

- Conditions are ripe for repeat of 1970s stagflation – Guardian

- Ignore the fearmongers: the 1970s are not coming back – Guardian

- A Stock Market Malaise With the Shadow of ’70s-Style Stagflation – NYT

Addressing these growing comparisons between the 2020s and the 1970s, last week Deutsche Bank’s credit strategists Henry Allen and Jim Reid looked into some of the similarities and differences between that infamous inflationary decade and today. Below we summarize some of the key observations made by the duo, who looked at how the 1970s evolved from an inflationary perspective and compare and contrast to today.

We start by reminding readers that things were very bad in the 1970s….

As Deutsche Bank writes, TV screens in the UK have recently shown scenes of long lines for gas across the vast majority of fuelling stations. Initially, this wasn’t about a shortage of fuel, but a shortage of HGV drivers that fed upon itself to become a fuel shortage amidst a demand surge as well. Right now, we’re still a long way from what we saw in the 1970s, when there were big reductions in the supply of energy, but the recent rise in global gas prices could be much more troublesome going forward. Across the globe, fuel rationing took place for a period of time back then, and governments ran huge media campaigns to conserve energy. President Nixon asked gas stations not

to sell gasoline on Saturday or Sunday nights, and eventually license plate restrictions (odd and even) were in place in the US for when you could buy fuel. In Europe, some examples of the stresses included a ban in the Netherlands on Sunday driving, whilst the UK imposed a 3-day week as coal shortages threatened electricity supplies alongside a winter series of strikes by coal miners and rail workers. Households were asked to heat only one room in their homes.

so we need to put into perspective how bad things got for individuals and economies due to the energy issues. The recent gas problems have raised the prospects of a winter where rationing could take place but this is speculation for now. However, the spikes in gas prices are reminiscent of what happened with oil in the early 1970s (both have a geopolitical angle too) so some historical awareness is useful.

How did inflation get out of control in the 1970s?

Today’s situation has a number of parallels to what happened in the 1960s and 1970s, when inflation gradually accelerated to the point where it was out of control. Various shocks coalesced over a short period of time, and policymakers were consistently behind the curve in reacting:

- In the US, the Johnson Administration’s Great Society programs and the Vietnam War drove up fiscal spending in the late-1960s.

- In 1971, President Nixon ended the dollar’s link to gold, ending the system of fixed exchange rates that had prevailed after the Second World War.

- An El Nino event in 1972 drove up food prices.

- The dollar underwent a devaluation in February 1973.

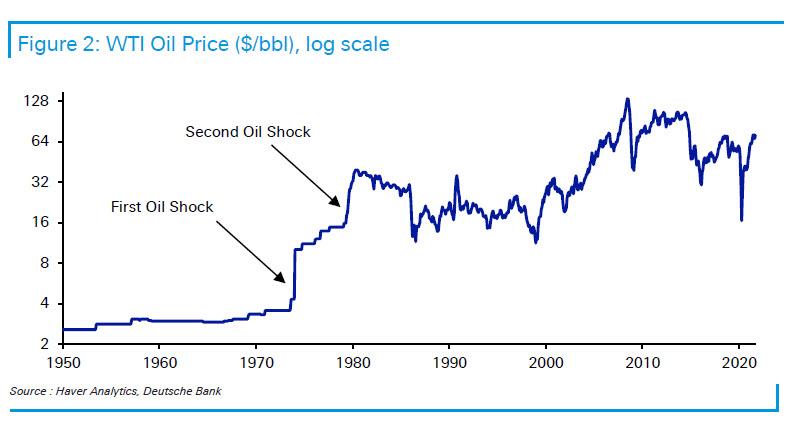

- Then on top of all this, the first oil shock occurred in 1973, followed by a second oil shock in 1979.

