So, the European elite have temporarily managed to contain the submerging market contagion which was threatening to blow apart their beloved superstate and have even managed ‘not to waste a good crisis’ by moving closer to the theoretically illicit fiscal transfer union which many feel must be the inevitable next step if the empire of Charlemagne (or of one of his equally arbitrary later emulators) is to be re-established in all its dubious glory

Of course, many questions remain unanswered, despite the remarkably convoluted attempt to lower the interest bill and to back away from the redemption cliff faced by Greece and its fellow strugglers.

Not the least of these is the legal issue of whether the announced programme will satisfy the Solons of the German Constitutional Court and, even if so, whether it will then require a lengthy and possibly fractious ratification by each of the member state parliaments before it can come into force.

Just how widespread will the private sector’s ‘voluntary’ participation in the accord turn out to be? Certainly, we can not afford to be too sanguine about the 90% acceptance rate assumed in last week’s proclamation. If enthusiasm is lacking, does this imperil the CDS trigger? Will it lead to hold-outs seeking to frustrate the bond exchange, or suing for better terms? Can the EU’s insistence this is for Greece and Greece only—a condition already partially breached in the funding rate adjustments—really be made good if, say, the Irish decide they would like to loosen the nails attaching them to the self-imposed cross of Anglo-Irish, et al?

Next, we must wonder whether those nations granted what is no more than a breathing space by this grand financial prestidigitation will still manage to summon up the will to enact the requisite degree of fiscal consolidation—complete with its demanding schedule of supposed privatisations—or whether the removal of the guillotine from the public square will encourage yet more damaging opportunism among the ruling classes who are improbably meant to incur lasting public wrath by diminishing the public trough.

The fact that, a quarter of a century on, Margaret Thatcher is still instinctively reviled by large sections of both the British labour movement and its fellow travellers among the metropolitan chattering classes should give the lie to the idea that political courage can really be expected to be its own reward.

More fundamentally, can we really suppose that the PIGS can now find a way to re-orient their human and physical capital on a sufficiently broad scale to enjoy a modicum of genuine material progress in place of their disastrous Rake’s progress and easy credit over-indulgence of recent years?

Beyond this, we must also keep a careful eye on the new powers of intervention granted to the EFSF—even if their exercise is supposed to be subject to the approval of the austere priesthood of the ECB—lest this prove to be a Pandora’s Box of budgetary indiscipline, monetary mission creep, national champion corporate welfarism, and Asian-style ‘price keeping operations’.

Until such matters are resolved, all we can safely say is that a near-term financial dislocation may well have been averted, but that it is far, far too premature to pack away the sackcloth and ashes and break out the bubbly.

With the super-troupers being extinguished, the elephants and trick ponies being led off to the grooming pens, and the roustabouts taking down the gaudy poles supporting the billowing Big Top in Brussels, lovers of political circus have begun to switch their attention instead to the no less heated arguments raging over the US debt ceiling.

This, too, has taken place in an atmosphere of increasing acrimony and to the accompaniment of some ludicrously overblown rhetoric concerning the Armageddon about to be unleashed upon the world by what the ineffable Vince Cable—giving voice to a sentiment shared widely by the soggy social democratic centre of Europe—categorised over the weekend as a ’handful of right-wing nutters in Congress’.

Come on, people! This is NOT the fiat money equivalent of the Cuban Missile Crisis, for goodness’ sake! We are not going to reduce the world to cinders on the morning of August 2nd if the imperial presidency actually has to hew to the Constitution for a change!

While there would no doubt be occasion for some interim difficulty in speculative markets if the US did not get to borrow even more next week, the Federal government need not actually default on that fateful day: one should not overlook that it does still face the option of simply not writing as many uncovered cheques as has been its all-too profligate wont.

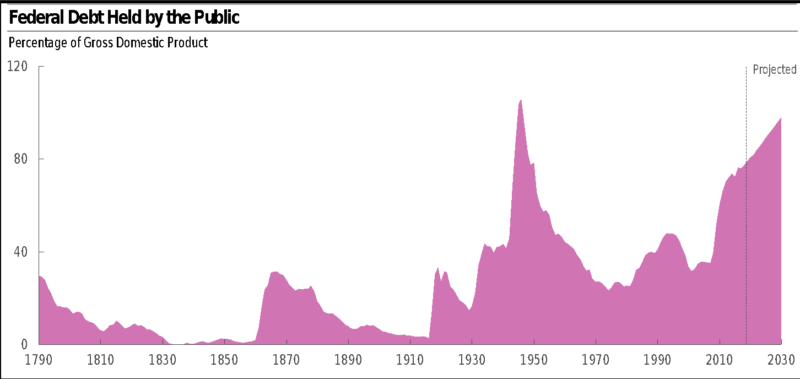

Be aware that the world’s largest economy still luxuriates in a soaring deficit of over 12% of private sector net domestic product (the wealth-creating rump out of which such debt must be serviced and redeemed) despite the ostensible recovery being enjoyed there. This gap comprises no less than forty, potentially inflationary percentage points of a vast, $3.6 trillion level of annual expenditure which is not only bigger than the output of the entire Geman economy, but which amounts to an initiative– and responsibility-crippling 30%+ of PNDP—a proportion heretofore unprecedented in peacetime.

Post-crisis, the Obama administration currently doles out three times as much as did the hardly-parsimonious first Bush one, as recently as 1990, burning through as much in a year as its predecessors in office managed cumulatively to consign to the flames in the entire first three decades of the post-WWII experience.

