The euro system and its currency are descending into crisis. Comprised of the ECB and the National Central Banks, the system is over its head in balance sheet debt, and it is far from clear how that can be resolved.

Normally, a central bank is easy to recapitalise. But in the case of the euro system, when the lead institution and all its shareholders need to be recapitalised all at the same time the challenge could be impossible. And then there’s all the imbalances in the TARGET2 system to resolve as well before national legislatures can sign it all off. Additionally, but part of the TARGET2 problem there’s the repo market with €8.7 trillion outstanding, set to implode on rising interest rates, destroying commercial bank balance sheets which are already highly leveraged.

This goes some way to explaining the deep reluctance the ECB has about raising interest rates. While producer prices in key member states are rising at over 30% year-on-year, and consumer prices by over 8%, the ECB keeps its deposit rate at minus 0.5%. It knows that if euro bond yields go any higher their situation which is already untenable will disintegrate into a full-blown crisis.

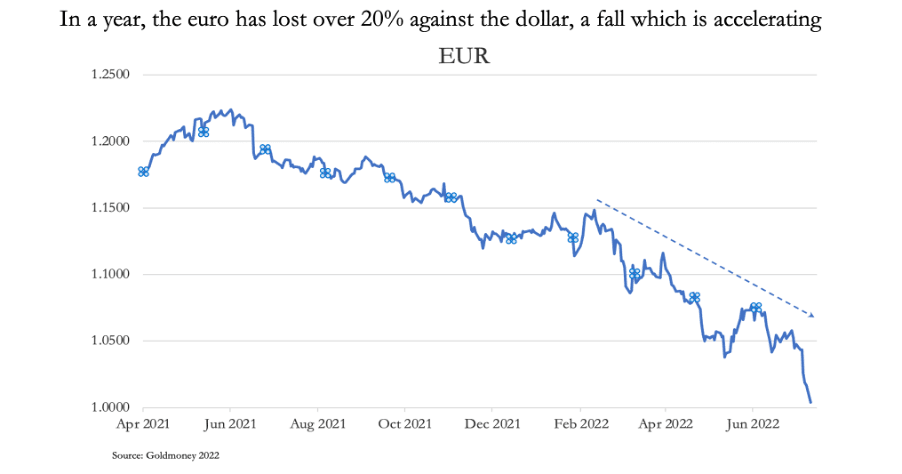

Therefore, the euro is sliding. Markets can see that all the ECB is doing is talking the talk and otherwise is frozen into inaction.

Fiddling while Rome burns…

At a political level there appear to be terrifying levels of ignorance about the economic consequences of continuing to punish Britain for Brexit (yes, that still rankles) and now ostracising Russia for its belligerence at a time when the EU’s own economy is teetering on the edge of a financial and economic catastrophe. The EU exercises its political agendas despite any economic mayhem created.

Russia is a far more serious issue than Brexit ever was. The EU has, to varying degrees, disposed of its fossil fuel capacity to placate environmentalists, exporting their production to nations not so squeamish about fashionable climate change strictures. Consequently, the EU has become highly dependent on Russian natural gas and oil, which in cavalier fashion it has decided to do without to punish Russia over its invasion of Ukraine.

The economic consequences have been to put Germany’s economy on life support with its industrial limbs beginning to shut down, along with the productive capacity of many other EU states. In the coming months there will be food shortages exacerbated by lack of fertiliser supplies. Then there will be winter without heating fuel and frequent power cuts. And winter with food shortages in a continental climate is no joke. They will spark riots and growing political instability.

The financial consequences stem partly from bank exposure to Russian entities, but far more important is the effect of soaring producer and consumer prices on the entire Eurozone financial structure. The euro system has depended on redistributing wealth from Germany and the fiscally conservative northern states to bail out the profligate south using suppressed interest rates. That scheme is now kaput.

