Although it might seem odd for a school of economics to largely ignore the role of money in the economy, this is indeed the case with traditional Keynesian economics. Declaring in 1963 that, “Inflation is, always and everywhere, a monetary phenomenon,” Milton Friedman sought to place money at the centre of economics where he and his fellow Monetarists believed it belonged. Keynesian policies continued to dominate into the 1970s, however, and were blamed by the Monetarists and others for the ‘stagflation’ of that decade—weak growth with rising inflation. Today, stagflation is re-appearing, the inevitable result of the aggressive, neo-Keynesian policy responses to the 2008 global financial crisis. In this report, I discuss the causes, symptoms and financial market consequences of the new stagflation, which could well be worse than the 1970s.

THE GOLDEN AGE OF KEYNESIANISM

During the ‘Roaring 20s’, US economists mostly belonged to various ‘laissez faire’ or ‘liquidationist’ schools of thought, holding that economic downturns were best left to sort themselves out, with a minimal role for official intervention. President Hoover’s Treasury Secretary Andrew Mellon (in)famously represented this view following the 1929 stock market crash when he admonished the government to stay out of private affairs and allow businesses and investors to “Liquidate! Liquidate! Liquidate!”

The severity of the Depression caught much of the laissez faire crowd off guard and thus by 1936, the year John Maynard Keynes published his General Theory, there was a certain open-mindedness around what he had to say, in particular that there was a critical role for the government to play in supporting demand during economic downturns through deficit spending. (There were a handful of prominent economists who did warn that the 1920s boom was likely to turn into a big bust, including Ludwig von Mises.1)

While campaigning for president in 1932, Franklin Delano Roosevelt famously painted Herbert Hoover as a lasseiz faire president, when in fact Hoover disagreed with Mellon. As Murray Rothbard and others have demonstrated, Hoover was a highly interventionist president, setting several major precedents on which FDR would subsequently expand.2 But all is fair in politics and FDR won that election and subsequent elections in landslides.

With the onset of war and the command war economy it engendered, in the early 1940s the economics debate went silent. With the conclusion of war, it promptly restarted. Friedrich von Hayek fired an early, eloquent shot at the Keynesians in 1946 with The Road to Serfdom, his warning of the longer-term consequences of central economic planning.

The Keynesians, however, fired back, and with much new ammunition. Beginning in the early 20th century, several US government agencies, including the Federal Reserve, began to compile vast amounts of economic statistics and to create indices to aggregate macroeconomic data. This was a treasure-trove to Keynesians, who sought quantitative confirmation that their theories were correct. Sure enough, in 1947, a new, definitive Keynesian work appeared, Foundations of Economic Analysis, by Paul Samuelson, that presented statistical ‘proof’ that Keynes was right.

One of Samuelson’s core contentions was that economic officials could and should maintain full employment (ie low unemployment) through the prompt application of targeted stimulus in recessions. As recessions ended, the stimulus should be withdrawn, lest price inflation rise to a harmful level. Thus well-trained economists keeping an eye on the data and remaining promptly reactive in response to changes in key macroeconomic variables could minimise the business cycle and prevent Depression.

For government officials, Samuelson’s work was the Holy Grail. Not only was this a theoretical justification for an active government role in managing the economy, as Keynes had provided; now there was hard data to prove it and a handbook for just how to provide it. A rapid, historic expansion of public sector macroeconomics soon followed, swelling the ranks of Treasury, Commerce, Labor Department and Federal Reserve employees.

CHICAGO AND THE ‘FRESHWATER’ DISSENT

Notwithstanding the establishment of this new economic mainstream and a public sector that wholeheartedly embraced it, there was some dissent, in particular at the so-called ‘freshwater’ universities of the American Midwest: Chicago, Wisconsin, Minnesota and St Louis, among others.

Disagreeing with key Keynesian assumptions and also with Samuelson’s interpretation of historical data, Monetarists mounted an aggressive counterattack in the 1960s, led by Milton Friedman of the Chicago School. Thomas Sargent, co-founder of Rational Expectations Theory, also took part.

The Chicago School disagreed that there was a stable relationship between inflation and employment that could be effectively managed through fiscal policy. Rather, Friedman and his colleagues argued that Keynesians had made a grave error in largely ignoring the role of money in the economy. Together with his colleague Anna Schwarz, Friedman set out to correct this in the monumental Monetary History of the United States, which re-interpreted the Great Depression, among other major events in US economic history, as primarily a monetary- rather than demand-driven phenomenon. Thus inflation, according to Friedman and Schwarz, was “always and everywhere a monetary phenomenon,” rather than a function of fiscal policy or other demand-side developments.