To imagine that one could not make a meaningful attempt at good housekeeping within such broad confines—without having to confiscate more private means or to penalise more individual endeavour along the way—is, frankly, risible: a fact of which the erudite, considered, and entirely sane Ron Paul (a man we would back over the likes of that elder statesman-manqué, Vince Cable, in almost any field of endeavour) is just as fully cognisant as he is aware that this game of brinkmanship is one of the few methods possessed by a no longer supine legislature to bring an arrogant executive to heel.

But what, we are constantly warned, if the US loses its AAA rating? Well, first of all, if this game of chicken ends up lowering the trajectory of future indebtedness, much less actually reducing it, this would presumably enhance, rather than impair the nation’s creditworthiness. If it does so by shrinking the deadening footprint of the state and so ‘crowding out’ less of the nimble, pitter-patter of the private sector, the effect would theoretically be redoubled as the prospects for growth glowed accordingly brighter.

Even if such a benign outcome were not to be achieved, would the possession or otherwise of this three-letter talisman do anything material to alter the dynamics of the country’s debt, or to raise the likelihood of its better management of its finances? Of course not!

For all the talk of eligibility triggers and violations of investment policy guidelines, it hardly seems conceivable that American buyers will decide en masse to eschew forever the obligations of their own sovereign in favour of Canadian paper, or Austrian, or that coming from Singapore, even if we might expect some interesting trading opportunities to arise—especially in smaller markets—from any marginal shift in attractiveness as the initial adjustments were being made.

Circumstances do differ between the two, but those tempted to take the government’s alarmism to heart might console themselves with the observation that Japan has sold 10-year debt at an average nominal 1.5% since it lost its first AAA rating in 1998, as compared to 4.5% in the prior period when it was thought to be on the verge of taking over the world (for real yields, we can compare 3.1% pre-98 to 1.6% after that watershed).

Absent the expectations of a renewed policy of monetization from the Fed, US Treasury rates are therefore likely to back up far more from the simple return of a modicum of free market pricing, regardless of their attached rating, than they are from a belated recognition by the zero-credibility agencies that no amount of politically-convenient pretence to the contrary can seem to put cloth on the back of a thoroughly naked emperor.

The fewer free rides the global hegemon enjoys—either in the debt or currency markets (and the two are, naturally interlinked) – the more responsible his behaviour might become toward both us and his own oft-afflicted citizenry. This battle could just conceivably bring about exactly such a curtailment of his ‘exorbitant privilege’.

Can this be entirely a bad thing of which to dream?

Whatever the upshot, market participants should not lose sight of the fact that, far beyond the twin, transatlantic farces, a rather darker drama is beginning to play out in terms of world economic activity.

The first warning signs come from the freight industry, where US West Coast container traffic has slowed appreciably. Imports, indeed, have decelerated to an extent only exceeded—and then by the smallest of margins—a handful of times in the past 15 years, sending the growth rate plunging from August 2010’s chart-topping 26.4% to a 17-month low of 2.2%.

More broadly, while US intermodal rail traffic is still setting records, its tally now stands a bare 2.5% above the reading recorded at the same juncture in 2010—a sharp deceleration from that earlier period’s 26% YOY increase.

Matching this, across the Pacific, Shenzhen port numbers are also barely in the plus column, as of May-June, while Shanghai has dropped from 18% yoy in the whole of 2010, to a 16-month low over the quarter, touching 7.4% in June itself.

Then we have the IATA air freight numbers, recording their first global decline since the crisis, paced by a swingeing 9.8% YOY drop in the crucial Asia-Pacific region—a drop only exceeded during the worldwide export slump between Sep-08 & Mar-09.

Adding to series of cautious statements emanating from the shipping industry, several key machinery makers have also struck a less optimistic note, among them Atlas Copco, Caterpillar, Sandvik, Alstom, Terex, and Siemens. For an Austrian, signs of stress among these higher-order goods manufacturers are a clear warning of the chance of stormy weather ahead.

All of these micro-trends have again been borne out with the decline seen in various regional PMIs—notably in China and Germany—in the last month, as well as in the slowing of Taiwanese export orders and industrial production.

We have not yet tipped unequivocally into a renewed slump, but it is undeniable that the stimulus-fuelled rebound from the slump has more or less run its course and caution is the watchword.

A central tenet of Austrian Business Cycle Theory is that the first users’ advantage, conferred when an inflationary impulse is preferentially delivered within an economy, will eventually dissipate as relative prices adjust across the board. This implies that, to sustain their activity above the levels which would naturally prevail in the absence of that initial inflation, progressively larger (nominal) injections will be needed in what effectively becomes a Red Queen race to keep the productive structure extended beyond the length which voluntary saving alone would dictate.

In such circumstances, any slowdown—whether caused by an outright withdrawal of stimulus or simply a more rapid adaptation to its ongoing application—tends to a degenerative condition in which margins are first squeezed, before revenues themselves begin to decline in the previously favoured sectors and those of their immediate suppliers.

This sink-or-swim attribute of a modern, vertically-segmented economic system is one of the cardinal reasons why the fabled ’Soft Landing’ has historically proven so very hard to deliver. Given the unusual degree of structural elongation brought about by Asia’s investment-driven boom, it is all the more likely to prove to be beyond the capacity of the central planners this time around, too.