The ECB, and the euro system of shareholder national central banks, has metaphorically been caught with their collective trousers down. Having suppressed interest rates into negative territory, they allowed member governments to borrow ultra-cheaply. Now that Eurozone CPI is rising at 8.6% and Germany’s producer prices are up 33.6%, either interest rates must rise smartly or the euro crashes. Our headline chart of the euro/dollar rate at the top of this article refers to the market’s reaction so far.

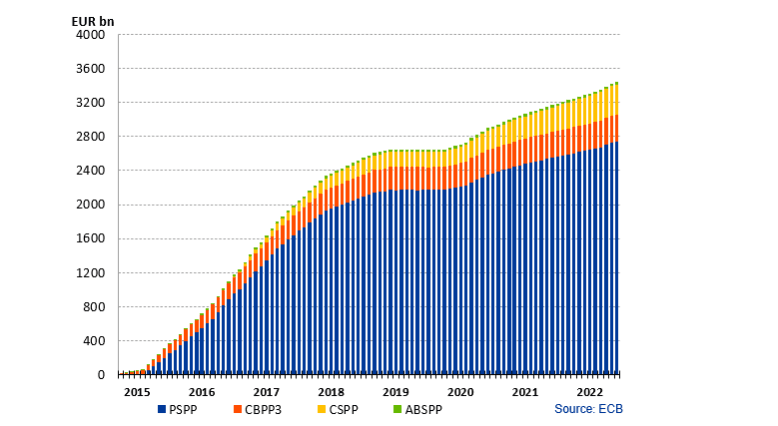

Bonds in the ECB’s Asset Purchase Programme have accumulated as shown in the chart below, split out into the Public Sector Purchase Programme (PSPP), Corporate Sector Purchase Programme (CSPP), Asset-backed Securities Purchase Programme (ABSPP) and the Third Covered Bond Purchase Programme (CBPP3). In June, they totalled €3,265,172 million.

From a year ago, government bonds have risen in yield from minus 0.5% to 1.36% for Germany’s 10-year bond, an overall rise of 1.86%. The rise in yield for a similar Italian bond is 2.87%, Spain’s 2.3%, France’s 2%, and Greece’s 3.2%. Given that government stock is 65% of the total, the rest being generally higher yielding corporate bonds, a conservative estimate is that if the portfolio has an average maturity of ten years the mark-to-market loss from a year ago is already in the region of €750bn. This is almost seven times the combined euro system balance sheet equity and reserves of €109.272bn. And as yields rise further, euro system losses of double that are easy to imagine.

Doubtless, if challenged the ECB would claim the euro system will hold these bonds to maturity, so they will continue to value them at par. But the euro system is unlikely to cease funding member states by inflationary means. And we cannot ignore the likelihood of further rises in yield due to the disparity between current interest rates (the ECB’s deposit rate is minus 0.5%) and a CPI heading towards annual increases of 10%.

The monetary error behind the EU concept

The concept underlying the EU can be summed up as the socialising of the wealth of the northern states to subsidise the southern and less wealthy member nations. In keeping with its post-war low political profile, Germany went along with the European project’s evolution from being a trading bloc into a currency union.

