Previously published at GoldMoney.com …

What would you like to see as a solution – albeit perhaps imperfect – to the Greek debt situation?

Sean Corrigan: What I advocated as soon as the last credit bubble burst was exactly what is now being slowly accepted as a sine qua non – that debtors who over-extended themselves in the Boom must renegotiate with creditors – who were, conversely, too glib about the risks they were taking on – now that the Bust has arrived.

This would have been much better undertaken at the first signs of trouble, over four years ago, than now and – given the difficulties of achieving a fair, judicial burden sharing when PUBLIC sector borrowers become involved – it would have been much better without the intervening folly of crude Keynesian stimulus, pace Soros, Krugman, Wolf, et al.

Greece should cut its debt to the maximum level consistent with its long-term sustainability under the constraints imposed by its currently poor growth prospects and it should be made to run a balanced budget henceforth – perhaps through denying it any new credit on terms which are too soft. If that means the state must shrink and people can only receive what they themselves can earn and pay for, so be it. I am confident that this would open up untold avenues for private wealth generation. After all, the Greeks have been noted traders and entrepreneurs since history began – while their current societal degeneracy has been an artefact of state intervention – whether their own or the preceding Ottomans’ – and it is high time their natural talents were given free reign, rather than their natural human proclivity to do as little as possible when someone else seems to be paying for whatever it is that they most require.

That this transition is unlikely to be a pleasant experience is not to be denied, but neither is the present prospect of hopeless, semi-permanent “austerity” – besides which, their great-grandfathers went through much the same experience in the late 19th century and came out much the better for it!

As for Western banks and insurers – well-tough! Caveat commodator – let the lender beware! Their own creditors and shareholders should be the first to take losses for their voluntary participation in such bad executive decision making, as they would in any other business. If that takes them to the brink of failure, again, so be it: let the strong buy out the weak and let’s reduce the count of those making a living by leveraging off both explicit and implicit taxpayer support in a ludicrously overbanked world.

Any role for government should be limited to expediting the transfer of titles from debtor to creditor, as well as the transformation of title from debt to equity with a final, backstop role in guaranteeing a minimum level of narrow money circulation so as to avoid a self-fuelling secondary depression.

What kind of a solution do you think that the EU/IMF will arrive at for Europe’s debt crisis?

Sean: I doubt it will be anything as comprehensive as the above, though, given recent developments, if the Northern members stand firm and we listen to those Bundesbankers who are trying to insist upon individual fiscal responsibility – as well as to restore a renewed, future separation of fiscal from monetary policy – rather than to the cabal at the ECB which seems to think its job is to protect bankers, not the value of the Union’s money, then we might be a lot closer to this than was conceivable even six months ago.

Do you think that the ECB will resort to large doses of QE in order to ease the pressure on the eurozone?

Sean: At the moment, I would only see this happening by default. That is, if they have to offer so much support to shore up the existing debt structure that it becomes operationally difficult to sterilise.

There is a touch of the Oscar Wildes about the fact that they have already lost two Bundesbankers in swift succession. I’m not sure they would risk the implicit rejection of their policy entrained in the resignation of a third.

Do you expect to see countries leaving the eurozone?

Sean: Strictly speaking it is unnecessary if the undoubtedly steep adjustments needed are taken by reducing prices, removing costs, and eradicating impediments and inefficiencies. Our Keynesian friends, with their unshakable thirst for monetary chicanery, sneer that such an “internal” devaluation; is impossible, but it is more honest, more equitable, and more salutary than the alternative of a mass resort to the money illusion of a currency devaluation.

Anyone who doubts this should look at the fact that, though not entirely without blemishes and short-cuts, one or two eastern European nations – as well as the Irish –have already gone a very long way down this road.

That the positive results for the first have not yet made themselves so clearly felt in the Emerald Isle is almost entirely due to the fact that Ireland was shamefully bullied by both the ECB and the US Treasury into the untenable co-option of the privately-contracted debts of its banking sector at the height of the crisis. Ireland should also put these straight back where they belong – with those banks shareholders and creditors – and should instead concentrate on making sure that all their hard-work in rebalancing the economy redounds to the well-being of the ordinary Irishman and woman.

