The sharp decline in US Treasury bond yields anticipates a pivot in Fed policy, which appeared to be justified this week by Chairman Powell’s dovish tone. But in truth, the Fed is not in control of events.

Given that it was US monetary policy which led the way up in interest rates, the dollar was strong against other currencies, creating opportunities for interest rate arbitrage. There is no knowing its scale, but we can expect it to be unwound post-pivot and should not be surprised at continuing dollar weakness. In short, a floor is being put under US price inflation through the exchange rate.

The far greater problem is that the monetary conditions of the 2020s are turning into a repetition of 1970s, but with added vengeance. This article explains the dynamics leading to higher interest rates in the coming years, higher bond yields and the threat of hyperinflation — all evident in the years following the Bretton Woods Agreement suspension.

In 1971, US government debt to GDP was only 34%. Today it is over 120% It is principally in this difference that the catastrophic consequences for the dollar lie, being firmly gripped in a debt trap. Furthermore, with the single exception of Germany, the other G7 nations are similarly ensnared.

These dynamics are not openly discussed in official circles, but by their actions in accumulating as much gold as is available, non-US central banks are fully aware and frightened by the likely consequences.

Introduction

With bond yields having fallen significantly since mid-October, the signs of relief are palpable. Mortgage rates for residential property have eased and lenders are beginning to compete again. Economists are talking increasingly about low growth leading to lower demand for goods, which they expect will lead to official interest rates in a falling trend. Add in the diversion of seasonal cheer, and the problems threatening markets are evaporating.

It appears to be a mystery why the outright recessionary conditions reported anecdotally are not being reflected statistically. We can put that down to a combination of currency debasement goosing the figures before the effect on prices becomes apparent, and the slavish belief in government statistics. But talk to any small or medium size business and you find that business conditions are dire. Where they are highly leveraged, larger multinational businesses are probably too relieved about the improving outlook for borrowing and refinancing costs to worry about immediate trading prospects.

However, the signs from China should not be ignored. Net investment by foreign corporations has become net divestment. Over the last six months, China’s exports have been contracting, only stabilising last month reportedly through widespread discount pricing. While western commentators are busy trashing China, reporting that factories are being shut down in a general crisis for an economy heavily dependent on property and construction, the message from China’s exporters is that we in the west are seeing a slump in demand for imported goods.

The optimists say that this is just more evidence which leads to lower interest rates sooner, so that bonds can be bought and with a falling trend in bond yields, investing in equities is safe as well. The bet here is a Keynesian one, that a recession leads to lower prices and that the stimulation of lower interest rates becomes appropriate. The monetarists buy into the lower interest rate argument as well, claiming that contracting money supply, evident throughout the G7, signals a recession and that the correct response is for central banks to reduce interest rates.

Both Keynesians and monetarists reject Say’s law, which broadly ties production output to consumer demand, and therefore rules out the prospects of a general slump in demand reducing prices across the board. This is because we produce to consume and if we are not producing, we are not consuming. A simplistic argument, maybe, but the truth behind it is impossible to ignore.

Of course, with government subsidies for the unemployed and make-work programmes, there are still earnings in the hands of the unemployed, but that is not the consequence of production but of monetary inflation. This developing recession is set to become stagflationary in character.

This is why optimism in financial circles that consumer price inflation is yesterday’s problem is misplaced. We enter a period of declining economic activity, and the more severe it is the worse the subsequent currency inflation problem becomes as governments crank up the printing presses. But even more alarming, instead of governments starting with balanced budgets creating Keynesian room for credit creation through deficits, we enter an economic downturn with budget deficits and government debt levels already at record levels.

Under these circumstances, interest rates are bound to become driven more by accelerating demand for credit from governments than falling credit demand from productive private sectors. Government bond yields are bound to rise, as foreign investors who make up the marginal investment demand shy away from returns which fail to compensate them for monetary debasement. In other words, this funding will only be achieved by higher, not lower bond yields.