By the late 1960s the dissent played a central role in escalating policy disputes, due primarily to a prolonged expansion of US fiscal policy. Following Keynesian policy guidance, the government responded to the gentle recession of the early 1960s with fiscal stimulus. However, even after the recession was over, there was a reluctance to tighten policy, for reasons both foreign and domestic. At home, President Johnson promised a ‘Great Society’: a huge expansion of various programmes supposedly intended to help the poor and otherwise disadvantaged groups. Abroad, the Vietnam War had escalated into a major conflict and, combined with other Cold War military commitments, led to a huge expansion of the defence budget.

DE GAULLE AND INTERNATIONAL DISSENT

In the early 1960s a handful of prescient domestic observers had already begun to warn of the increasingly inflationary course of US fiscal and monetary policy (Henry Hazlitt wrote a book about it, What Inflation Is, in 1961.) In the mid-1960s this also became an important international topic. Under the Bretton-Woods system, the US was obliged to back dollars in circulation with gold reserves and to maintain an international gold price of $35/oz. In early 1965, as scepticism mounted that the US was serious about sustaining this arrangement, French President Charles De Gaulle announced to the world that he desired a restructuring of Bretton-Woods to place gold itself, rather than the dollar, at the centre of the international monetary system.

This prominent public dissent against Bretton-Woods unleashed a series of international monetary crises, roughly one each year, culminating in President Nixon’s decision to suspend ‘temporarily’ the dollar’s convertibility into gold in August 1971. (Temporarily? That was 43 years ago this month!)

The breakdown of Bretton-Woods would not be complete until 1973, when the world moved formally to a floating-rate regime unbacked by gold. However, while currencies subsequently ‘floated’ relative to one another, they collectively sank in purchasing power. The price of gold soared, as did the price of crude oil and many other commodities.

Rather than maintain stable prices by slowing the growth rate of the money supply and raising interest rates, the US Federal Reserve fatefully facilitated the dollar’s general devaluation

with negative real interest rates. While it took several years to build, in part because Nixon placed outright price controls on various goods, eventually the associated inflationary pressure leaked into consumer prices more generally, with the CPI rising steadily from the mid-1970s. Growth remained weak, however, as the economy struggled to restructure and rebalance. Thus before the decade was over, a new word had entered the economic lexicon: Stagflation.

STAGFLATION IS A KEYNESIAN PHENOMENON

Keynesians were initially mystified by this dramatic breakdown in the supposedly stable and manageable relationship between growth (or employment) and inflation. Their models said it couldn’t happen, so they looked for an explanation to deflect mounting criticism and soon found one: The economy had been hit by a ‘shock’, namely sharply higher oil prices! Never mind that the sharp rise in oil prices followed the breakdown of Bretton-Woods and devaluation of the dollar: This brazen reversal of cause and effect was too politically convenient to ignore. Politicians could blame OPEC for the stagflation, rather than their own policies. But an objective look at history tells a far different story, that the great stagflation was in fact the culmination of years of Keynesian economic policies. To generalise and to paraphrase Friedman, stagflation is, always and everywhere, a Keynesian phenomenon.

Why should this be so? Consider the relationship between real economic activity and the price level. If the supply of money is perfectly stable, then any negative ‘shock’ to the economy may reduce demand, but that will result in a decline rather than a rise in the general price level. The ‘shock’ might also increase certain prices in relative terms, but amidst stable money it simply cannot increase prices across the board, as is the case in stagflation.

They only way in which the toxic stagflationary mix of both reduced growth and rising prices can occur is if the money supply is flexible. Now this does not imply that a flexible money supply is in of itself a Keynesian policy, but deficit spending is far easier with a flexible money supply that can be increased as desired to finance the associated deficits. Yes, this then crowds out real private capital, with negative long-term consequences for economic health, but as we know, politicians are generally more concerned with the short-term and the next election.

CONTEMPORARY EVIDENCE OF STAGFLATION

Contemporary examples provide support for the reasoning above. It is instructive that two large economies, Japan and France, have been chronically underperforming in recent years, slipping in and out of recession. Both run chronic budget deficits in blatant Keynesian efforts to stimulate demand. In Japan, where the money supply is growing rapidly, inflation has been picking up despite weak growth: stagflation. In France, where the money supply has been quite stable, there is price stability: That is merely stagnation, not stagflation.

The UK, US and Germany have all been growing somewhat faster. Following the large devaluation of sterling in 2008, the UK experienced a multi-year surge in prices amidst weak growth, clearly a stagflationary mix. The US also now appears to be entering stagflation. Growth has been weak on average in recent quarters—outright negative in Q1 this year—yet inflation has now risen to 4% (3m annualised rate). Notwithstanding a surge in labour costs this year, the US Fed has, up to this point, dismissed this rise in CPI as ‘noise’. But then the Fed repeatedly made similar claims as CPI began to rise sharply in the mid-1970s.