Even though the commodity shocks are generally held most responsible for the high inflation over the period, it’s clear that inflation was already embedded in the system well before they occurred. So if you were keeping a strict timeline you could argue that when it comes to economic policy being more expansionary, we’re more in the late-1960s than the 1970s. Perhaps Covid has made the timeline more compressed, but inflation steadily moved from under 2% in the first half of the 60s to over 6% by the end of the decade.

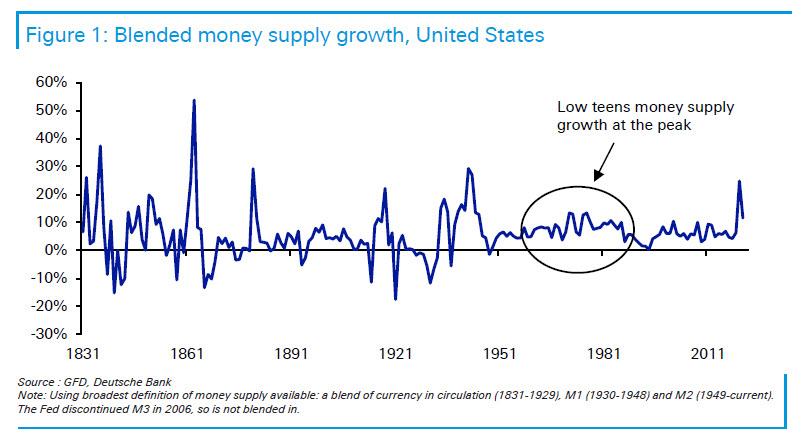

The inflationary set up in the 70s then deteriorated thanks to the suspension of the dollar’s convertibility into gold in 1971. Given that virtually every other currency was fixed to the dollar at the time, we quickly moved from a world of gold-based money to one where fiat money was in control. Interestingly, Figure 1 shows that with this loosening of policy constraints, the YoY percentage growth in monetary aggregates moved consistently into the low teens from high single digits in the late 1960s.

Today, we’ve moved from pre-covid mid-single digit YoY percentage growth to a brief period of 25% YoY growth at the peak. Even if we revert back to single digit percentage growth there’s still a large residual amount of liquidity in the economy far above that assumed by the pre-covid trend. So there’s been a faster injection of money into the economy in the space of a year than we saw at any point in the 1970s.

But even as inflation continuously accelerated through the late-1960s onwards, central bankers found it difficult to shift policy in a hawkish direction. This was partly down to political pressure, both explicit and implicit, since politicians were not keen on the idea of a slowdown in growth and higher unemployment. It was also down to a poor understanding of the economy – with policymakers wrongly believing in the Phillips Curve, and the belief that it was possible to “buy” lower unemployment with higher inflation, when this wasn’t actually true over the long term.

We can see some of this pressure in action by looking back through the archives. The following quote comes from the Fed’s senior economist, J. Charles Partee, in the memorandum of discussion from the March 1973 FOMC meeting. He said that “To adopt a substantially more restrictive policy that carries with it the danger of stagnation or recession would seem unreasonable and counterproductive. As unemployment rose, there would be strong social and political pressure for expansive actions, so that the policy would very likely have to be reversed before it succeeded in tempering either the rate of inflation or the underlying sources of inflation.”

So even the Fed’s economists at the time were acknowledging the “social and political pressure” under which they were operating. One more recent academic paper by Charles Weise (2012) actually found that references at FOMC meetings to the political environment were correlated with the stance of monetary policy, which further suggests it was having an impact on decision-making.

Another serious issue was that the Fed was operating with a poor understanding of the available data. Orphanides (2002) notes that errors in the assessment of the natural rate of unemployment meant policymakers believed that the economy was operating beneath potential. So that helped to justify lower interest rates than prevailed in reality. Had they actually realized the situation as it prevailed at the time, then perhaps they would have pushed more strongly for a hawkish stance. So a number of factors were pushing inflation higher. But what turbocharged it into double-digits in the US were two major oil shocks, which had ramifications across the entire developed world?