Apart from the Keynesian cycle of economic stimulation, there will also be the consequences of debt traps sprung on the private sector by higher interest rates. Governments will be expected to support an entire commercial banking system facing rising non-performing loans as zombie malinvestments finally stumble into their graves. Over-indebted consumers unable to pay their mortgages, credit card debt, and car loans can be added to the depressing mix.

Entire economies, from governments downwards, have been set on a path to bankruptcy by zero and negative interest rates. As we are repeatedly told, so long as governments have a printing press, they cannot go bankrupt. What they don’t tell us is that ultimately it leads to destruction of their currencies. With the single exception of Germany, the other six G7 nations are entrapped in exponentially rising debt obligations, which with mandated social commitments are impossible politically to control.

Welcome to a world of ubiquitous debt traps.

The US Government’s debt trap

In May this year, the Congressional Budget Office estimated outstanding US Government debt next October to be $27,388 billion. By the end of the first quarter of the fiscal year, it will exceed $34,000 billion. It is soaring out of control, and perhaps it is not surprising that the CBO has not updated its forecasts with this debt uncertainty. The CBO also assumed that debt interest costs last year would be $663 billion, when it ended up being $980 billion 48% higher than forecast. For the current fiscal year, the CBO assumed that the average interest cost on debt held by the public would be only 2.9%. Short-term T-bill financing upon which the Treasury has become overly dependent is almost double that.

Of the total bond debt, some $7.6 trillion has to be refinanced this fiscal year, to which must be added the financing of the budget deficit. Bearing in mind that 2024 is a presidential election year when government spending always increases in an attempt to buy votes, the deficit excluding bond interest is bound to rise from last year’s nearly $1 trillion.[i] And with recessionary forces depressing tax revenue and increasing welfare costs, perhaps we can pencil in an underlying deficit of $1.5 trillion for the current year, to which interest costs must be added.

So far, the US Treasury has not had difficulty in current funding, because at an average rate of over 5.4% since end-September, T-bills have been draining money market funds out of the Fed’s reverse repo facility. At current discount rates, this probably adds about $150 billion to the government’s interest bill compared with fiscal 2023 so far. The balance of funding requirements for the rest of this year should take the total to about $1.5 trillion, 50% of the total deficit, which in turn at $3 trillion is rising at a 50% annual clip.

With GDP this year estimated by the CBO to be $27,266 billion, it gives a budget deficit to GDP ratio of 11%. That is without factoring in an economic downturn. Together with the estimated $7.6 trillion of maturing debt to be rolled into new debt at higher bond yields this fiscal year, we are looking at a further $3 trillion of deficit to fund, totalling $10.6 trillion. This is miles away from the CBO’s debt estimate of $34,205 billion at the end of the fiscal year. After not three months in, debt is already just $300 billion from that total — it looks like the outturn next September will be closer to $37,500 billion.

Debt funding costs will depend on the marginal collective view of foreigners. Other than offshore funds, such as the Cayman Islands, Ireland, Luxembourg and Switzerland, major holders of the coincidental $7.6 trillion in US Government debt such as Japan and China have been net sellers. And of the top twenty holders, seven are arguably categorised as either leaning towards China or threatening to reduce their exposure to US dollar hegemony. On these grounds alone, future foreign participation in US Government funding cannot be guaranteed.

In large measure created by debt funding problems, rising interest rates will make this situation even more difficult. For now, there is easy funding available by issuing treasury bills, attracting money market funds out of reverse repos at the Fed. But this sweet spot is rapidly being exhausted. There is the potential for banks to deleverage their risks by dumping private sector exposure in favour of so-called risk free short-term government stock and that is undoubtedly happening. But that intensifies the shortage of credit for cash-flow starved businesses, leading to higher borrowing costs for the private sector if scarce credit is available. And that surely opens up the possibility that down the line the US Government will be forced to step up costly support for failing businesses.