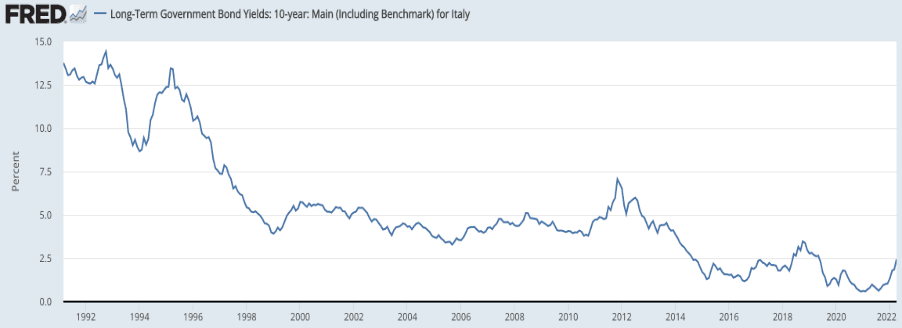

The euro was intended to be a leveller, enabling nations like Italy, Spain and Greece to piggyback on Germany’s debt rating, on the statist argument that being issued by a sovereign nation tied into a common currency and settlement system, there is little difference between owning German and Italian, or even Greek sovereign debt. The consequences were that through investing institutions Germany’s savers directly and indirectly subsidised debt issued at levels that fail to compensate for the borrower’s true risk. The FRED chart below shows the effect on otherwise risky Italian 10-year benchmark bond yields.

In the run up to the replacement of national currencies by the euro, the Maastricht rules for qualification were ignored. Otherwise, Italy’s level of sovereign debt would have disqualified its entry. The market rate for Italy’s 10-year government bond was a yield of 12.4% when the Maastricht treaty setting the conditions for entry into monetary union came into effect in 1992. Germany’s equivalent benchmark yielded 8.3% for a differential of 4.1%. Today the German benchmark yields 1.35% and the Italian 3.37%, a difference of 2.2%. Not only has the gap converged, but by the end of 2021 the quantity of Italian government debt had increased to over 150% of GDP.

Similar examples can be shown of the other PIGS — Portugal, Greece, and Spain. Clearly, the evidence is that markets are not pricing sovereign risk as they should, and their yields are being heavily suppressed. Stuck in debt traps, even more debt needs to be issued because the outlook for budget deficits in these nations is simply dire, made worse by a Eurozone economy on the verge of an energy induced meltdown.

The ECB and its impossible task

So far, we have laid bare the consequences of the energy crisis for the eurozone economy and the losses that arise on the euro system balance sheets. Overseeing it all is the ECB’s president, who previously served as Chair of the IMF and before that held roles in the French government, including economy and finance minister. With this experience she was appointed to the ECB as a safe pair of hands. And as such, she has inherited an impossible position, because she has no mandate to moderate the ECB’s inflationary policies.

More correctly, Lagarde inherited two impossibilities. The first is to continue to distribute Germany’s national wealth to support the PIGS, and the second is a banking system that is well and truly broken. And as stated earlier, Germany itself is now on life support.

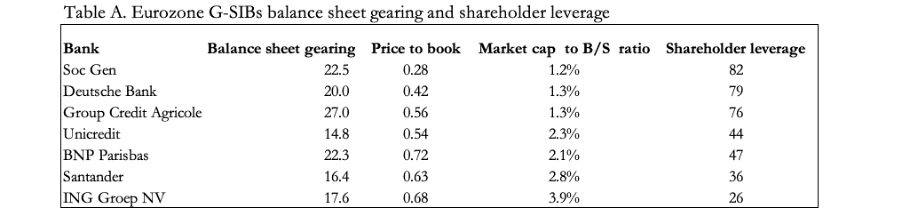

Table A shows the relationship between the Eurozone G-SIBs’ balance sheet totals, their balance sheet equity, and market capitalisations to illustrate the fragility of the Eurozone’s global systemically important banks (G-SIBs).

G-SIBs are required to have extra capital buffers designed to ensure they do not create or spread counterparty risk. The liquidity is created from the structure of the total balance sheet and does not require shareholders’ capital to be involved. Nevertheless, gearing between total assets and balance sheet equity (which includes undistributed profits and ranking capital other than common shares) average just over twenty times for the Eurozone G-SIBs, ranging from Credit Agricole at 27 times to Unicredit at 14.8 times.

Price to book values for all these banks are at a discount, some deep enough to call their immediate survival into question, given that an economic downturn for the Eurozone is now in progress. If they are to protect their shareholders’ equity, these banks have no alternative but to contract their balance sheets where they can. Indeed, when it occurs, a downturn in GDP is due in large measure to the withdrawal of bank credit. This is bound to expose and create bad debts, which threatens to wipe out shareholders’ capital entirely.

