This time last year, while still bullish out of regard for the effects of the Fed’s latest burst of monetary pharmacology, we had begun to warn that the latter part of 2011 was unlikely to be anywhere near as benign for either market participants or those struggling, far beyond the Bloomberg screens and VaR reports, to make a living in the real world of industry and commerce.

As regular readers will no doubt recall, ever since the cracks started appearing in the last Boom, our guiding theme has been that policy would be driven by a convergence of political expediency, faulty economic reasoning, and a misapprehension of the historical record. This, we said, would inevitably preclude the application of any swift and effective remedy for our ills in favour of a long, drawn-out programme of partial fixes, inappropriate treatments, and mounting shots of stimulus, each more short-lived than the last in its effect on growth and employment; each more rapidly dissolving into an unedifying chorus of complaint as the malign side effects of the inflation affected already-pressured household budgets. As we put it some years back, the imperative to avoid the disaster of 1931-3 would first get us into a mess from which the equally ardent desire not to replicate the ‘mistakes’ of 1937 would make it almost impossible to extract ourselves.

And so it is today, where – almost five years after the first warning tremblors began to shake our debt-mortared Tower of Babel – we are still beset with calls for yet more government borrowing, yet more central bank activism, the better to suppress the natural healing process of thrift in favour of a ruinous policy of enforced speculation and capital exhaustion.

Twelve months ago, it was clear that those emerging market nations whose financial architecture was not too obviously endangered by our Occidental folly, whose fiscal burdens were far less crushing than ours, and whose current accounts were typically in a comfortable surplus – and hence whose reliance on the forbearance of external creditors was minimal – had already pushed the envelope too far. Yes, they had been the engines of growth going into the crisis; yes, their initial, trade-driven slump had been swiftly surmounted on a wave of easy money and state-directed spending; yes, the impetus was such as to power them on to new highs of output and resource use, but the boost had not surprisingly served to raise the cost of living to the point where social unrest was threatened.

Thus, from a programme of full-bore pump-priming, the pendulum had swung toward restraint in China, in Brazil, in India and several other key contributors to global growth. As a result, real M1 (our preferred indicator) went from an incredible 37.5% yoy in China (five full sigmas over the 1996-2009 mean) to barely 2.8% (2.5 sigmas below it) in the space of 20 months. For Brazil, the story was similar: from 15.3% ( 0.8 sigmas over the 14-year, post-hyperinflation mean) to minus 6% (1.8 sigmas under it) in a year. India, too, saw a heavy-footed switch from the gas to the brake, as a 12.6% increase (1 sigma over a 25-year, stationary mean) gave way to an 8% decrease (almost 3 sigmas below it).

Making the transition even more painful in the first of these, was the inevitable bifurcation by which the brunt of the impact was felt by those arguably more entrepreneurial, smaller scale businesses who have to strive to maintain themselves in their niche, largely absent the cosseting of cheap finance and subsidised inputs which their larger, more predatory, State-Owned competitors routinely enjoy.

Nor was the situation eased by the fact that so much credit was being made available – both within and without the putative regulatory framework. As a consequence it appeared much more simple to turn a fast buck by grabbing what funding one could (especially when borrowed via a fake commodity purchase in what appeared to be a perennially depreciating dollar) in order to participate in the ballooning real estate mania, than it did to face the hard grind of safeguarding revenues and preserving profitability in a world of dubious export prospects, laggardly internal demand, and steeply rising costs.

Compounding all this was the great externality which arose firstly from the so-called ‘Arab Spring’, then from the summer’s sponsored insurgence against the Libyan regime, and lastly from the threatened Iranian (nuclear) Winter – namely, the persistently elevated price of oil which, for, say the Germans, has spent the last twelve months at a real level higher than that endured at the peak of the second oil shock and also 12% above 2008’s worst, like-period reading. The estimable Jim Walker of Asianomics refers to this as the GCT – the Global Consumption Tax – a jump in the price of a vital input which therefore constitutes at least a short-term drain on discretionary spending (and, of course, on capital formation) in all those not lucky enough to be wallowing in petrodollars or able easily to borrow them back in these times of straitened credit, in order to make up the budgetary shortfall.

Meanwhile, in Europe, the Pelion upon Ossa of adding the Keynesian burden of counter-cyclical profligacy to the chronic, boomtime self-indulgence of the all bar a few member states finally revealed the hopelessness of what we have previously characterised as the vacuous circle of ailing banks being propped up by overstretched governments who must then borrow the very same rescue funds back from the banks whose future they were supposedly securing.

As the money markets froze and the doors of the foreign exchange market almost clanged shut in their faces, such banks were no longer able to contribute to the sustenance of a rate of real money expansion which had hit what was at least a 30-year high (12.6% yoy; +2.1 sigmas) in the triumphal autumn of 2009 when this newest of New Deals was seemingly proving its worth in forestalling a slip into a slough of prolonged economic despond.