In the process of relying increasingly on short-term funding, the debt maturity profile shortens, so that the costs of rolling over maturing debt rapidly rises. It’s a situation made worse by growing foreign apathy towards investing in dollars, of which they already own too many.

Some commentators are beginning to see this danger, leading them to believe that if only interest rates can fall, it is an outcome which can be avoided. They believe that the Fed controls interest rates and can bring it about. The Fed also appears to believe it, and we can be reasonably sure that as statistical evidence of recession mounts, it expects to cut interest rates, stop quantitative tightening, and even return to QE. Furthermore, it is a presidential election year and employment will become a more important policy objective than inflation. This policy switch being already apparent, the dollar’s exchange rate will begin to decline materially, and then foreigners will surely increase their selling of US Treasuries.

Foreign holders of dollars, some $33 trillion onshore, a further $85 trillion in foreign exchange derivatives, plus a further $10 trillion in eurobonds cannot be expected to stand idly by and just watch their dollars lose value. Admittedly, similar problems are faced by the other G7 currencies. But if anything, the international community of foreign currency holders are not so exposed to euros, yen, pounds, and loonies. Interest rate arbitrageurs are even short of euros and yen, and their positions would be reversed out if interest rate differentials are expected to decline.

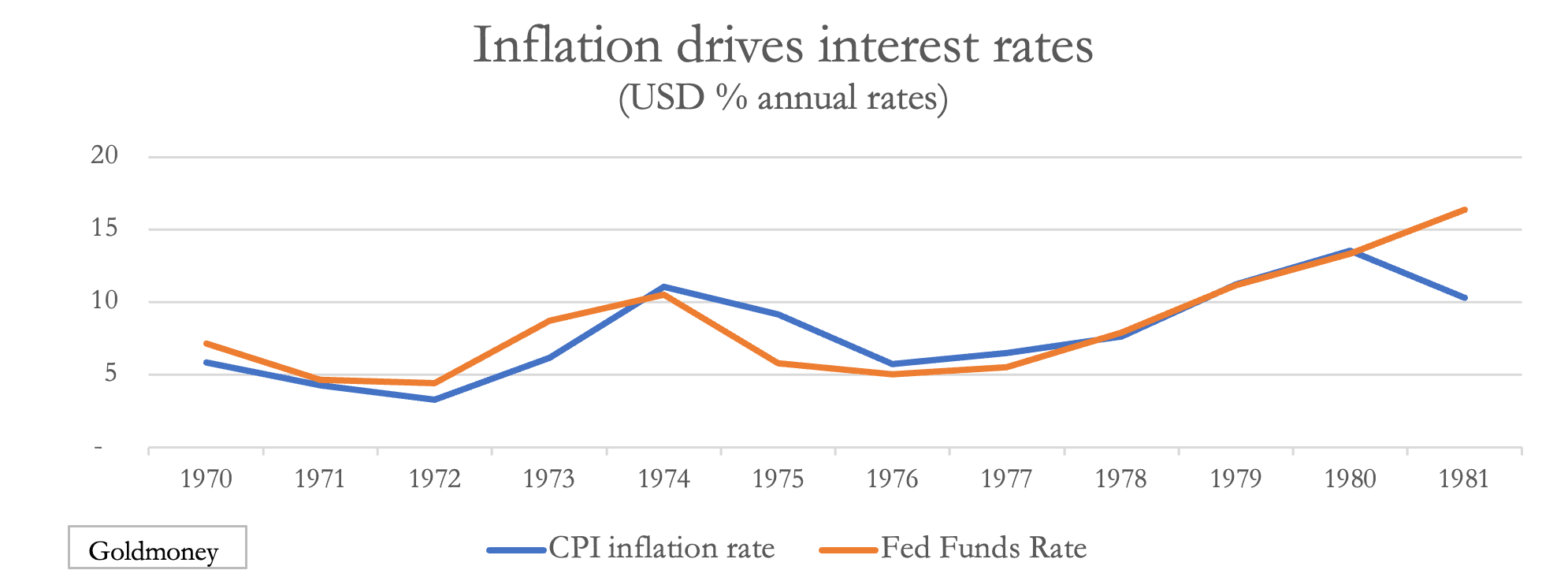

With credit in the form of national currencies and bank lending no longer being attached to gold, monetary theories which evolved during the era of fixed exchange rates are no longer valid. They should be revised for the reality of a fiat currency system. Failure to do so caused major policy failures in the 1970s. As was the situation in the 1970s, it is the rate of consumer price inflation which now correlates with the Fed’s interest rates. If, as seems increasingly likely, foreigners begin liquidating their overweight dollar holdings thereby driving the exchange rate lower in terms of purchasing power, both interest rates and inflation must rise. The tightness of the relationship during the 1970s is shown in the chart below.