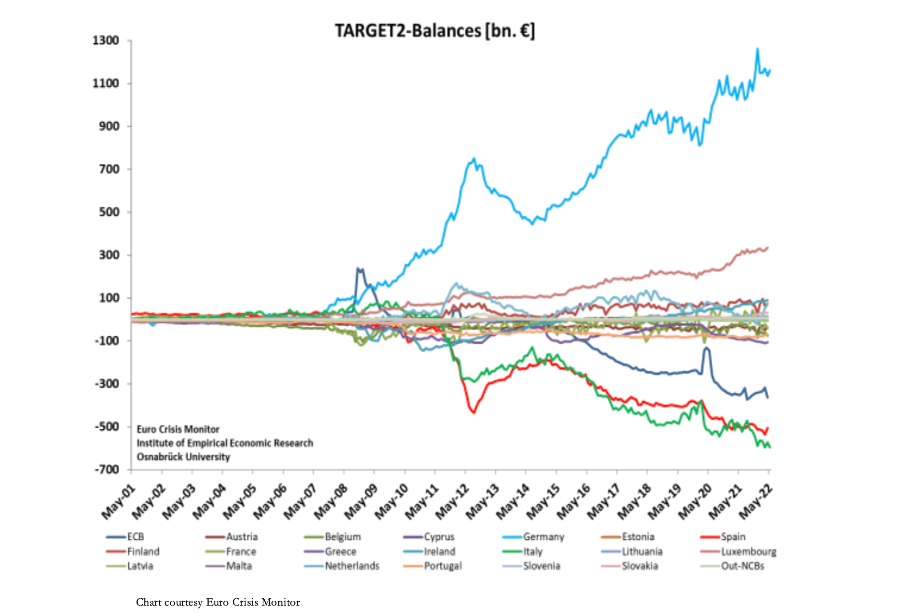

Much of the devil is to be found in those non-performing loans. It has become routine for national regulators to deem them performing so that they can act as collateral for loans from the national central bank. When they then become lost in the TARGET2 settlement system they are forgotten, and miraculously the commercial bank appears solvent again. But TARGET2 becomes riddled with those bad debts and imbalances arise as the next chart from the Euro Crisis Monitor shows. In theory, these imbalances should not arise, and before the Lehman crisis it was generally true.

This is one way Germany’s national savings are being redistributed to the PIGS. At end-May, Germany’s Bundesbank was “owed” €1,160bn.

At the same time, the greatest debtors, Italy, Spain, Greece, and Portugal have combined TARGET2 debts of €1,255bn. But the most rapid deterioration for its size is in Greece’s negative balance, more than tripling from €25.7bn at end-2019 to €106bn in April. Spain’s deficit is also increasing at a worrying pace, up from €392.4bn to €505bn, and Italy’s from €439.4bn to €597bn.

If one national central bank runs a Target2 deficit with the other central banks, it is because it has loaned money to its commercial banks to cover payments, instead of progressing them through the settlement system. These loans to commercial banks appear as an asset on the national central bank’s balance sheet, which is offset by a liability to the ECB’s Eurosystem through TARGET2 — hence the PIGS’ deficits. In effect, central banks running deficits are providing their commercial banks with extra liquidity. This is mostly done through repurchase agreements, more of which anon. The fact that commercial banks in the PIGS require this liquidity is a red flag.

Under the rules, if the TARGET2 system fails, the costs are shared out by the ECB on the pre-set capital key formula based on the equity ownership of ECB shares by the national central banks. The ECB itself has a deficit of €365bn arising from non-payment of bond purchases by national central banks acting on its behalf. These non-payments are recorded as assets on the national central bank balance sheets, reducing their net TARGET2 liabilities. The extent to which Italian, Spanish, Greek, and Portuguese central banks are owed money by the ECB for bond purchases reduces their apparent TARGET2 obligations. For these NCBs, the true position could be considerably worse than the declared figures suggest.