1973: The First Oil Shock

The first oil shock was triggered by the Organization of Arab Petroleum Exporting Countries (OAPEC) placing an embargo on a number of countries, including the United States, in retaliation for their support for Israel in the Yom Kippur War. There is also some evidence that the US abandoning the convertibility of the dollar into gold, which led to a big devaluation of the dollar, and a loss of income for oil producers, helped create resentment from this group.

Regardless of the cause, this led to a quadrupling in oil prices, triggering a recession across multiple countries that began in late 1973. Inflation was already running at a decent clip, but this turbocharged it, with CPI peaking at 12.2%, which was the highest it had been since the immediate aftermath of WWII.

This, as Deutsche Bank notes, posed a tricky dilemma for the Federal Reserve. Although the inflation rate was high and rising, unemployment was also climbing at the same time. So hiking rates to deal with inflation risked exacerbating the unemployment situation. This scenario is completely unlike what happened after the GFC in 2008, which was a big deflationary shock, making it clear which way the Fed needed to move rates.

At the time, the view was that the embargo was a structural shock that monetary policy couldn’t affect, so it should therefore look through such a transitory factor (this should ring a few bells). For a fly-on-the-wall view, Stephen Roach, who’s now a Senior Fellow at Yale but was formerly on the research staff at the Fed, said that Fed Chair Burns argued that as the shock had nothing to do with monetary policy, the Fed should exclude oil and energy-related products from the CPI index for its analysis. Roach then said Burns insisted on removing food prices in 1973 after unusual weather. This too should ring bells… and alarms.

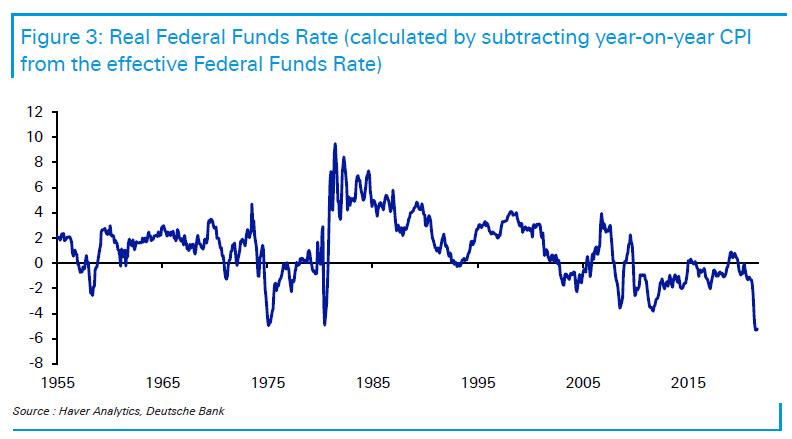

The exclusions of these “transitory” factors became so extreme that Roach estimates that only 35% of the CPI basket was left. By the middle of the decade this series itself was then rising at a double-digit rate. You can get a sense of how loose policy was here by looking at the real Federal Funds rate, which moved into negative territory as a result of the oil shock. Interestingly, the real rate is now even lower than it was at any point in the 1970s.

To be fair to the Fed, at the start of the energy shock it would have been tough to know how the situation would develop. The record from the December 1973 Fed meeting says: “On balance, the Chairman concluded, he believed that some easing of monetary policy was indicated today, but that it should take the form of a modest and cautious step. He was aware of the possibility that the oil embargo might not last more than another few weeks. On the other hand, the embargo might last another year.” So although we can view events with a detached level of hindsight, with the knowledge of how they played out, they were living through this in real time.

As it happened, the embargo lasted until the following March, but the long-term effects are still with us today. The shock had revealed the dependence of the United States and others on foreign oil, so an emphasis was placed on reducing that dependence. That saw the Strategic Petroleum Reserve created in the US in 1975, which is a tool that today’s Energy Secretary has said is under consideration to deal with the present energy price surge. Then in 1977, the Department of Energy was created, which is also with us to this day.