Fifty years ago, before the introduction of index linking of benefits and bond yields the CPI’s compilation was reasonably objective with government statisticians independent from outside pressures. That is no longer the case. According to estimates compiled by John Williams at Shadowstats, if the basis of calculation in 1980 had not been subsequently revised, it would reflect an inflation rate closer to 12% than the official 4%.

It should be admitted that there is no correct way of calculating an entirely theoretical concept such as the general level of prices. But there should be no doubt that the average of consumer prices is still rising at a far faster rate than generally admitted. It is perhaps fortunate for the US Treasury that the public doesn’t question official figures. If anything, they are in thrall to them. But this obvious foolery conceals a developing catastrophe.

It was economist Robert Triffin who pointed out that you cannot fool markets all the time. Back in the early 1960s, he pointed out that for the dollar to act as a reserve currency trade policy must ensure that there is an adequate international supply. This meant running a deficit on the balance of trade while retaining a balance of payments, the difference amounting to supply accumulating in foreign hands. He further pointed out that this meant policies must be pursued which were economically destructive in the long run, inevitably leading to a monetary crisis.

In his eponymous dilemma, Triffin proved to be correct when the US and European nations with gold reserves were corralled into establishing the London gold pool to assist in stabilising the dollar-gold exchange rate, a move which failed. The problem persisted, which led to President Nixon suspending the post-war Bretton Woods Agreement in August 1971. Driving that rolling crisis was a surplus of dollars in foreign hands, the realisation that it was debased, and therefore overvalued in terms of real money, which is and always has been gold. It was the crisis predicted by Robert Triffin.

There can be no doubt that the world is on the edge of a similar event today. The figures quoted above, amounting to over $125 trillion dollars and derivative commitments in foreign hands is nearly four and a half times US GDP. The Triffin crisis is set to become a self-fulfilling prophecy again, potentially on a far greater scale than the failure over fifty years ago. All it needs is a loss of faith by foreign holders of dollars in the US Government’s finances and its self-serving statistical manipulation.