In Japan, the UK and US, the stagflation is highly likely to continue as long as the current policy mix remains in place. (For all the fanfare surrounding the US Fed’s ‘tapering’, I don’t consider this terribly meaningful. Rates are still zero.) In France, absent aggressive structural reforms that may be politically impossible, the stagnation is likely to remain in place.

Germany is altogether a different story than the rest of these mature economies. While sharing the same, relatively stable euro money supply as France, the price level in Germany is also stable. However, Germany has been growing at a faster rate than most other developed economies, notwithstanding a smaller deficit. This is compelling evidence that Germany is simply a more competitive, productive economy than either the US or UK. But this is nothing new. The German economy has outperformed both the US and UK in nearly every decade since WWII. (Postwar rebuilding provided huge support in the 1950s and 1960s but those days are long past.)

The persistence of German economic outperformance through the decades clearly demonstrates the fundamental economic superiority of what is arguably the least Keynesian set of policies in the developed world. Indeed, Germans are both famed and blamed for their embrace of sound money and fiscal sustainability. ‘Famed’ because of their astonishing success; ‘blamed’ because of, well, because of their astonishing success relative to economic basket cases elsewhere in Europe and around the world. As I sometimes say in jest to those who ‘blame’ the Germans for the economic malaise elsewhere: “If only the Germans weren’t so dammed productive, we would all be better off!”

INVESTING FOR STAGFLATION

Stagflation is a hostile environment for investors. As discussed above, Keynesian policies require that the public sector siphon off resources from the private sector, thereby reducing the ability of private agents to generate economic profits. So-called ‘financial repression’, a more overt seizure of private resources by the public sector, is by design and intent hostile for investors. Regardless of how you choose to think about it, stagflation reveals previously unseen resource misallocations. As these become apparent, investors adjust financial asset prices accordingly. (Perhaps this is now getting under way. The Dow fell over 300 points yesterday.)

The most recent historical period of prolonged stagflation was the 1970s, although there have been briefer episodes since in various countries. Focusing here on the US, although there was a large stock market decline in 1973-4, the market subsequently recovered these losses and then roughly doubled in value. The bond market, by contrast, held up during the first half of the decade but, as stagnation gradually turned into stagflation, bonds sold off and were sharply outperformed by stocks.

That should be no surprise, as inflation erodes the nominally fixed value of bonds. Stock prices, however, can rise along with the general price level along as corporate revenues and profits also rise. It would seem safe to conclude, therefore, that in the event stagflationary conditions intensify from here, stocks will outperform bonds.

While that might be a safe conclusion, it is not a terribly helpful one. Sure, stocks might be able to outperform bonds in stagflation but, when adjusted for the inflation, in real terms they can still lose value. Indeed, in the 1970s, stock market valuations failed to keep pace with the accelerating inflation. Cash, in other words, was the better ‘investment’ option and, naturally, a far less volatile one.

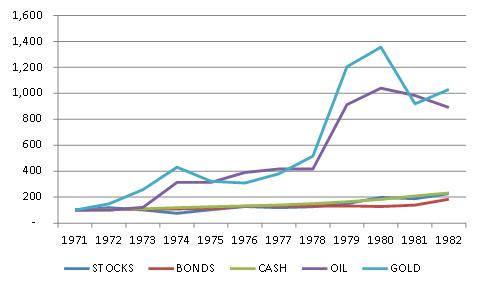

Best of all, however, would have been to avoid financial assets and cash altogether and instead to accumulate real assets, such as gold and oil. (Legendary investors John Exter and John van Eck did precisely this.) The chart below shows the total returns of all of the above and the relative performance of stocks, bonds and cash appears irrelevant when compared to the soaring prices of gold and oil, both of which rose roughly tenfold.

REAL VS NOMINAL ASSETS IN STAGFLATION

(Jan 1971 = 100)

Source: Bloomberg; Amphora

Some readers might be sceptical that, from their current starting point, gold, oil or other commodity

prices could rise tenfold in price from here. Oil at $100/bbl sounds expensive to those (such as I) who remember the many years when oil fluctuated around $20. Gold at $1,300 also seems expensive compared to the sub-$300 price fetched by UK Chancellor Brown in the early 2000s. In both cases, prices have risen by a factor of 4-5x. Note that this is the rough order of magnitude that gold and oil rose into the mid-1970s. But it was not until the late 1970s that both really took off, leaving financial assets far behind.