So, to come back to the question, to see a secession, much less an expulsion, we have to assume that the distaste for the Greek’s –and others’ – persistent free riding (as expressed recently by the likes of Otmar Issing) overcomes fears that this will weaken, not strengthen, the remaining union by setting a dramatic precedent and so focusing market scrutiny even more closely on the finances and political temperament of those left in the club. We also have to assume that the leaver’s elites see the subsequent trauma as either lesser in nature or easier to blame on others.

Until those two conditions are filled, I would expect the Nomenklatura to continue to inch painfully towards a solution which entails no shrinkage of the Union, entailing, as this would, the relinquishing of 80-odd years of political wishfulness.

What sort of things are you looking at to discern whether or not gold is overvalued or undervalued?

Sean: What is “value” in a world where the single goal of the powers-that-be is to deny the market the ability to have its constituents’ underlying ordering of wants accurately reflected in the price structure?

We have no proper market in capital; severely impaired markets in any number of basic goods; false markets in real estate; distorted markets in labour (hence why so many poor souls are still without jobs) and no certainty about anything except the awful certainty that nothing is off limits to those who are desperately trying to put Humpty Dumpty together again in time for the next turn of the electoral cycle rather than accepting the fact that he’s shuffled off this mortal coil and that it would be better now to see whether at least we can salvage a half-decent omelette out of the remains?

Gold is moving up as central bank balance sheets expand at an inordinate pace and as trust in fiat currencies erodes accordingly. Gold is working also as a diversifier – even an insurance policy – in a portfolio of real assets: outperforming other commodities and equities when we are in one of the recurring “Risk Off” phases which are so stultifying recovery.

Occasionally – as, for example, in late summer – it gets palpably overbought by those who are attempting to use zero-cost finance to game all this confusion and, as a result, it often suffers violent corrections.

However, while the perception persists that inflationism is the first line of defence, and while no one can be sure that – thanks to the stupidity of the Fed and its peers in trying to deny the reality of the losses we suffered under their previous regime of over-easy money – further financial disasters do not lie just around the next bend, it is hard to say that gold will not continue to do what it has for much of the past 5-6 years and grind ever higher, especially in USD trade-weighted terms.

Do you expect to see Britain facing the kinds of problems that are currently affecting the PIIGS?

Sean: Well, when the Crisis first broke, I used to joke that we Brits should not be too supercilious about the PIIGS since we had Scotland, Wales, Ireland (North), and England – aka, the SWINE!

The UK’s “austerity” package is so far somewhat elusive to locate since spending is still creeping up. The country still runs a near record trade deficit in the middle of a slump, despite having a currency whose decline in the Crash was only beaten by that of the Icelandic Krona.

Since 1998, Britain has lost 40% of its manufacturing jobs and added 35% to its roster of public sector workers, increasing the ratio between these two classes of tax-payers and tax-eaters from 60 drones per 100 bees to 160! And now, despite the highest level of joblessness since 1994, we have the highest gain in the Retail Price Index in 20 years, with the Bank of England actually easing as it rises!

Given the fragile coalition which is in office and the size of the lobby for maintaining public spending – as well as the almost insurmountable, pro-Labour electoral calculus built into the geography of the constituency boundaries – it is hard to see how the deficit, much less the debt will be meaningfully reduced without an eventual recourse to the tried and trusted old methods of inflation.

What’s your opinion of ‘Europe v. America’ in terms of economic health?

Sean: Well, for now, Europe seems to be reluctantly facing up to the reality that the state treasury is not a bottomless barrel and that public sector cannot live up to its casting as the Keynesian Tooth Fairy. This may not stand the test of time, but, for now, there is something of a push to reining in budgets, not expanding them endlessly.

We can hardly say that about the US where almost 40% of the enormous $1.3 trillion deficit is unmatched by revenues of any kind – something that Professor Bernholz at Basle University has identified as a threshold beyond which the threat of accelerating inflation becomes very real.

