“Wherever there’s injustice, oppression and suffering, America will show up six months late and bomb the country next to where it’s happening.”

- From Give War a Chance by P.J. O’Rourke, cited by Jonathan Allum of SMBC Nikko Capital Markets in The Blah !

There’s a phrase that Warren Buffett has used on numerous occasions that appears to have come via Dr Johnson:

“The chains of habit are too light to be felt until they are too heavy to be broken.”

The shorter version: certain longstanding habits can be intensely dangerous. As Niels Jensen of Absolute Return Partners points out, growth stocks have outperformed value stocks for many years, leading many investors to assume that this outperformance has now become a permanent feature of the stock market. This assumption overlooks the power of the relationship between stocks and the bond market:

“When bond yields decline, growth stocks outperform value stocks, and vice versa when bond yields rise. With declining bond yields for most of the last 35 years, it is easy to understand why many investors are infatuated with growth stocks. An entire generation of investors have never seen value stocks outperform growth stocks, and those who have hardly remember because it is more than 35 years ago.

“Now, assuming we stand in front of a multi-year rise in interest rates, even if it is of modest proportions (as I think it will be), all that could be about to change. Investors who are wedded to their growth stock rule may be disappointed, while those who are prepared to adapt to the changing regime are more likely to outperform.”

In other words, for the historic outperformance of growth versus value to continue, interest rates may need to go lower or at least stay low for the foreseeable future.

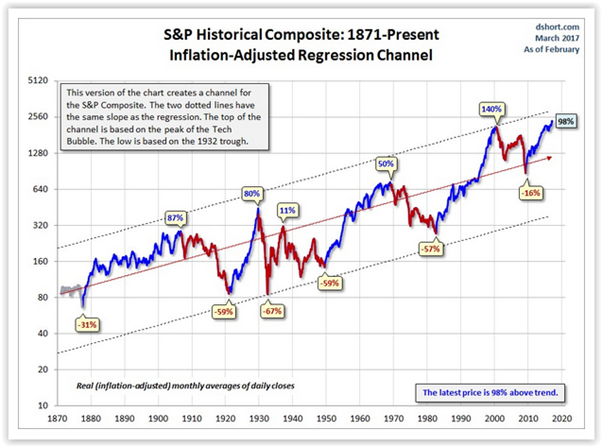

By any objective assessment, US stock markets are hardly cheap. Jensen cites the inflation-adjusted trend for the S&P Composite Index, shown below, which indicates that the US market is currently 98% above its historic trend: “the secular bull market we have been in since 2009 is (at the time of writing) 98% above the long-term trend line but, when secular bear markets take charge, equity markets rarely ‘just’ go back to the trend line. Most of them go all the way back to the bottom of the channel.

This leads me to conclude that equities in general, and US equities in particular, are priced for problems in the years to come; hence I would allocate only a limited amount to this asset class at present.”

Sources: Jill Mislinski, Advisor Perspectives, March 2017, www.advisorperspectives.com and Absolute Return Partners

Could it be, though, that the world has changed, in a way that would justify markedly higher valuations for the US stock market ? This is the question posed by Jeremy Grantham in his latest quarterly commentary for GMO. As he points out in the chart below, the average p/e ratio for the S&P 500 for the period prior to 1997 was 13.95. For the period subsequent to 1997 it has been almost twice as high, at 23.36. Anybody waiting for mean reversion in valuations for the US stock market has had a long and so far futile wait. And as Grantham goes on to show, both the return on sales for the S&P 500 and the share of US GDP held by corporate profits have also trended higher since 1997.

For Grantham, too, squaring this circle will likely depend on the future behaviour of the bond market.

“So, to summarize, stock prices are held up by abnormal profit margins, which in turn are produced mainly by lower real rates, the benefits of which are not competed away because of increased monopoly power, etc. What, we might ask, will it take to break this chain? Any answer, I think, must start with an increase in real rates.”

So to forecast the outlook for stocks, one needs to forecast the outlook for the bond market. But this is easier said than done. More than 8 years of QE have driven the prices of all kinds of assets a long way from their “fundamental” level and there can be no easy presumption that the genie of QE is about to vanish back into a bottle at the Marriner Eccles Building, or anywhere else.

There are two other words that are driving financial markets today. Jeremy Grantham has previously described them as “career risk”:

“The central truth of the investment business is that investment behaviour is driven by career risk. In the professional investment business we are all agents, managing other peoples’ money. The prime directive, as Keynes knew so well, is first and last to keep your job. To do this, he explained that you must never, ever be wrong on your own. To prevent this calamity, professional investors pay ruthless attention to what other investors in general are doing. The great majority go with the flow, either completely or partially. This creates herding, or momentum, which drives prices far above or far below fair price. There are many other inefficiencies in market pricing, but this is by far the largest.”

There is, however, a way of resolving these various problems. Avoid the use of benchmarks. Abandoning the tyranny of benchmarking at an asset class level frees one from an overdependence on what are almost certainly overpriced government bonds. And abandoning the tyranny of benchmarking at the equity level frees one from an overdependence on what seems to be a clearly overpriced US stock market. The apparent overvaluation of US stocks is only a problem if you are forced to own them to begin with. Avoiding US stocks does not mean avoiding stocks, especially those of profitable businesses in Asia trading at extremely undemanding multiples, both on a relative and absolute basis.

Jeremy Grantham has also written well in the past about three strategies investors can use to survive seemingly irrational markets:

- Allow a generous Benjamin Graham-like ‘margin of safety’ in your stock selection;

- Stay reasonably diversified;

- Never use leverage.

The investment world may seem irrational and many markets may be expensive, but sound advice may be priceless.