The comforting fallacy of GDP

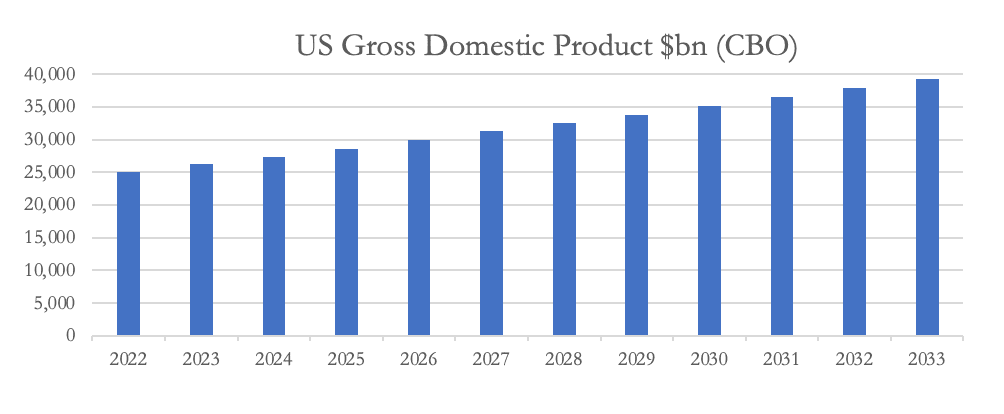

So far, we have not yet explained why the GDP statistic fails to reflect anecdotal evidence of underlying trading conditions. The next chart is of the CBO’s current (outdated) forecast for nominal GDP, forecasting a steady rise over time in defiance of changes in underlying economic conditions.

It should be noted that the continuing expansion of GDP doesn’t reflect economic activity, but the deployment of two sources of credit into qualifying activities: that of commercial banks lending to businesses and consumers, and of excess government spending over revenue raised. Taking figures simplistically, we can see that in the current fiscal year to end-September there will be a direct injection of $1.5 trillion by government spending over revenue into the economy, nearly all of which by being spent on welfare and non-financial activities raises nominal GDP accordingly. We can add to that a more slowly trickling element into GDP originating from interest costs, all of which initially goes into financial services excluded from GDP. Some of it becomes spent into GDP over time.

GDP is slated to rise by $1,028 billion in the current fiscal year, so adjusted for the government’s non-productive injection of credit, private sector nominal GDP is already declining.

The non-distinction between wasteful government spending and the productive private sector is an illustration of the error of thinking that growth (in other words a rising GDP) represents an improving economy. An increase in GDP merely reflects the deployment of extra credit and says nothing about how that credit is used. Economists with their models merely assume that growth in GDP represents economic progress. But any government, whose contribution to GDP is ranked exactly the same as that of private sector actors, is a burden on progress because it diverts resources from demanded production. Therefore, the more government there is, the more hampered an economy becomes.

In addition to the fallacy of the US Government’s contribution to GDP, the deployment of capital resources within the private sector has become corrupted by the prevention of Schumpeter’s concept of creative destruction. Bad and inefficient businesses which should have ceased trading have been kept going by a mixture of the fruits of government lobbying and the availability of ultra-cheap credit. Borrowing has also been undertaken for non-productive purposes, such as financial engineering.

The build-up of malinvestments which in a free market would have been rapidly liquidated and the capital redeployed more productively has become an enormous blight, undermining economic potential. The rapid rise in interest rates from the zero bound has exposed the fallacy of operational leverage for even stable utility-like earners, whose modest returns are only multiplied by ultra-low interest costs until refinancing becomes due.

These malinvestments are a ticking timebomb for socialising governments which are always inclined to continually subsidise inefficient industries for fear of rising unemployment. Unemployment itself becomes harder to resolve, because subsidising unemployment through welfare payments tends to make the redeployment of labour resources sticky. Employment taxes are an additional cost, and HR regulations have made employment both less productive and woke. And having encouraged commercial banks to increase their operational leverage with zero interest rates, it doesn’t take much in the way of bankruptcies in industry to create a banking crisis. Whether industries, or banks, or both are supported through the developing economic downturn, the US Government will have additional and unexpected financial commitments ahead. Monetary inflation is therefore set to accelerate beyond anyone’s estimation as the recession develops, and that is bound to undermine faith in the currency. Consequently, the outlook as the recession deepens is for rising, not falling interest rates.

The consequences for prices

Having bought into Keynes’s dismissal of Say’s Law, mainstream economists and commentators think that a recession leads to lower prices. But that is without reckoning on lower production, because normally production layoffs increase ahead of falling consumption. But the division of labour which links the general level of output with consumer demand is corrupted by government welfare payments. And consumer borrowing to finance consumption is a further element supporting demand as production output declines.