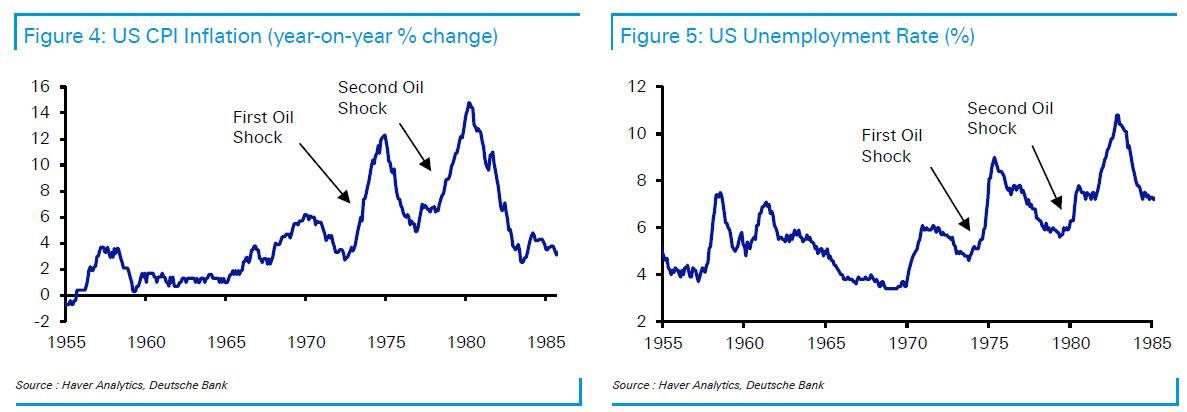

As Figure 4 shows, US inflation did come down again once the worst of the first oil shock had passed. But it only fell back to around 5% before picking up again, whilst monetary policy still remained fairly accommodative to deal with high unemployment (Figure 5), which in December 1976 stood at 7.8%.

This was partly because there was still political pressure on the Fed. The Carter Administration arrived in office at the start of 1977, and in the transcript of the FOMC meeting that January, Chairman Burns said “We have a new Administration; the new Administration has proposed a fiscal plan for reducing unemployment, and any lowering of monetary growth rates at this time would, I’m quite sure, be very widely interpreted–and not only in the political arena–as an attempt on the part of the Federal Reserve to frustrate the efforts of a newly elected President and newly elected Congress to get our economy, to use a popular phrase, “moving once again.”

Fast forward to today and although there isn’t the same level of political concern, the Fed have recently undertaken a dovish shift following their recent policy review. Their move towards average inflation targeting is an explicit acknowledgement that they’re willing to accept above-target inflation to make up for past undershoots. Furthermore, they have adopted a much more tolerant view on the risk of

inflationary pressures from low unemployment, and officials regularly discuss distributional issues such as economic performance for those on low incomes or minority groups. So it’s clear that the Fed’s reaction function has changed relative to where it was just a few years ago.

1979: The Second Oil Shock

Back to the 70s and just as the economy was recovering from the effects of the 1973 shock, a second oil shock in 1979 sent inflation sharply higher once again. This took place around the time of the Iranian revolution, which coincided with a big decline in Iranian oil output, to the tune of around 7% of global production at the time. Then in 1980, the Iran-Iraq War caused further declines in production for both countries.