On the one hand, the Democrats seem to think that taxing the odd millionaire a few extra dollars will solve all the nation’s problems, and, on the other, the mainstream media won’t even accord any airtime to the one man to have foreseen the difficulty, to have consistently analysed the cause, and to have put forward radical, but logical proposals for dealing with the issue – namely, Ron Paul. In each case we are hollowing out the middle classes and reinforcing the divide between the plutocracy and the pauperised. In each case enterprise is being stifled and the flames of a paralysing uncertainty are being stoked ever higher.

America is traditionally seen as a more “flexible” society where the barriers to entrepreneurship are fewer and hence where recovery is both swifter and more assured, but, the laziness of relying on the ever-open chequebook of a woefully compliant central bank could do an awful lot to undermine whatever marginal advantage the nation still possesses over Welfare State Europe.

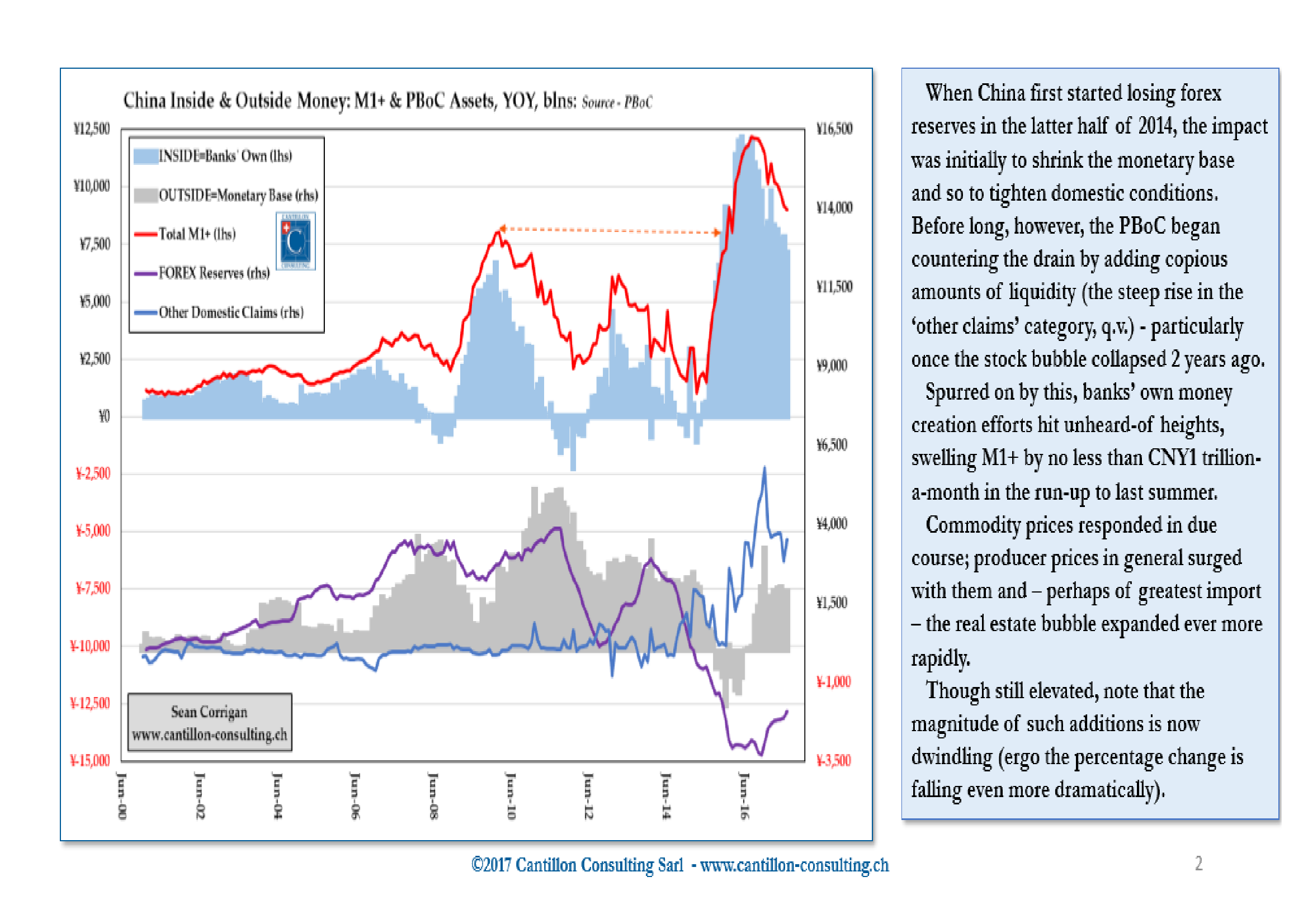

How dependent on western demand is the Chinese economy? Is “decoupling” a flawed concept?

Sean Corrigan: This is harder to say in absolute terms than many will admit, but, undoubtedly, the economy stands on two main pillars, neither of which is as steady as it might be.

Externally, the West still supplies much of its market and, in terms of its overall trade surplus, the US alone has accounted for more than 100% of the past two years’ total, and for 75% of the past five years’.

Even if we can argue forever about what the ultimate value added component of all this is, China’s exports amount to around a quarter of its published (if highly dubious) reckoning of GDP, so, clearly, a significant numberof livelihoods are dependent both on this and on the import and shipping of those goods that give rise to such exports.

However, such is China’s wayward economic structure that it has distorted all manner of pricing signals internally, too – the cost of capital, of land, of energy and other inputs – so that the second, shaky pillar on which it relies takes the form of ever more, credit-fuelled, higher-order malinvestment to generate its famous 9%+ national income scores.

It is only a little tongue in cheek to say that when we consider that the nation has yielded up a good deal of its comparative advantage (however illusory some of this was) and unleashed a nasty inflation – complete with a boom in what will prove to be either marginally productive, or completely unproductive, property and infrastructure – that it has sucked up into underremunerative ends its people’s savings, even as it purports to offer them a job not otherwise to be had in building more of the same, there are parallels with the mid-90s Asian Tigers.