The general level of consumer prices would be somewhat higher if the offshoring of production to cheaper manufacturing facilities over the last forty years had not occurred. A combination of readily available inexpensive labour and extensive automation of production in Southeast Asia and China has had a substantial and beneficial impact on production costs, reducing consumer prices in the G7 nations below where they would otherwise be. Without this benefit, the current rise in the general level of consumer prices would be significantly higher.

This should be borne in mind, when in a presidential election year China-bashing and Make America Great Again memes will intensify the trend for industrial disinvestment from China and Southeast Asia. Unwinding the diverse supply chains built up over the last forty years comes at a considerable cost. At an economic forum in Columbia recently, the deputy managing director of the IMF, Gita Gopinath warned:

“Fault lines are emerging as geoeconomic fragmentation is increasingly a reality. If fragmentation deepens, we could find ourselves in a new Cold War. The economic cost of Cold War II could be large. The world has become much more integrated, and we face an unprecedented breadth of common challenges that a fragmented world cannot tackle.”

She also urged countries to protect free trade and warned that growing global tensions could threaten food security. And she estimated that losses in global trade could amount to between 2.5%—7%, pointing out that about 3,000 additional trade restrictions were imposed globally in 2022.

Presumably the presidential candidates in America will disregard Gopinath’s warning, preferring to tackle the trade deficit problem by way of inflationary subsidies and tax credits for US production, and imposing yet more trade barriers. President Biden is already going down this route with his inappropriately named Inflation Reduction Act. If there was any merit in this approach the supply of dollar credit into foreign hands would slow for the currency’s benefit, but that is no more than wishful thinking.

Economic theory posits that all else being equal the budget deficit must be covered by an increase of consumers’ savings in excess of capital investment, otherwise a deficit on the balance of trade will be the result. And if the level of net savings remains unchanged, the budget deficit should approximate to the trade deficit. Whether it is created by the banks or the central bank, an excess of credit not covered by increased consumer savings is inflationary, and with bank credit not expanding the major source of this inflationary credit is the budget deficit.

The supply gap created by excess credit injected into the economy as the consequence of a budget deficit can be covered either by higher unit prices or increased imports. Domestic businesses can respond to price pressures by investing in extra output capacity, to reduce unit costs. Importation of raw materials, machinery, and semi-manufactured items is why capital investment becomes a necessary component in the twin deficit calculation.

With diversified supply chains, over recent decades capital investment has bolstered production abroad, rather than domestically. This has reduced cost pressures on production, indicating that a rising trade deficit provides an important relief valve for inflationary pressures. That is assuming a stable currency exchange rate, which has uniquely benefited the dollar because of its reserve status and demand for it for funding and settling expanding international trade.

Taken at face value and given that American citizens are unlikely to increase their savings in the current difficult economic climate, the trade deficit for the current fiscal year is set to increase in line with the budget deficit. Corrected for the creative accounting over student loan forgiveness, which was rejected by the Supreme Court, the budget deficit for the last fiscal year was about $2 trillion, of which 48% was debt interest. In the current fiscal year, the run up to a presidential election is bound to see a greater emphasis on deficit spending. And with the US economy stagnating or worse, a spending deficit rising to over $1.5 trillion is likely with debt interest additionally taking the total to about $3 trillion.

The twin deficit hypothesis suggests that the deficit on the balance of trade will trend towards a similar figure to the budget deficit. But that might not happen due to official attempts to interpose trade barriers. Consequently, restrictions on the supply of goods from abroad will lead to domestic substitution replacing cheaper imported consumer goods. To the extent that production is repatriated, consumer prices will tend to rise, making it impossible for the Fed to reduce interest rates over the coming years.

Other G7 debt traps

According to the IMF, G7 members’ government debt to GDP ratios are 121% for the US, 107% for Canada, 98% for the UK, 261% for Japan, 112% for France, 144% for Italy, and 65% for Germany. Germany is the only G7 member not directly exposed to a debt trap.

