By Dr Frank Shostak

Most economic commentators consider a weakening in economic statistics such as gross domestic product (GDP) as indicative of a weakening in the economy. According to most experts this decline in the GDP, which is labeled a recession, as a rule arises because of a decline in the overall demand for goods and services. This is seen as predominantly because of a decline in the private sector’s buying of goods and services.

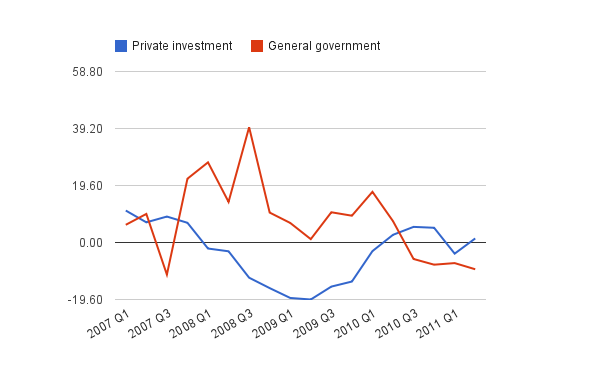

Consequently, it is recommended that the central bank should step in and strengthen the private sector’s demand. This it is held, is going to pull the economy out of the slump. The means recommended by experts to revive the economy are the lowering of the interest rates and raising the growth rate of money supply.

Most goods that individuals require to support their life and well-being are not readily available. These goods have to be produced by transforming various things in nature into goods that individuals can use. The transformation of things has to undergo various stages.

In an economy, which operates in the framework of the division of labor some individuals are employed in the extraction of various raw materials such as coal and iron. Some other individuals are employed in the conversion of raw materials into various tools and machinery. Whilst some other individuals are employed in the transformation by means of tools and machinery of various things that are available in nature into consumer goods.

Note that individuals employed in the various stages of production must have access to consumer goods in order to support their life and well-being. The access to consumer goods becomes possible because of savings, which are the amount of consumer goods produced in excess of the consumption of these goods.

For instance, if a baker produces ten loaves of bread and consumes two loaves his savings are eight loaves of bread. In order to enhance his oven, the baker hires the services of a technician. The baker pays the technician with the saved bread. The saved bread enables the technician to maintain his life and wellbeing whilst he is busy improving the oven. With an improved oven, the baker could increase the production of bread.

Likewise, the other producers of consumer goods by exchanging these goods for the products and services of various producers, supply them with the means that support their life and wellbeing.

Note that the saved consumer goods support individuals in all the stages of production. From the producers of consumer goods to the producers of raw materials and the producers of tools and machinery. The saved consumer goods are the subsistence fund that sustains individuals in the various stages of the production structure.

Observe that if the production of consumer goods were to increase all other things being equal, this would permit the increase in savings and hence the increase in the subsistence fund. This in turn would permit the expansion of the infrastructure and the increase in the economic growth.

Again, capital goods are not readily available, in order to make these goods it is necessary to allocate consumer goods to sustain individuals that are going to be employed in the production of tools and machinery. The allocation of consumer goods is what savings is all about.

Also note that the allocation of consumer goods is done by the producers of final consumer goods. Hence, it is the producers of final consumer goods that save and therefore the key for economic growth. If the producers of final consumer goods were to decide to increase their consumption, then this would reduce savings and reduce the economic growth. Thus, if a baker that produces ten loaves of bread decides to consume five loaves rather than two his savings are going to be five loaves of bread rather than eight loaves, all other things being equal. This is going to force the baker to acquire a fewer hours of technician services thereby reducing the production of bread versus the case when his savings is eight loaves of bread.

Defining what recession is

We suggest that the subject matter of recession is not a weakening of GDP and various other economic indicators as such but the liquidation of various nonproductive activities that have emerged on the back of the easy monetary policies of the central bank. We label these activities bubbles.

When the central bank relaxes its monetary stance, this lays the foundation for the exchanges of nothing for something, which amounts to a diversion of savings from wealth generating activities to non-wealth generating activities. This undermines the wealth generation process.

Note that once the central bank’s pace of the monetary expansion has strengthened, the pace of the savings diversion is also going to strengthen. Conversely, once the central bank has tightened its monetary stance, this slows down the savings diversion.

Activities that sprang-up on the back of the previous easy monetary policies are now getting fewer support as a result of a tighter monetary stance. These activities fall into trouble – an economic bust, or a recession emerges.

Regardless of how big and strong an economy is, a tighter monetary stance is going to undermine bubble activities that sprang-up on the back of the previous expansionary monetary policies.

It follows then that recessions or economic busts are not about the strength of an economy as such. It is about the liquidation of activities that emerged on the back of the previous easy monetary policies of the central bank. The recessionary process is set in motion once the central bank reverses its easy stance.

Now, recessions are good news for wealth generators. A tighter monetary stance slows the diversion of savings from them towards bubble activities. This in turn strengthens the wealth generation process.

By most commentators as long as the growth rate of consumers’ expenditure is on the increase there is no risk of a recession ahead. This means that as long as there is a growing demand by consumers, good times are going to follow the growing demand.

We suggest that demand cannot be independent, it is restricted by the previous production. The only way to raise the ability to consume more is to raise the ability to produce more.

On this James Mill held,

But if a nation’s power of purchasing is exactly measured by its annual produce, as it undoubtedly is; the more you increase the annual produce, the more by that very act you extend the national market, the power of purchasing and the actual purchases of the nation…. The demand of a nation is exactly its power of purchasing. But what is its power of purchasing? The extent undoubtedly of its annual produce.

Once more, what limits the production growth of goods is the availability of tools and machinery i.e., capital goods, which makes workers more productive.

GDP and money supply

The key variable that most commentators are paying attention to is the gross domestic product (GDP). Given that this indicator is monetary turnover, then obviously changes in the money supply are followed by changes in the GDP. We suggest that policies that are aiming at preventing the emergence of a recession make things much worse. These policies not only provide support to existing bubble activities but allow the emergence of new bubbles thereby undermining the wealth generating process further.

As long as wealth producers can generate an adequate amount of savings to support productive and bubble activities, the easy monetary policies of the central bank, which strengthens the GDP (the monetary turnover), is regarded by most experts as a success.

Once the ability of wealth generators to support the overall economic activity weakens, the economy is starting to slide into a recessionary hole. No central bank easy monetary policy can reverse this slide – on the contrary it is going to deepen the economic slump. Note again, that the easy monetary stance undermines the savings formation process thereby weakening the wealth generator’s ability to support the production of goods.

Conclusion

We suggest that recession is about the liquidation of activities that emerged on the back of the previous easy monetary policies of the central bank. The recessionary process is set in motion once the central bank reverses its easy stance. What matters for economic strength is not strong economic data but freedom from the central bank policies of tampering with markets.