Furthermore, it is in the interest of a national central bank to run a greater deficit in relation to its capital key by supporting the insolvent commercial banks in its jurisdiction. That way, if TARGET2 fails, its write-off becomes greater than its contribution to the ECB’s recapitalisation.

Along with Luxembourg, Germany is the biggest loser in the arrangement. Germany’s equity ownership in the ECB is 21.44% of its capital.[i] If TARGET2 collapsed, the Bundesbank would lose over a trillion euros owed to it by the others and the ECB itself, and pay up to €387bn of the net losses, based on current imbalances. It would wipe out the Bundesbank’s own balance sheet many times over.

Beyond the ECB’s obligations for unsettled bond purchases, to understand how and why some of the problem arises, we must go back to the earlier European banking crisis following Lehman. From that time non-performing loans began to accumulate at the commercial banks.

If a national banking regulator deems loans to be non-performing, the losses would be a national banking problem. Alternatively, if the regulator deems them to be performing, they are eligible for the national central bank’s refinancing operations — mostly done through repurchase (repo) agreements. A commercial bank using the questionable loans as collateral borrows from the national central bank, which in turn borrows to cover by withholding payments into the TARGET2 system. Insolvent loans are thereby removed from the PIGS’ national banking systems and lost in the euro system.

In Italy’s case, the very high level of non-performing loans (NPLs) peaked at 17.1% in September 2015 but by March this year had been miraculously reduced to 4%.[ii] Given the incentives for the regulator to deflect the non-performing loan problem from the domestic economy into the Eurosystem, it would be a miracle if the reduction in NPLs is entirely genuine. And with all the covid-19 lockdowns, Italian NPLs will be soaring again along with Italian banking exposure to Russia and Ukraine. There’s no sign of this being reflected in national banking statistics, so it must be concealed somewhere.

In the member states with negative TARGET2 balances, such as Italy, there have been long established and growing trends towards liquidity problems for legacy industries, rendering many of them insolvent without the drip feed of additional credit. With the banking regulator incentivised to not admit these recorded and unrecorded NPL problems in the domestic economy, loans to these insolvent companies have been continually rolled over and increased by effectively funding them through TARGET2 and the relevant national central bank. The consequence is that new businesses have been starved of bank credit for lack of balance sheet space. And now, responding to deteriorating economic conditions banks need to contract their lending obligations.

Officially, there is no problem, because the ECB and all the national central bank TARGET2 positions net out to zero, and the mutual accounting between the central banks in the system keeps it that way. To its architects, a systemic failure of TARGET2 was inconceivable. But because some national central banks are now accustomed to using TARGET2 as a source of funding for their own insolvent banking systems, the Ukraine crisis and the rising interest rate environment attributed to producer price and consumer inflation threaten to increase imbalances even further, potentially bringing the euro-settlement system crashing down.

The euro system member with the greatest problem is Germany’s Bundesbank, now owed well over a trillion euros through TARGET2. The risk of losses is set to accelerate rapidly because of repeated rounds of Covid lockdowns in the PIGS and now with the Ukraine situation. Under Jens Weidmann (who has since resigned) the Bundesbank was right to be very concerned.[iii]

This is a direct quote from the highly respected Professor Sinn’s paper on the subject:

“… the Target issue hit political headlines when the new President of the German Bundesbank, Jens Weidmann, voiced his concerns over the Bundesbank’s target claims in a letter to ECB president Mario Draghi. In the letter Weidmann not only demanded higher credit rating criteria for collateral submitted against refinancing loans, but also called for collateralisation of the Bundesbank’s soaring Target claims. Weidmann wrote his Target letter after several months of silence on the part of the Bundesbank, during which it conducted extensive internal analysis of the Target issue. This letter marked a departure by Weidmann from the Bundesbank’s earlier position that Target balances represent irrelevant balances and a normal by-product of money creation in the European currency system.”[iv]

