Saturn Devours His Children

A recent Wall St Journal article gave vent to a scare-story full of Underconsumptionist claptrap, carried under the catchy headline: “The Coronavirus Savings Glut”….

For honest money and social progress

For honest money and social progress

A recent Wall St Journal article gave vent to a scare-story full of Underconsumptionist claptrap, carried under the catchy headline: “The Coronavirus Savings Glut”….

For many an age, a principal element of Britain’s strategy in its frequent wars with its Continental rivals was that of the naval blockade….

complete show notes & links: PODCAST LINKS: https://soundcloud.com/paul-60-1 player.fm/series/1877735 itcher.com/podcast/thinktradingcom/the-state-of-the-markets unes.apple.com/us/podcast/state-of-the-markets/id1301360737?mt=2 SHOW NOTES: __________________________________________________ Tim F Price @timfprice of www.pricevaluepartners.com & Paul Rodriguez…

In his recent posting on Linked In, entitled, ‘The death of macro-prudential’, Stuart Trow of the EBRD delivered a well-aimed broadside at the pitiable…

A theme which frequently pops up in current financial and economic commentary is that of the burgeoning levels of outstanding debt under which all…

As world stock markets continued to climb to cyclical – if not all – time highs, it became almost the norm for industry talking…

Demographics, productivity & the great central bank fallacy of interest rate determination Summary As we go to press, the Mighty Oz’s and Grand Panjandrums…

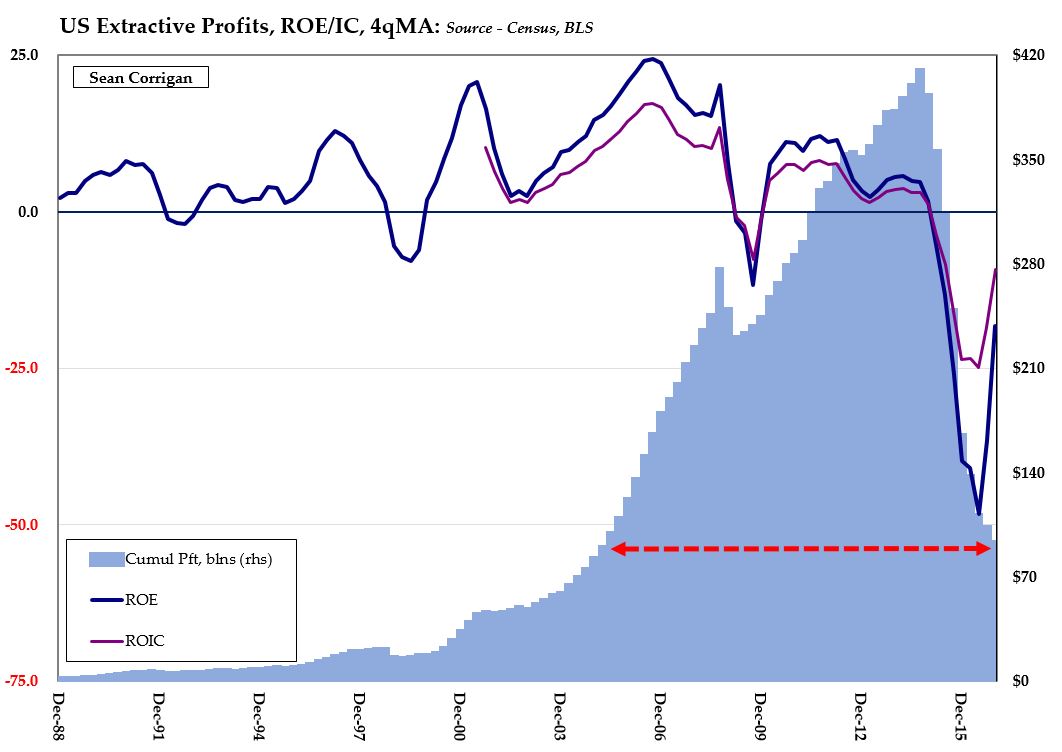

Dear Lord, Y’all give us another oil boom… If there is one sector of the US economy where an Austrian-style Boom-and-Bust bust has taken…