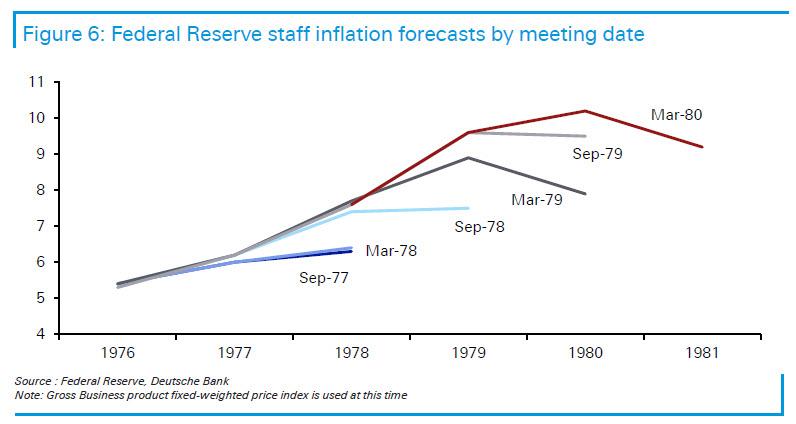

Although plenty blame the oil shock for creating high inflation, the truth was that this was merely the final nail in the coffin for the old regime, since in the preceding years, the Fed had persistently underestimated how high inflation would rise. The next chart shows that the Fed’s staff forecasts were repeatedly upgraded as time went on, even prior to the second shock.

Unlike in 1973 however, this shock induced a much more hawkish policy response from the new Fed Chair Paul Volcker. Indeed, the transcript from Volcker’s first meeting as Fed Chair in August 1979 shows him pointing to higher inflation expectations that had developed, saying that “I think people are acting on that expectation [of continued high inflation] much more firmly than they used to.” And Volcker also recognized that restoring the credibility of economic policy could also “buy some flexibility in the future”.

Although higher rates were a contributory factor behind the recession that began in early 1980, this new pro-active approach was successful at containing inflation, which fell from a peak of 14.6% in March 1980, down to 2.4% in July 1983. The real Fed Funds rate turned sharply positive in the early 1980s, dramatically above levels seen in the mid-1970s (see Figure 3). To this day, US inflation has yet to rise above 7% again.

Comparing the 1970s and the 2020s: can we expect a repeat?

Having discussed the 1970s, Deutsche notes that one of the biggest questions on investors’ minds is whether we’re in for a repeat. Some factors like demographics or globalization indicate that there are much greater inflationary pressures today. But others like declining union power and lower energy intensity are pointing in the other direction. We now look at a number of these in turn.

1. Monetary Policy

Like the 1970s, monetary policy is very loose today. In fact, the real federal funds rate (simply found by subtracting 12-month CPI inflation as per Figure 3) is actually lower today than it was then, while the increase in the money stock (Figure 1) has also seen a much bigger single year expansion than ever took place in the 1970s. Financial conditions today remain accommodative as well, thus providing a lot of support for the economy.

2. Debt

Recent decades have seen an extraordinary increase in global debt levels. In particular, government debt levels today are well in excess of the low levels reached in the 1970s. As a consequence, higher rates will have a much bigger impact on government and non-government balance sheets, and risk being much tougher to stomach today than they were then. This could mean policy makers are forced to remain behind the curve in a similar way to the 1970s, albeit for different reasons.

3. Demographics

The consensus assumes that demographics will be disinflationary as societies age. However, one similarity between the 1970s and now could be a worker shortage, albeit from different sides of the baby boomer demographic miracle. In the 1970s, the boomers had yet to hit the workforce and labor was relatively scarce. But from the 1980s onwards, the global labor force exploded in size as the boomers came of age. Simultaneously, China began to integrate itself into the global economy for the first time in several generations, thus unleashing a big positive labor supply shock onto the global economy. This combination has been disinflationary for wages for the past four decades. However, the major economies are now set to see their labor forces decline or at best level off as the baby boomers retire. So will we get similar labor market pressures as seen in the 1970s? Covid has shown what can happen to wages when there is a shortage of labor. The huge number of vacancies in low-paid jobs today due to a shortage of workers due to covid related issues are pushing wages up. And although the covid bottleneck will clear, the declining working-age population in many places over the decade ahead could see labor gain back some power that it lost from the end of the 1970s.

