The recent Greek capitulation under pressure from other euro member countries, led by Germany, demonstrates that euro members have de factoceded sovereignty over fiscal policy to the EU. While this arrangement may be acceptable to some countries, perhaps even Greece, it will be resisted by others.

However, as the Greek failure also demonstrates, any eurozone country wishing to restore fiscal sovereignty, or restructure some of their debt, or implement any policy or set of policies that runs afoul of the preferences of certain Eurogroup finance ministers will have near-zero negotiating leverage if they fail to plan, credibly and in advance, for the introduction of a viable alternative currency.

Without this critical card to play, the country in question will be held hostage by the now politicised ECB. Its domestic banking system and financial markets will be shut down, the economy will grind to a halt and the government will face either a humiliating retreat or full capitulation.

Former Greek finance minister Yanis Varoufakis has now revealed much of the detail of the recent negotiations, capitulation and attempts to vilify him personally for acting insubordinately or even in a treasonous manner at the 11th hour. However, it is entirely understandable that, once Varoufakis became aware of the degree to which his country’s banks and national finances had been taken hostage by the ECB and EU institutions, he sought some flexibility in order to strengthen Greece’s negotiating position. Alas, this was much too little, and way too late.

In retrospect, it is now obvious that Varoufakis and his colleagues should have set about developing a credible alternative currency plan prior to entering into any negotiations around either debt reduction or fiscal reforms. Had they done so, when the ECB suspended further increases in the ELA, forcing the banks and financial markets to close, Greece would have been able to roll out a temporary plan which, in the event that subsequent negotiations were indeed to fail, could easily have become permanent. Moreover, the very existence of such a plan would have greatly strengthened Greece’s hand to the point where negotiations may well have succeeded.

Although it might sound a daunting prospect, introducing an alternative currency is not particularly difficult as long as the fundamentals of currency design are understood by its architects, and it is professionally planned in advance. The problem for Greece and other countries is that currency design is a skill which the troika are actively seeking to have every nation “unlearn”, in Orwellian speak. The personal careers of too many senior officials depend upon no one of the 19 nations breaking away and thriving, rather than collapsing.

Having spent four years pitching currency design alternatives to an array of governments, central banks, and leading opposition parties we are happy to set out the basic steps. The domestic banking and payments systems must be made sufficiently flexible to switch from one unit of account to another. Either physical cash, or some form of electronic cash, such as debit or credit cards, must be printed or produced in advance, with a robust distribution plan. These logistical considerations are no different in principle than a new product rollout for a major corporation in a major industry.

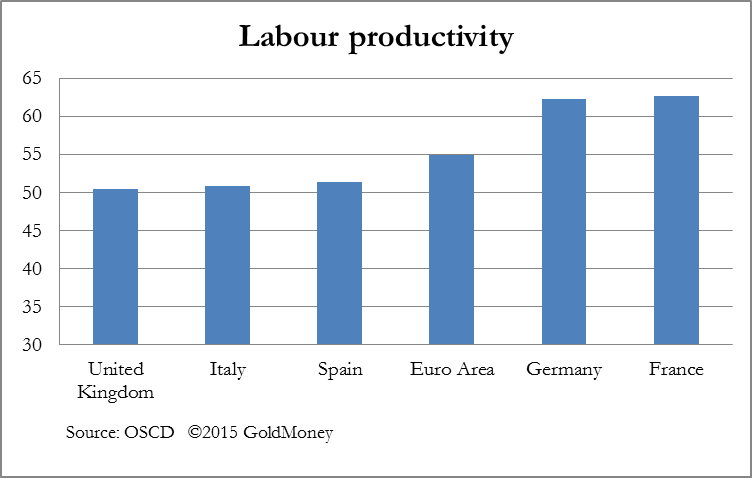

What is different, and requires due consideration, is how a new national currency will be credible in the eyes of the public expected to use it. Any currency thought to be at risk of a major devaluation will struggle to gain sufficient credibility. However, if the currency is introduced at an already credibly devalued rate – one which would reset Greek unit labour costs to a level competitive with the euro area average for example – and the national debt burden is also redenominated in a fait accompli visa-vis creditors, greatly reducing its value in real if not nominal terms, then the new currency’s value will indeed be credible and will be able to support commerce and business as usual. Additional credibility-boosting actions could include the build-up of foreign reserves, say by selling off specified state assets.

The lesson for a future Greek government, or any present or future euro area government is clear: if you want to restructure your sovereign debt or restore sovereignty over fiscal policy, you simply cannot negotiate without a credible plan to reintroduce a national currency. Recent statements by the governments of Poland, Bulgaria and the Czech Republic that they are in no hurry to join the euro, if ever, indicate that this message is not lost on these increasingly successful, competitive economies.

Present euro area members take note: failing to prepare an alternative currency Plan B is preparing to fail in future negotiations. The time to plan is now, before the probably inevitable arrival of the next euro sovereign debt crisis.

- John Butler is a contributor to Cobden Partners, a bank and currency reform consultancy, and the author of The Golden Revolution (Wiley and Sons, 2012)

Source: http://www.theguardian.com/business/economics-blog/2015/aug/13/greece-crisis-proves-the-need-for-a-currency-plan-b