Last year, in a paper entitled The Stock Market Crash Really Did Cause the Great Recession – Roger Farmer of UCLA argued that the collapse in the stock market was the cause of the Great Recession:-

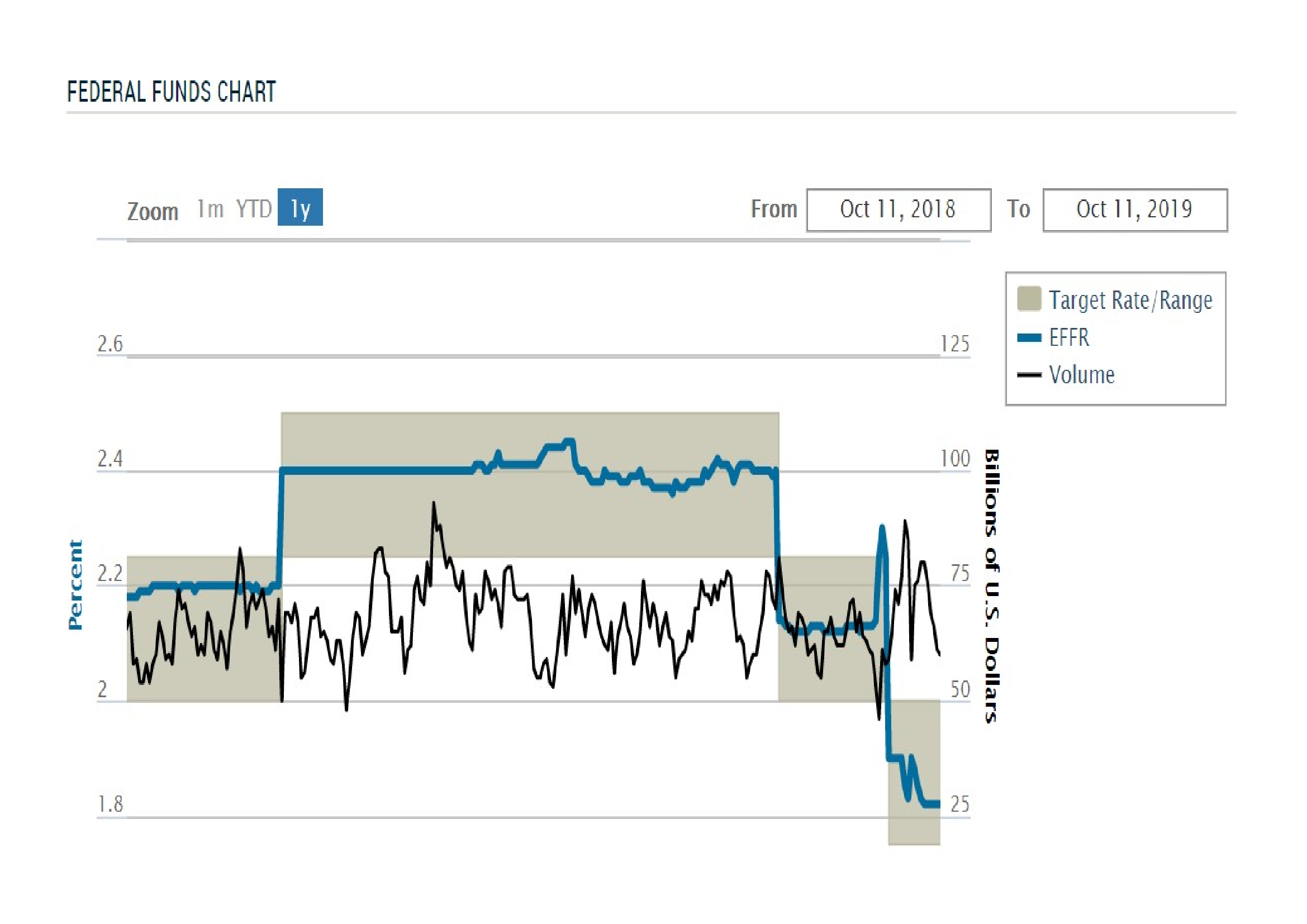

In November of 2008 the Federal Reserve more than doubled the monetary base from eight hundred billion dollars in October to more than two trillion dollars in December: And over the course of 2009 the Fed purchased eight hundred billion dollars worth of mortgage backed securities. According to the animal spirits explanation of the recession (Farmer, 2010a, 2012a,b, 2013a), these Federal Reserve interventions in the asset markets were a significant factor in engineering the stock market recovery.