4. Globalization

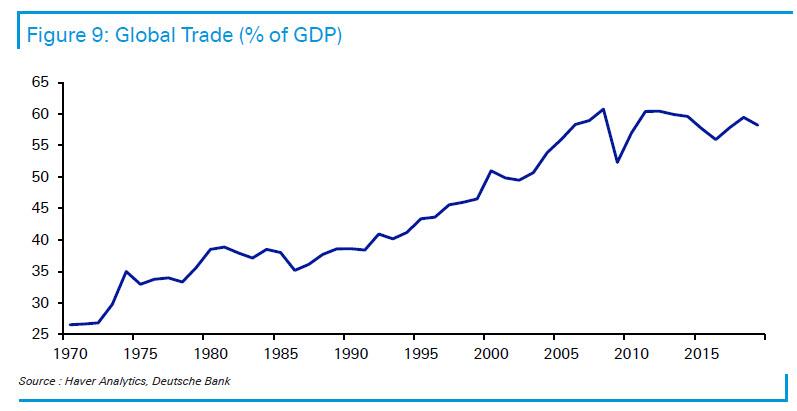

The late-20th century was an era of rising globalization, with the 1970s alone seeing the share of global trade in GDP rise from 27% in 1970 to 39% by 1980. But since 2008, that progressive advance has stalled, and there are many signs that the post-pandemic will see a return to less globalization, as both countries and corporates look to localize their supply chains in order to make them more resilient. In turn, a retreat from globalization and firms facing less competition implies higher prices than would otherwise be the case. So as with demographics, the potential retreat of globalization would remove another of the big forces that’s helped to suppress inflation over recent decades.

All the factors mentioned above point towards inflation being more difficult to combat today. But there are others that point in the opposite direction.

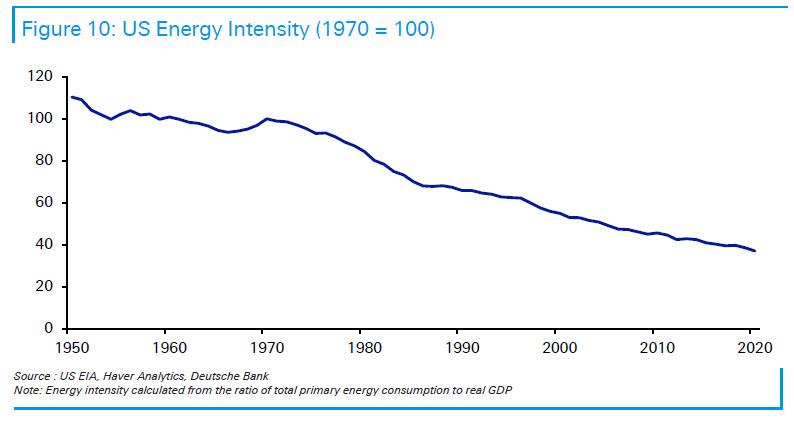

5. Energy Reliance

Since the 1970s, the US economy has become progressively less energy intensive. By 2020, the amount of energy required for each unit of GDP was just 37% of where it had been back in 1970, and the US Energy Information Agency are forecasting that will continue to fall over the coming decades. So with less energy required to support output, the impact of a price shock will be commensurately less than it was back in the Great Inflation of the 1970s.