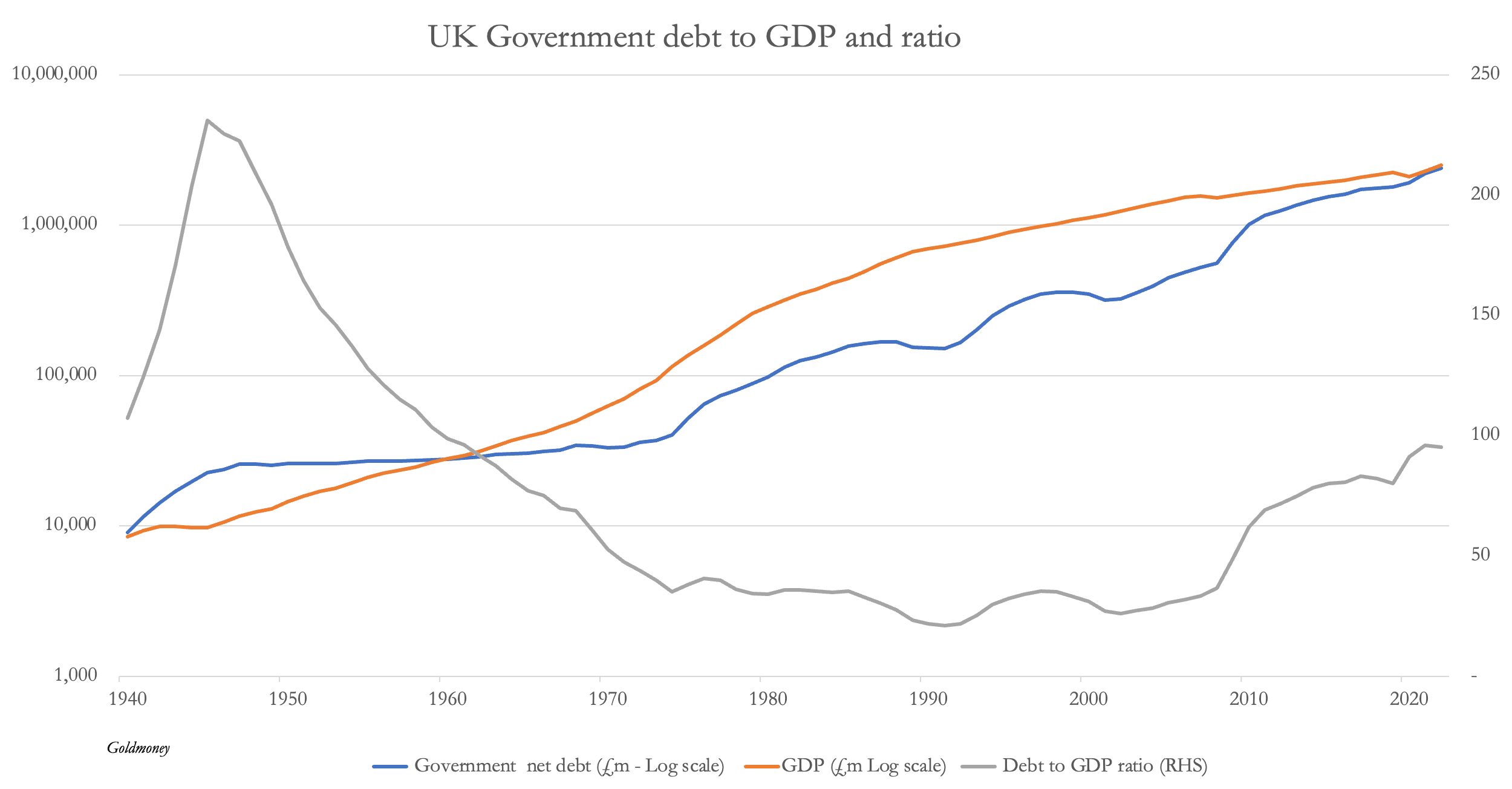

In the past, high debt to GDP ratios have been reduced by ensuring that government debt grows at a slower pace than GDP, outright cuts in borrowing proving impossible to implement in practice. The following chart illustrates how the UK managed to reduce her debt to GDP ratio following the Second World War despite increasing debt levels.[ii]

