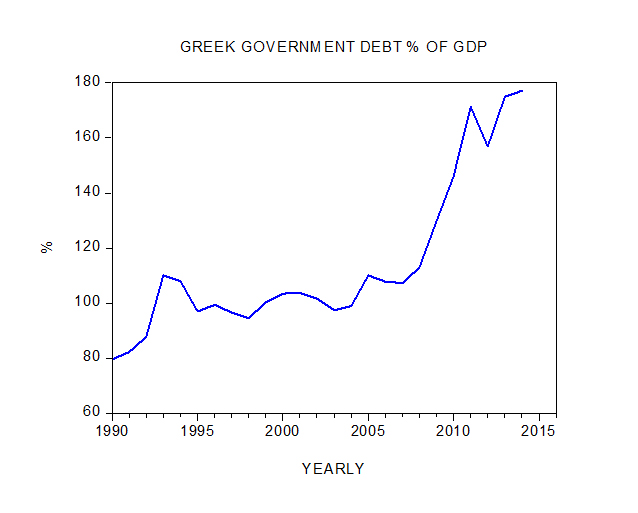

Greece crisis proves the need for a currency Plan B

byThe recent Greek capitulation under pressure from other euro member countries, led by Germany, demonstrates that euro members have de factoceded sovereignty over fiscal policy to…

For honest money and social progress

For honest money and social progress

The recent Greek capitulation under pressure from other euro member countries, led by Germany, demonstrates that euro members have de factoceded sovereignty over fiscal policy to…

Dear Prime Minister Tsipras, First, congratulations for mustering the popular support to say “no” to the troika. The euro has long offered Greece a…

For months, now, the mass media and the financial markets have anxiously watched and waited to see the outcome of a war of words,…

It goes without saying that you pick up any newspaper or journal of late and one is bombarded with how Grexit and contagion risk…

The International Monetary Fund (IMF) confirmed that Greece had not made its scheduled 1.6 billion euro loan repayment to the fund. As a result…

This coming Sunday Greece will hold its referendum. The question to be asked is not, as the foreign press initially reported it, about leaving…

Greece needs to reschedule its debt or default Capital Controls maybe inevitable A piecemeal solution is not the answer, yet it’s more likely than…

In his magisterial 1936 work, ‘A World in Debt‘, Freeman Tilden treated the business of contracting a loan with a heavy serving of well-deserved…

“Central bankers control the price of money and therefore indirectly influence every market in the world. Given this immense power, the ideal central banker…

Every Monday morning the readers of the UK’s Daily Telegraph are treated to a sermon on the benefits of Keynesian stimulus economics, the dangers of belt-tightening…