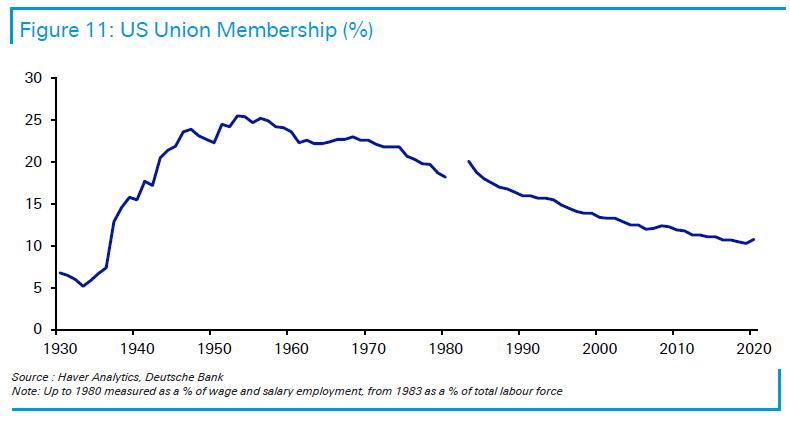

6. Union Power

Another force acting against inflation is the decline in union membership over recent decades. Unions themselves do not cause inflation, which is a monetary phenomenon, but they can contribute to wage-price spirals. This is because higher inflation leads to higher wage demands from trade unions to ensure their members’ wages keep up with the rising cost of living. But firms then anticipate this by bidding up their own prices further, which can create a circular feedback loop as the unions in turn demand higher wages still. So the fact that unions are weaker is likely to put downward pressure on inflation, all other things equal. Having said this, there is some evidence that unionization is on an increasing trend, albeit from a low base. The mention of unions in official company documents was the fastest growing of our ESG buzz words in September 2021 relative to a year earlier.

7.War, Geopolitics and Climate Change

Many of the biggest inflations in history have been associated with wars, and the inflation of the 1960s and 1970s got going around the time of the Vietnam War, when there was upward pressure on spending. Today, the economic response to Covid has been almost comparable, with fiscal deficits on a scale not seen since WWII for many countries. In addition, the geopolitics of Russia being such an important supplier of gas to Europe has parallels with the West’s reliance on Middle Eastern oil supplies in the 1970s at a time of a divisive Arab/Israeli conflict.

Going forward, the US/China relationship could be a key driver of inflation later in the current decade, particularly if an escalating cold war leads to a more bipolar world and a retreat from globalization, as discussed earlier. And that’s before we get onto the threat of climate change, where we’re already seeing the consequence of trying to move away from coal, in that we’ve become more dependent on other fuel sources such as natural gas. As the globe tries to further wean itself off fossil fuels, we could have more energy shocks over the course of this decade.

8. The lessons of history

Finally, history itself plays an important role in policymaking. For example, part of the reason that the economic response to the pandemic was so large and swift was in order to avoid repeating the mistakes of the global financial crisis, where delays undermined the recovery.

When it comes to inflation in 2021, plenty have raised concerns that today’s policymakers have little to no experience of dealing with a significant inflation problem. Indeed, for the decade after 2008, the main focus was on how to tackle chronically deficient demand as central bankers struggled to hit their inflation targets on a sustained basis in many countries. So the fear is that policymakers might have a dovish bias given these experiences, and risk being slow to recognize if inflation has become a more permanent feature of the landscape. This is particularly so when if anything, the perception is that they were too hawkish in the period following the financial crisis.

On the other hand, today’s central bankers and other policymakers are aware of the lessons of the 1970s and will not want their legacies to involve a repeat. They recognize that inflation and unemployment can’t be traded off against each other over the longer term, and have much better data than their predecessors. Furthermore, there is still strong political pressure to avoid higher inflation… even as there is even greater political pressure to avoid taking the much needed if very painful steps to contain the coming inflation.

What can we learn from this?

Looking at the 1970s, the most important lesson is that even if inflation is down to transitory factors, the arrival of yet more “transitory” shocks can accumulate to keep inflation at high levels, with expectations becoming unanchored. That was what occurred with the oil shocks: although inflation was sent sharply higher, the truth is that inflation was pretty high already, as a legacy from the late 1960s, and the shocks turbocharged it yet further.