Back then, their increasing uncompetitiveness and their growing misuse of resources on turning cheap money into expensive real estate was a key signal of the bust to come. The main difference with today’s China is that far less of this present excess is being financed with hot foreign money, given the difficulties in – though not the impossibility of – transferring funds across the current account barrier.

China is indisputably an enormous accident waiting to happen, but the only thing which may prove uncomfortable for the China bears among us is the nation’s unquantifiable, but redoubtable ability to hide the true cost of all this and to shuffle money endlessly from one balance sheet to another – to hide subsidies and support payments in a welter of accounting confusion and soft loan extension. Even the Soviets had their moment in the sun, remember, when Khrushchev’s tentative economic reforms in the 1950s seemed to offer a better way of doing things than either his predecessor or his contemporaneous Western competitors could manage.

When Adam Smith remarked, two centuries before that, that there was “a lot of ruin in a nation”, he was giving cold comfort to those long CDS protection or short Ozzie banks!

American financial analyst Jim Rickards has cited four potential outcomes to the world’s current monetary problems: multiple reserve currencies; SDRs; gold; or chaos. Which of these do you see as the most likely outcome – or is there another possibility?

Sean: Barely-managed chaos is what we have endured for the past 40 years – and arguably for much of the 60 years before that. I’m not sure that does not remain the smart way to bet, whatever the ambitions of the One World Platonic elite for a global Federalist construct to be forged in the funeral pyre of finance corporatism!

What things can ordinary people do to protect themselves from the economic fallout that may result from all these events?

Sean: The goal of the authorities is to make every man a gambler or a wastrel, for that way, it is assumed, the stock markets will rise again and cash registers across the land will ring out a merry peal of renewed Keynesian prosperity.

The sad truth, of course, is that this is a road to ruin along which we are all being force marched by the inflationist intellectuals and the other indefatigable defenders of the Provider State which their policies underwrite.

