Introduction: Bank-Money

by‘BANK ROBBERY’ is not a book about how to rob a bank: it’s about how banks rob us. The title sounds a bit sensationalist:…

For honest money and social progress

For honest money and social progress

‘BANK ROBBERY’ is not a book about how to rob a bank: it’s about how banks rob us. The title sounds a bit sensationalist:…

INTRODUCTION Philip Mirowski, known for his book More heat than light – economics as social physics, physics as nature’s economics in which…

(This Report is an adaptation of my keynote address to the 2015 Sydney Precious Metals Symposium, held this month.) “Power tends to corrupt. Absolute…

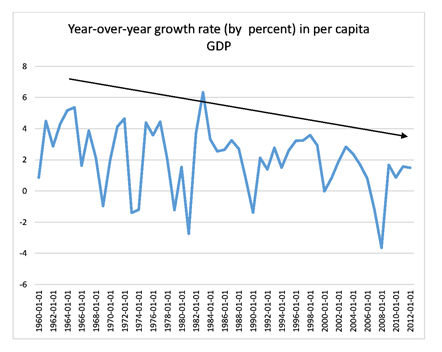

Since the economic downturn of 2008, the critics of capitalism have redoubled their efforts to persuade the American people and many others around the…

The following was written for The Cobden Centre by Vishal Wilde. The Eurozone is in dire need of monetary reform in order to…

[This article, from Peter St. Onge at Mises.org was first published here https://mises.org/library/government-regulation-and-economic-stagnation] One of the more interesting economic debates in the past couple…

[This piece first appeared here http://www.epictimes.com/richardebeling/2015/05/free-trade-benefits-vs-fears-of-foreign-goods/] Japanese Prime Minister Shinzo Abe spoke before a joint session of the U.S. Congress on April 29, 2015 and…

The dollar is always losing value. To measure the decline, people turn to the Consumer Price Index (CPI), or various alternative measures such as…

At CPAC, recently, an estimated 10,000 conservatives and libertarians, together with many presidential aspirants, gathered across the Potomac. They did so amidst massive hoopla…

As a new year begins, it is easy to consider that the prospects for freedom in America and in many other parts of the…