So Weidmann, who has since resigned from the Bundesbank, knew precisely the danger described in this article, wanting better quality collateral standards to prevent the dumping of non-performing loans into the TARGET2 system. There must be a strong suspicion that he was powerless to change things, forcing him to resign on this vital issue. But the problem remains: as a mechanism that permits the PIGS to shelter nonperforming loans in increasing quantities, the TARGET2 setup has become rotten to the core and off the record is known to be. And now, thanks to the economic impact of the coronavirus followed by Ukraine, sooner rather than later the settlement system is set to fail completely.

Until then, TARGET2 is a devil’s pact which is in no one’s interest to break.

The sheer scale of a TARGET2 failure makes a resolution appear impossible. Current imbalances over the whole system total €1.736 trillion. As mentioned above, according to the capital keys, in a systemic failure the Bundesbank’s net TARGET2 assets of €1.160 trillion would be replaced by liabilities up to €387bn, the rest of the losses being spread around the other national banks in the EU.[v] No one knows how it would work out because failure of the settlement system was never contemplated; but many if not all of the national central banks would have to be bailed out, presumably by the ECB as guarantor of the system. But with only €7.66bn of subscribed capital, the ECB’s balance sheet capitalisation is miniscule compared with the losses involved, and its shareholders will themselves be seeking bailouts in turn to bail the ECB. A TARGET2 failure would appear to require the ECB to recapitalise itself and the whole eurozone central banking system.

The ending of TARGET2 is therefore likely to be a complete write-off for the national central banks and will mark the end of the ECB, at least in its current form. And we haven’t even mentioned the immediate impact of rising interest rates, let alone the failure of TARGET2 on the Eurozone’s commercial banks.

Shuffling non-performing loans into central banks is achieved principally through the repo market. Under a repurchase agreement (repo), a bank swaps collateral for cash, a transaction which is reversed later. In this way the central bank ends up with collateral, which has been cleared as “performing” by the local bank regulator, and the commercial bank gets cash and a seemingly clean balance sheet. Any amount of rubbish can be concealed by these means.

The euro repo market is enormous, estimated by the International Capital Markets Association to have been €8.726 trillion outstanding in June 2021. It is far larger than the US dollar equivalent, which at the moment is just over $2 trillion of reverse repos, i.e. the other way with the Fed taking in cash instead of dishing it out. While much of this excess in euro repos is the consequence of negative interest rates, even paying banks to borrow against government bond collateral, it is of such a size as to easily hide bad and doubtful debts within the central bank settlement system.

The ECB has fostered this market, because it creates demand for government debt to be used as colateral, which with minimal and even negative yields would not otherwise be bought. Rising interest rates will collapse this market, withdrawing liquidity from the commercial banks and putting yet more pressure on them to reduce their balance sheets.

It is hard to avoid the conclusion that the ECB must prevent rising interest rates and bond yields at all costs, not only to preserve the euro system itself, but to prevent a collapse of the entire commercial banking network.

Assuming the status of the euro as a medium of currency and credit is to continue, a different and formulaic system of currency management designed to recapitalise the national central banks and keep the currency moderately scarce throughout the Eurozone would have to be implemented. And because its implementation would have to be instantaneous, it would probably prove to be impossible. Therefore, the euro is extremely unlikely to survive its systemic crisis.

The EU’s future following the ECB’s failure

The failure of TARGET2 would require national central banks to address their own relationships with their commercial banking networks properly. It is beyond our scope to see how this might be done in individual jurisdictions, being more interested in the bigger picture and the prospects for the euro and its successors.

Therefore, it is now a when, rather than an if, the TARGET2 system collapses. Foreign G-SIBs appear to have low exposure to the euro system and its commercial banking network, evidenced during the US’s repo crisis in September 2019, when the sale of Deutsche Bank’s primary dealership to BNP was completed. Consequently, the immediate currency effect is likely to be driven by domestic Eurozone entities, rather than foreign liquidation.