Hence, we can only offer generalities. Work hard; work longer; pay down all unproductive debt – at least until such time as you are sure that the interest burden and redemption schedule you face will be washed away by the loss of value of the money in which the loan is denominated. Try to acquire as much flexibility as possible in your finances for everything is – and is likely to remain – in a state of flux for a long while to come, with few certainties attached to the path by which we will eventually be forced to recognise the degree of our self-impoverishment. Try to find honest and competent entrepreneurs in whom to invest as these provide the best ‘active management’ of your money of anyone, especially when times are hard. Try to turn soft money into hard value wherever you can identify it.

This is all every well to say, of course, but much, much harder to achieve and meanwhile, there is the awful truth that there is no reward for thrift, no safe haven for one’s savings, and that the greater one’s success in managing one’s affairs and the greater one’s moderation in spending the rewards of that success, the larger and juicier the temptation one offers for an increasingly rapacious tax man to siphon off one’s reserve into the echoing depths of the state’s empty coffers.

Sadly, there can be few guaranteed winners in such a world.

Terrific interview, Sean.

One error (quite possibly a typo) seems to have crept in.

“We can hardly say that about the US where almost 40% of the enormous $1.3 trillion deficit is unmatched by revenues of any kind – something that Professor Bernholz at Basle University has identified as a threshold beyond which the threat of accelerating inflation becomes very real.”

What you meant, presumably, is that this threshold occurs when deficits exceed 40% of government expenditure.

yes, that para WAS rather garbled… what it should have said was that circa 40% of expenditure is unmatched by revenues – that gap amounting to no less than $1.3 trillion -itself now more than 10% of non-Govt GDP.

Sean Corrigan advocates a sound, non-inflatable supply of market-given money; free banks, shorn of all state support and legal privilege and hence the abolition of the central bank.

I think I understand and can empathise with Corrigan’s point of view, yet still I remain somewhat perplexed, wondering whether or not his wish is a priori self-contradictory.

As a neophyte and less than dilettant in the dismal science, I understand a Central Bank’s role to impose reserve requirements on fractional-reserve banking thereby putting limits on the amount of money banks are permitted to lend thereby limiting money creation – leaving central bankers in theoretical control of how much money is being created in the economy.

PhDed Quants and modern computer technology allowed banks to indulge in financial necromancy which Charles Morris credits David Roche as coining the “new monetarism”. Swaps and securitization increase the money supply by converting more and more real assets into tradable instruments. (A new species of paper currency as it were.) Meanwhile – not only are banks able to move liabilities off their balance sheets thereby permitting them to recycle these illegitimate windfalls into even more shakier and shakier loans… banks are even able to transmogrify “liabilities” into “assets” thereby magnifying the problem and distorting balance sheets into fantastic perversions of accountability.

We are in fact confronting an ongoing “reverse-liquidity” problem. Private Banks (Not Central Banks) are perversely and without control creating liquidity ex nihilo. Unfortunately, the resulting debt results in today’s taxpayer “solvency” problem.

An obtuse gainsayer could attempt to contradict Sean Corrigan by claiming today’s monetary catastrophe was not due to Central Bank interference; but rather Central Bank impotence given novel and unanticipated modern fiscal methods of mass destruction (to paraphrase Warren Buffet).

I view today’s economic cataclysm as the “Tragedy of the Commons” writ large and squared and expanded yet again. Try as I may, the Libertarian solution to the “Tragedy of the Commons” offers little comfort. Their solution of privatization in excelcis to my unjaundiced eye is precisely what got us into this unholy mess. I cannot but recall some of Sean Corrigan’s earlier essays describing the fiasco of unregulated Italian Renaissance banks and their invention of the term “bankrupt” as a corruption from banca rotta.

I cite by way of continuing contradiction my favourite chapter in George Cooper’s seminal book “Minsky meets Mandelbrot”. I would be most curious how Sean Corrigan would respond to Cooper’s thesis.

http://www.amazon.com/Origin-Financial-Crises-Central-Efficient/dp/0307473457#_

ITMT – forgive my palaverous prose… I am truely perplexed and await elucidation with bated breath.

BTW – I agree… GREAT INTERVIEW!!!