If anything, a persuasive case can be made that the potential for gold, oil and other commodity prices to outperform stocks and bonds is higher today than it was in the mid-1970s. Monetary policies around the world are generally more expansionary. Government debt burdens and deficits are far larger. If Keynesian policies caused the 1970s stagflation, then the steroid injection of aggressive Keynesian policies post-2008 should eventually result in something even more spectacular.

While overweighting commodities can be an effective, defensive investment strategy for a stagflationary future, it is important to consider how best to implement this. Here at Amphora, we provide investors with an advisory service for constructing commodity portfolios. Most benchmark commodity indices and the ETFs tracking them are not well designed as investment vehicles for a variety of reasons. In particular, they do not provide for efficient diversification and their weightings are not well-specified to a stagflationary environment. With a few tweaks, however, these disadvantages can be remedied, enabling a commodity portfolio to produce the desired results.

CURRENT COMMODITY OPPORTUNITIES

For those inclined to trade commodities actively, and relative to each other, there are an unusual number of opportunities at present. First, grains are now unusually cheap, especially corn. This is understandable given current global weather patterns supportive of high yields, but beyond a certain point producers are fully hedged and/or are considering withholding some production to sell once prices recover. That point is likely now close.

Second, taking a look at tropical products, cotton has resumed the sharp slide that began earlier this year. As is the case with grains, we are likely nearing the point where producer hedging and/or holding out for higher prices will support the price. By contrast, cocoa prices continue their rise and I note that several major chocolate manufacturers have recently increased prices sharply to maintain margins. That is a classic indication that prices are near a peak.

Third, livestock remains expensive. Hog prices have finally begun to correct lower but cattle prices are at record highs. There are major herd supply issues that are not easily resolved in the near-term but consumers are highly price sensitive in the current environment and substitution into pork or poultry products is almost certainly now taking place around the margins. Left to run for awhile, this is likely to place a lid on cattle prices, although I do expect them to remain elevated for a sustained period until herds have had a chance to re-build.

Fourth, following a brief correction lower several weeks ago, palladium prices have risen back near to their previous highs of just under $900/oz. Palladium now appears expensive relative to near-substitute platinum; to precious and base metals generally; and relative to industrial commodities. The primary source of demand, autocatalysts, has remained strong due to auto production, but recent reports of rising unsold dealer inventory in a handful of major countries, including the US, may soon weaken demand. In the event that the fastest growing major auto markets—the BRICS—begin to slow, then a sharp decline in palladium to under $700 is likely.

Finally, a quick word on silver and gold. While both have tremendous potential to rise in a stagflationary environment, it is worth noting that, following a three-year correction, they appear to have found long-term support. Thus I believe there is both near-term and well as longer-term potential and I would once again recommend overweighting both vs industrial commodities.

1Von Mises not only warned of a financial crash and severe economic downturn in 1929; he refused the offer of a prominent position at the largest Austrian bank, Kreditanstalt, around the same time, not wanting to be associated with what he correctly anticipated would soon unfold. A Wall Street Journal article discussing this period in von Mises’ life is linked here.

2A classic revisionist view is that of Murray Rothbard, AMERICAS GREAT DEPRESSION. More recent scholarship by Lee Ohanian has added much additional detail to Rothbard’s work. I briefly touch on this subject in my book and also in a previous Amphora Report, THE RIME OF THE CENTRAL BANKER, linked here.

Why pick on just the Keynesians and portray the Monetarists as the good guys when, in my view, the Monetarists are just as much to blame for the mess .

Many Monetarists are also Misian and Smithsonian who believe in the free market except when it comes to money and then they become Statists.

A little bit elitist to say the least, they are the ones that insist on governments setting interest rates and controlling the money supply and always getting it wrong.

Growth of the economy will happen in line with population growth and consumption aspirations whilst interest rates will ideally set themselves as a result of the actions of borrowers and savers. Absolutely no need for government involvement at all and, the less governments do in general the more the efficiently will the free market operate.

That money does not need to be managed is perfectly illustrated in your article viz the value of gold and other commodities against the value of paper money: unmanaged they hold their value and increase in value only in response to demand, exactly as money should, whilst the value of paper money has dramatically declined in value to the point where it is no longer seen as a good store of value..

Setting interest rates at near zero will be eventually seen as a great mistake, allowing malinvestments to sustain and unduly fuelling assets to an unsustainable level, and then- another bust.

Hello ‘Wargames’:

I agree that Monetarism is flawed in various respects, in particular that it does not allow for a properly free market in providing society with the money it desires, in the quantity and quality it desires. At no point in this post do I advocate Monetarism, although I do reference its assumption that money matters to help illustrate that Keynesianism leads to stagflation and to suboptimal economic outcomes more generally, as is once again becoming evident.