Loans denominated in euros will be called in. To the extent that bank customers have deposits and liquid investments in foreign currencies, selling them will inevitably become a source of funds to pay euro obligations, initially driving the euro’s exchange rate higher against other currencies. Furthermore, foreigners who use the euro as the basis of a carry trade, for example to back positions in the fx swap market, will also have their positions unwound, leading to further demand for euros on the foreign exchanges.

Given the extent to which the dollar is currently over-owned by foreigners and while the euro is under-owned internationally, it is the dollar which is likely to suffer most from a eurozone monetary crisis, at least initially. The euro’s fate as a medium of exchange will then be principally in the hands of its users. This will be the background against which Germany’s Bundesbank will be considering its options.

The case for a new mark

A failure of the Eurosystem, which we can now see is becoming inevitable, has also been seen as a danger in some quarters of the Bundesbank, whose staff under Weidmann looked into the reasons for TARGET2 imbalances. Doubtless, the internal arguments over the situation were put on hold by his resignation last year.

This is the logical conclusion from Weidmann’s letter to Mario Draghi at the ECB. It therefore follows that somewhere in the bowls of the Bundesbank there is a Plan B in existance, which at the least will be intended to insulate the Bundesbank from the difficulties faced by other national central banks and the ECB itself in a crisis. This can only be achieved with a new currency, based on the German mark before it was folded into the euro. That way the euro-based Bundesbank can be written off as the Eurosystem collapses, while a mark-based Bundesbank emerges.

Germany will not want to resuscitate old enmities. The Bundesbank will be acutely aware what pursuing its own interests would mean for the PIGS, and also for France whose eurozone ambitions are entirely political. Interest rates in the replacement currencies for these nations would almost certainly rise sharply, collapsing their bond markets insofar as they still exist, undermining any surviving commercial banks, and destroying national finances. These nations would have no practical alternative but to seek the shelter of a better form of money than the euro to re-establish their bond markets, and with a view to having continuing access to credit. In short, the monetary consensus could eventually move from an overtly inflationary monetary system gamed by the national central banks and their regulators to one based on a sounder form of currency and credit.

But instead of debtor nations fully abandoning inflationary habits, their intention is likely to retain the facility of inflationary funding in new clothes. With its new currency, the Bundesbank is therefore likely to resist moves which in effect leaves it in the position of the defunct ECB, taking on responsibility for the circulation of all currency in the former eurozone. Admittedly, the German government, as opposed to the Bundesbank, might view the situation differently, but even it is likely be aware of the political implications of appearing to have escaped a euro crisis relatively unscathed compared with the other nations, and then taking over control of the defunct eurozone’s money. For this reason, the mark is unlikely to be offered up as a replacement for the euro.

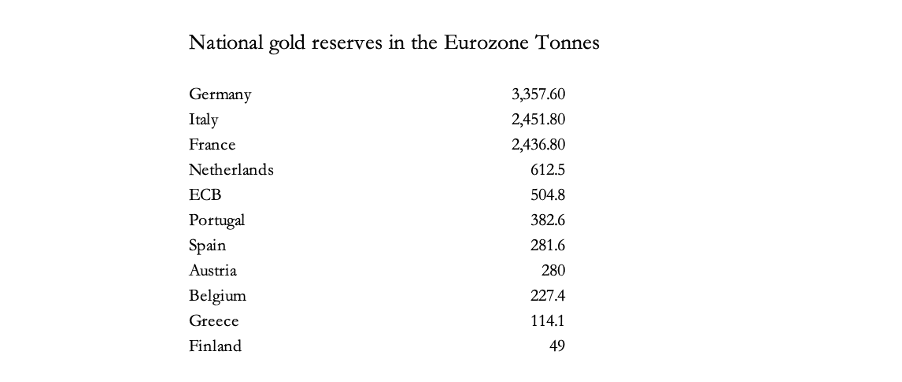

The obvious solution is for German to adopt a credible gold standard, and to encourage other member states to do the same. Figure 2 shows the official gold reserves of key member states.[vi]