The animal spirits theory provides a causal chain that connects movements in the stock market with subsequent changes in the unemployment rate. If this theory is correct, the path of unemployment depicted in Figure 8 is an accurate forecast of what would have occurred in the absence of Federal Reserve intervention. These results support the claim, in the title of this paper, that the stock market crash of 2008 really did cause the Great Recession.

Central banks (CBs) around the globe appear to concur with his view. Their response to the Great Recession has been the provision of abundant liquidity – via quantitative easing – at ever lower rates of interest. They appear to believe that the recovery has been muted due to the inadequate quantity of accommodation and, as rates drift below zero, its targeting.

The Federal Reserve (Fed) was the first to recognise this problem, buying mortgages as well as Treasuries, perhaps guided by the US Treasury’s implementation of TARP in October 2008. The Fed was fortunate in being unencumbered by the political grid-lock which faced the European Central Bank (ECB). They acted, aggressively and rapidly, hoping to avoid the policy mistakes of the Bank of Japan (BoJ). The US has managed to put the great recession behind it. But at what cost? Only time will tell.

Other major CBs were not so decisive or lucky. In the immediate aftermath of the sub-prime crisis the Swiss Franc (CHF) rose – a typical “safe-haven” reaction. The SNB hung on grimly as the CHF appreciated, especially against the EUR, but eventually succumbed to “the peg” in September 2011 after the Eurozone (EZ) suffered its first summer of discontent. It was almost a year later before ECB President Draghi uttered his famous “Whatever it takes” speech on 26thJuly 2012.

Since 2012 government bond yields in the EZ, Switzerland, Japan and the UK have fallen further. In the US yields recovered until the end of 2013 but have fallen once more as international institutions seek yield wherever they can.

By 2013 CBs had begun to buy assets other than government bonds as a monetary exercise, in the hope of simulating economic growth. Even common stock became a target, since they were faced with the same dilemma as other investors – the need for yield.

In late April 2013 Bloomberg – Central Banks Load Up on Equities observed:-

Central banks, guardians of the world’s $11 trillion in foreign-exchange reserves, are buying stocks in record amounts as falling bond yields push even risk-averse investors toward equities.

In a survey of 60 central bankers…23 percent said they own shares or plan to buy them. The Bank of Japan, holder of the second-biggest reserves, said April 4 it will more than double investments in equity exchange-traded funds to 3.5 trillion yen ($35.2 billion) by 2014. The Bank of Israel bought stocks for the first time last year while the Swiss National Bank and the Czech National Bank have boosted their holdings to at least 10 percent of reserves.

…The SNB allocated 82 percent of its 438 billion Swiss francs ($463 billion) in reserves to government bonds in the fourth quarter, according to data on its website. Of those securities, 78 percent had the top, AAA credit grade and 17 percent were rated AA.

…The survey of 60 central bankers, overseeing a combined $6.7 trillion, found that low bond returns had prompted almost half to take on more risk. Fourteen said they had already invested in equities or would do so within five years.

…Even so, 70 percent of the central bankers in the survey indicated that equities are “beyond the pale.”

…the SNB has allocated about 12 percent of assets to passive funds tracking equity indexes. The Bank of Israel has spent about 3 percent of its $77 billion reserves on U.S. stocks.

…the BOJ announced plans to put more of its $1.2 trillion of reserves into exchange-traded funds this month as it doubled its stimulus program to help reflate the economy. The Bank of Korea began buying Chinese shares last year, increasing its equity investments to about $18.6 billion, or 5.7 percent of the total, up from 5.4 percent in 2011. China’s foreign-exchange regulator said in January it has sought “innovative use” of its $3.4 trillion in assets, the world’s biggest reserves, without specifying a strategy for investing in shares.