But we can view the events of the 1970s with the benefit of hindsight. For policymakers at the time, it was less obvious that these shocks would not prove transitory, and today they face a similar dilemma. If policy reacts too forcefully to something central banks can’t control (like inflation thanks to supply-chain disruptions), then that risks undermining the recovery and actually pushing inflation below target, since the shock will eventually pass and monetary policy operates with a lag. On the other hand, doing nothing risks inflation expectations becoming unanchored, particularly if another shock then arrives to push inflation higher still. One can also argue that with money supply growth so strong over the past 18 months, there has been a strong monetary angle to inflation and therefore some tightening of monetary policy is sensible. Overall, it is an unenviable dilemma, and the debate in the economics profession right now speaks to the unknowns.

So we approach this question with some humility. But we do think it worth noting that many factors like debt, demographics and globalisation all indicate that we could be facing an even more difficult situation than we saw back then. And the monetary aggregates have also seen a much more rapid increase as well. So policymakers will need to be vigilant for a potential repeat, particularly given that the institutional memories of high inflation have faded over time.

Source: https://www.zerohedge.com/markets/stagflation-here-comparing-2020s-1970s

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The current tools available to central banks and policy makers fall a long way short of what is needed. We plan to make changes to the lending and savings industries that will start a process towards creating the macro-economic tools that are needed.

Here is a flier we are testing. It will go by email with a link to the discussion website.

The idea is to update a wages index-linked lending model that has been in use in high inflation countries for a couple of decades and introduce it to the rest of the world. Initially funded by pension funds this will dramatically cut arrears risk as borrowers will increase their cost of repayments at a rate that lags behind the wages index, possibly by 4% p.a. or almost 12% after three years.

When adopted by all lenders and when regulatory restrictions have been lifted, people will be able to get a wages index linked annuity at a predefined cost: X annual wages saved will provide a pension for life of Y% of that annual wage, rising with the wages index. The appropriate new regulations will ensure that the property market will no longer inflate and then bust and central banks will have better control over monetary policy.

But that is not good enough. Central banks need full control over the stock of money, MO / MA in active circulation so that it remains scarce but available at a price.

This creates another tool that is needed to manage a fiscal stimulus in a way that does not add a rising sovereign debt or even the need to borrow money in order to deliver it. The money needed by the National Treasury will be created by the central bank and a similar amount of money repaid to lenders will be destroyed.

HOW IT ALL WORKS

When all of the reforms have been done, the reserve ratio for lenders will be 1. All new money will be created as deposits earning interest by the central banks, which rate of interest will be determined by market forces at auctions of deposits and any excess money that is created to deliver a fiscal stimulus will be instantly removed by the central banks as borrowers repay their debts to lenders and lenders are forced to place those repaid deposits with their central banks. As many economists have noted, creating and destroying sovereign (government) money is a cost free process of altering the total amount of money held by lending institutions at the central bank. It is like altering the number in a cell on a spreadsheet.

From here-on in money will facilitate economic activity, and not get in the way of it. The market rate of interest will vary freely without causing inflation problems in the property or equity sectors, and everyone will have a better chance of planning their financial lives. The removal of risk saves money for everyone and the simplification of everything will enable businesses and governments to plan further ahead.

In a complex system if any one thing is improperly done the knock on effects spread throughout the system. So when we replace our linear loan repayment system with an exponential system that gets paid from exponentially growing incomes we take a huge first step in the right direction. As Professor Leon Brummer, professor of stock broking at the University of Pretoria, remarked to Edward C D Ingram, “This simplifies everything.”

TESTIMONIALS – Three of many more

“These reforms are critically important.” Andrew Pampallis, retired Head of Banking at the University of Johannesburg, referring to the lending and savings reforms.

“These ideas will become prescribed reading at universities.” Professor Evelyn Chiloane-Tsoka from the University of South Africa.

“This book will inspire rethinking on the perimeters of economic thought and theory, and their practical use in policy making. A ‘should-read’ for budding researchers in Financial Economics to expand its horizon.” Dr Rabi N. Mishra, Economist, and a Chief General Manager, Reserve Bank of India.

Very pertinent at the moment. It will eliminate the cycle of bailouts and bailinns.