The ECB’s gold reserves were originally created by transfers from the national central banks, so we can assume its 504.8 tonnes will be transferred back to them, because other than other EU central banks outside the eurozone they are the ECB’s only creditors.[i] That being the case, the top ten eurozone holders will have over 10,500 tonnes between them. The gold is, however, unevenly distributed, with Germany, Italy and France possessing significant reserves. But Holland and Portugal have ample reserves for their size as well.

While credible gold standards are the best solution, all these nations, including Germany, are likely to be reluctant to mobilise their gold to back new currencies. Germany recovered from two currency collapses in the last century without gold backing, and the Bundesbank is likely to take the view that mere possession of its gold reserves and its historic reputation for sound currency will be enough to convince its citizens that a new mark will be stable and a credible currency. Furthermore, it is not sufficient to turn fiat into gold exchange currencies without addressing government spending. Not only does a successful gold standard require balanced budgets, but a deliberate reduction in overall spending must be maintained for the standard to stick over time. The failure of the Maastricht treaty in this respect illustrates the difficulties of fiscal discipline in the European context.

Politically, it requires a reversal of the European social democratic ideal, risking a political vacuum, threatened to be replaced by various forms of extremism.

International influences

The political and monetary evolution of a post-euro Europe will not be determined solely by endogenous events. There is a similar but less complex crisis evolving in Japan, equally leading to a failing yen mirroring the euro. And both the Fed and the Bank of England are desperately hoping that they won’t be forced to raise interest rates to reflect persistent price inflation. And everywhere that significant financial markets exist, they are under the doleful influence of the bear.

Obviously, the implications of several separate developing crises for each other and the timings involved cannot be predicted beyond guesswork, but there are common threads. The most notable is that the suppression of interest rates and government bond yields by the major central banks has come to an end.

Central banks have maintained their objectives by the inflation of currency and credit, allowing debt creation to balloon and inflate financial asset bubbles. These bubbles have different systemic characteristics. The ECB and Bank of Japan along with a few others imposed negative interest rates while, the Fed and Bank of England have respected the zero bound. With the US economy being more financial in nature and the dollar being the international reserve currency, the dollar’s loss of purchasing power is the primary driver of global commodity and energy prices.

A common linkage between major financial centres is through the G-SIBs. A failure in the eurozone’s banking system will almost certainly undermine that of the US, as well as of the others. History has shown that even a minor bank failure in a distant land can have major consequences worldwide. In this context, it is to be hoped that by exposing the faults in both the TARGET2 system and the eurozone’s commercial banks, a greater understanding of the monetary dangers faced by us all has been achieved. And for citizens in the EU, the regaining of national power from the Brussels bureaucracy is the opportunity for an improvement on the current situation — assuming it is used wisely.

[i] As a shareholder in the ECB the Bank of England might have a claim to some of its gold.

[i] The ECB’s capital keys in the eurozone amount to 69.6176% of the total which includes non-eurosystem EU member states. It was last rebalanced to reflect Brexit. Germany’s is 21.4394% of that total.

[ii] See https://www.ceicdata.com/en/indicator/italy/non-performing-loans-ratio

[iii] See Evergreening in the euro area; Steinkamp, Tornell and Westermann, working paper No. 113 July 2018, which describes how zombie companies are being kept afloat and how their loans end up as Target2 collateral.

[iv] See Hans Werner Sinn’s description of the public debate, when he first pointed out that the liabilities faced by the Bundesbank on TARGET2’s failure were to be decided by its capital key. https://www.hanswernersinn.de/en/controversies/TargetDebate

[v] ibid

[vi] Source: IMF via the world Gold Council.