Reserves have increased at a slower pace since 2012, but the top 50 countries still accounted for $11.4trln, according to the latest CIA Factbook estimates. The real growth has been in emerging and developing countries – according to IMF data, since 2000, in the wake of the Asian crisis, their reserves grew from $700bln to above $8trln.

By June 2014 the Financial Times – Beware central banks’ share-buying sprees was sounding the alarm:-

An eye-catching report this week said that “a cluster of central banking investors has become major players on world equity markets”. An important driver was revenues foregone on bond portfolios.

Put together by the Official Monetary and Financial Institutions Forum, which brings together secretive and normally conservative central bankers, the report’s conclusions have authority. Some equity buying was in central banks’ capacity as, in effect, sovereign wealth fund managers. China’s State Administration of Foreign Exchange, which has $3.9tn under management, has become the world’s largest public sector holder of equities.

The boundary, however, with monetary policy making is not always clear. According to the Omfif report, China’s central bank itself “has been buying minority equity stakes in important European companies”.

…Central bank purchases of shares are not new. The Dutch central bank has invested in equities for decades. The benchmark for its €1.4bn portfolio is the MSCI global developed markets index.

The Italian, Swiss and Danish central banks also own equities. Across Europe, central banks face pressures from cash-strapped governments to boost income. As presumably cautious and wise investors, they have also been put in charge of managing sovereign wealth funds – Norway’s, for instance.

…the Hong Kong Monetary Authority launched a large-scale stock market intervention in 1998, splashing out about $15bn – and ended up making a profit. Since the Asian financial crisis of that year, official reserves have expanded massively – far beyond what might be needed in future financial crises or justified by trade flows.

The article goes on to state that CB transparency is needed and that it should be made clear whether the actions are monetary policy or investment activity. Equities are generally more volatile than bonds – losses could lead to political backlash, or worse still, undermine the prudent reputation of the CB itself.

Here is an example of just such an event, from July last year, as described by Zero Hedge – The Swiss National Bank Is Long $94 Billion In Stocks, Reports Record Loss Equal To 7% Of Swiss GDP:-

…17%, or CHF91 ($94 billion) of the foreign currency investments and CHF bond investments assets held on the SNB’s balance sheet are foreign stocks…

…In other words, the SNB holds 15% of Switzerland’s GDP in equities!

Zero Hedge goes on to remonstrate against the lack of transparency of other CBs equity investment balances – in particular the Fed.

The ECB, perhaps due to its multitude of masters, appears reluctant to follow the lead of the SNB. In March 2015 it achieved some success by announcing that it would buy Belgian, French, Italian and Spanish bonds, under its QE plan, in addition to those of, higher rated, Finland, Germany, Luxembourg and the Netherlands. EZ Yield compression followed with Italy and Spain benefitting most.

The leading exponent of this “new monetary alchemy” is the BoJ. In an October 2015 report from Bloomberg – Owning Half of Japan’s ETF Market Might Not Be Enough for Kurodathe author states:-

With 3 trillion yen ($25 billion) a year in existing firepower, the BOJ has accumulated an ETF stash that accounted for 52 percent of the entire market at the end of September, figures from Tokyo’s stock exchange show.

…Japan’s central bank began buying ETFs in 2010 to spur more trading and promote “more risk-taking activity in the overall economy.” Governor Haruhiko Kuroda expanded the program in April 2013 and again last October.