From its peak at 231% of GDP, GDP grew faster than government debt and the ratio fell to 22% in 1992. From then on, debt began to grow faster than GDP, which is why by 2022 it rose to 98%. The conditions, included interest rate and bond yield moderation, reflected the Bretton Woods Agreement gold standard until 1971, by which time the ratio had fallen to 44%. It should be noted that the expansion of credit before the seventies, which fuelled the increase in GDP, was not much reflected in rising consumer prices, which were restricted by the global Bretton Woods Agreement.

Though interest rates rose strongly twice in the 1970s, nominal GDP also rose strongly, reflecting significant increases in inflation rates, peaking at over 20% at one point. In effect, the debt to GDP problem was inflated away.

Without fiscal control suppressing the growth of government debt below the growth of GDP, the debt to GDP ratio will increase. But with the private sector stagnating in all G7 jurisdictions and only unproductive government spending increasing, today’s currencies will be debased. Absent strict budget spending discipline, the purchasing powers of all G7 currencies are declining and the rate at which they will continue to do so is set to accelerate in the next year or two because the required spending discipline is politically impossible. We can therefore conclude that expectations that the inflation problem will diminish are misplaced. At the least, we face a period similar to the 1970s with the added problem of government deficits already out of control and debt to GDP ratios already high.

In the mid-seventies, the UK government was forced to issue three tranches of gilts with coupons at 15% and over. At that time, the UK’s debt to GDP ratio was only 38%, and with an emergency loan from the IMF which also enforced the necessary fiscal discipline, Britain got through it. With debt to GDP ratios three times higher for the US currently, this year’s fiscal deficit is likely to exceed 12%, and with no outside disciplinarian such as the IMF, the outlook for dollar interest rates is, to put it mildly, terrifying.

Conclusion

This article argues that the current decline in price inflation is temporary, and that interest rates will rise significantly in the coming years. The conditions which led to the IMF having to rescue Britain from insolvency in the mid-1970s are being repeated in the US today, along with the other G7 nations. Germany’s relative fiscal rectitude is negated by the debt traps on other euro area G7 nations.

Like the British experience five decades ago, today’s economic establishment is blindsided. Additionally, the debt trap problem centres on the US dollar, partly due to her high debt to GDP ratio and partly due to unprecedented levels of foreign ownership of dollar credit and financial investments.

This article has explained why along with the other G7 members the US Government is in a debt trap, which can only end in a dollar crisis. It might have even begun this week, with the Fed pivoting from its attempts to limit inflation to rescuing the economy from recession. Inevitably, a declining dollar is going to lead to its purchasing power declining and encourage foreign liquidation of the currency. Against this background, the funding problem for soaring budget deficits can only be resolved through higher interest rates and bond yields.

When interest rates and bond yields inevitably begin to rise again, the value of financial assets in foreign ownership will fall. The prospect of losses is sure to accelerate liquidation of foreign owned dollars and assets. And where the dollar goes, eventually all other fiat currencies will follow.

It is no exaggeration to say that we are almost certainly seeing the beginning of the end of the era of pure fiat currencies, bookended by the 1970s and 2020s. Though they won’t say so in public, central bankers also see it as a growing possibility, which is why they are accumulating physical gold as rapidly as possible.

[i] The actual outturn for 2023’s deficit was recorded at $1.7 trillion. But this was after a credit for $300bn for student loan repayments which were disallowed by the Supreme Court.

[ii] Data from the Bank of England: A millennium of macroeconomic data for the