Source: Bloomberg, TSE

More ETFs can be created to redress the balance, or the BoJ may embark on the purchase of individual stocks. They announced a small increase in ETF purchases in December, focused on physical and human capital firms – also advising that shares they bought from distressed financial institutions in 2002 will be sold (very gradually) at the rate of JPY 300bln per annum over the next decade. At the end of January the BoJ decided to adopt negative interest rate policy (NIRP) rather than expand ETF and bond purchases – this saw the Nikkei hit its lowest level since October 2014 whilst the JYP shed more than 8% against the US$. I anticipate that they will soon increase their purchases of ETFs or stocks once more. The NIRP decision was half-hearted and BoJ concerns, about corporates and individuals resorting to cash stashed in safes, may prove well founded – So it begins…Negative Interest rates Trickle Down in Japan – Mises.org discusses this matter in greater detail.

In early March the ECB acted with intent, CNBC – ECB pulls out all the stops, cuts rates and expands QE takes up the story:-

…the ECB announced on Thursday that it had cut its main refinancing rate to 0.0 percent and its deposit rate to minus-0.4 percent.

“While very low or even negative inflation rates are unavoidable over the next few months as a result of movement in oil prices, it is crucial to avoid second-round effects,” Draghi said in his regular media conference after the ECB statement.

…The bank also extended its monthly asset purchases to 80 billion euros ($87 billion), to take effect in April.

…the ECB will add corporate bonds to the assets it can buy — specifically, investment grade euro-denominated bonds issued by non-bank corporations. These purchases will start towards end of the first half of 2016.

…the bank will launch a new series of four targeted longer-term refinancing operations (TLTROs) with maturities of four years, starting in June.

The Communique from the G20 meeting in Shanghai alluded to the need for increased international cooperation, but it appears that a sub-rosa agreement may have been reached to insure the Chinese did not devalue the RMB – in return for a cessation of monetary tightening by the Fed.

In an unusually transparent move, a report appeared on March 31st on Reuters – China forex regulator buys $4.2 bln in stocks via new platform:-

Buttonwood Investment Platform Ltd, 100 percent owned by the State Administration of Foreign Exchange (SAFE), and Buttonwood’s two fully-owned subsidiaries, have bought shares in a total of 13 listed companies, the newspaper reported, citing top 10 shareholder lists in the companies latest earnings reports.

Shanghai Securities News said the investments are part of SAFE’s strategy to diversify investment channels for the country’s massive foreign exchange reserves.

Recent earnings filings show Buttonwood is among the top 10 shareholders of Bank of China, Bank of Communications , Shanghai Pudong Development Bank , Everbright Securities and Industrial and Commercial Bank of China.

Conclusions and investment opportunities

The major CBs are beginning to embrace the idea of providing capital to corporates via bond or stock purchases. With next to no yield available from government bonds, corporate securities appear attractive, especially when one has the ability to expand ones balance sheet, seemingly, without limit.

The CBs are unlikely to buy when the market is strong but will provide liquidity in distressed markets. Once they have purchased securities the “free-float” will be almost permanently reduced. The lack of, what might be termed, “trading liquidity”, which has been evident in government bond markets, is likely to spill over into those corporate bonds and ETFs where the CBs hold a significant percentage. In the UK, under our takeover code, a 30% holding in a stock would obligate the holder to make an offer for the company – the 52% of outstanding ETFs held by the BoJ already seems excessive.

The ECB has plenty of government, agency and corporate bonds to purchase, before it moves on to provide permanent equity capital. The BoE and the Fed are subject to less deflationary forces; they will be the last guests to arrive at the “closet nationalisation” party. The party, nonetheless, is getting underway. Larger companies will benefit to a much greater extent than smaller listed or unlisted corporations because the CBs want to appear to be “indiscriminate” buyers of stock.

As the pool of available bonds and stocks starts to dry up, trading liquidity will decline – markets will become more erratic and volatile. Of greater concern in economic terms, malinvestment will increase; interest rates no longer provide signals about the value of projects.

For stocks, higher earning multiples are achievable due to the rising demand for equities from desperate investors with no viable “yield” alternative. CBs are unelected stewards on whom elected governments rely with increasing ease. For notionally independent CBs to purchase common stock is de facto nationalisation. The economic cost of an artificially inflated stock market is difficult to measure in conventional terms, but its promotion of wealth inequality through the sustaining of asset bubbles will do further damage to the fabric of society.