Alas! Since then, it has been a descent from surfeit into dearth. With nominal growth scarcely positive for much of last year – and with prices rising as a consequence of the earlier, near-universal laxity of fiscal and monetary settings around the globe – the score for the past few quarters has been in the negative column (-2%-plus; -1.6 sigmas) and the hopes of escaping with only a light penance in absolution of the sins of the Noughties have crumbled, turning much of the Continent into drear shadowland filled with weeping and wailing and gnashing of teeth.

At the height of the sugar-rush asset markets of last Spring, it was widely assumed that risks would be minimal. Not only did the Herd presume that the Fed stood ready to relight the blue touchpaper the minute the US economy sputtered, but the all-seeing Chinese mandarins were well on the way to engineering that most fabulous of economic happenings, the Soft Landing, too. Greece was meanwhile NOT going to trigger any CDS-inspired chaos and, besides, Portugal had just been approved for its bailout and the EU commissariat had proposed an expansion of the EFSF’s capabilities to no less than €440 billion (albeit over the dead bodies of certain Finnish and Slovak politicians, not to mention the impending professional hara-kiri of one or two Bundesbankers).

Sad to relate, this was just about the point when the metaphorical rats which carried the latter-day Black Death to sovereign Europe repeated the course of their historical antecedents and jumped the Aegean-hailing ship to swim ashore at Genoa. As Italy’s finances came under closer scrutiny, all manner of chaos was unleashed – euro-dollar basis swaps plunged to negative triple figures; OIS-Libor and vanilla swap spreads began to climb; risk reversals plummeted; the floor fell out from beneath the equity market, and the euro itself spun out to an 8-year low.

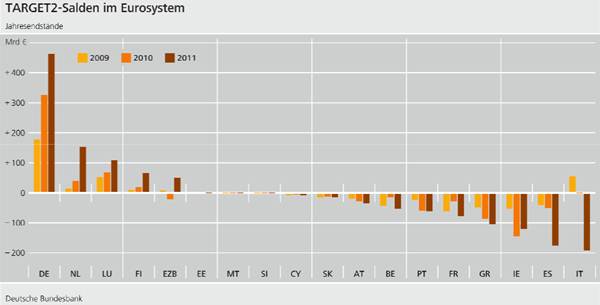

Meanwhile, the intra-Eurozone TARGET2 balances which record transfers being conducted between the system’s national central banks – who, by extension, are thus acting to provide an intermediating ‘credit wrap’ between those commercial banks of net surplus and net deficit countries who will no longer deal with each other directly – began to soar, with Germany and the Netherlands seeing their combined net creditor position mount €260 billion in the second half of 2011, while Spain and Italy’s combined net debt increased by €310 billion.

In Asia, meanwhile, the PBOC stuck to its guns, forcing banks to consolidate many of their ‘shadow’, reg-arb loans back on to their balance sheets where they would become subject to all of a heightened reserve requirement, a stricter enforcement of loan:deposit ratio ceilings, and to capital adequacy provisions. Backed up with other, bureaucratic restrictions imposed on the property market – as well as a severe cutback in other forms of infrastructure spending, such as that undertaken by the heavily-indebted and widely-criticised Railway Ministry, the China bears were soon having what looked like a well-deserved field day, as trade flows and industrial output around the entire global boiler-room began to slacken.

The stock market, for one, reacted by shedding a third of its value to home in on three-year lows and to stand briefly no higher than it did way back in early 2007 – another harsh reminder that the generation of even the most impressive series of GDP reports says little or nothing about returns on capital, much less the level of the equity prices which supposedly reflect them.

We are on record as being highly sceptical of the Chinese ‘miracle’ – how could an Austrian not look askance at this highly corrupted, semi-command economy, with its dysfunctional markets for goods, resources, capital, and currency? But we are also realistic – or resigned – enough to understand that ‘there is a lot of ruin in a country’ and to warn our fellow pessimists that, at least while the capital account remains largely closed off, China has a great deal of room to move losses from one balance sheet to another, and to seek out new media through which to direct the wealth and energy of its people in the wasteful pursuit of gigantism and in the false worship of the Keynesian cargo-cult of consumption at any price.

Given the vast sums at stake, it could even be that China moves to avert a nasty, decidedly non-linear episode in the wake of its imploding property bubble by seeking to reinflate that same excess directly. However, in light of the decidedly adverse political calculus associated with such a move – not to mention the perilous reinforcement of moral hazard it would entail – we would rather bet on them finding some other vehicle through which to enact any coming ‘stimulus’ – a windmill for every household, a horizontal gas rig for every acre of scrubland, and a domestic appliance voucher boondoggle for every SOE, perhaps.

Here again, the room for reversal is greater than it was last year when the land resounded to the anger of those who felt cheated by the system and who chafed at the ubiquitous evidence of Party-generated self-enrichment and privilege, an inequity whose contrast was even more strongly drawn by the experience of their own dwindling standards of living. The subsequent easing of price pressures has given the authorities a certain leeway within which to tack, when they so require – and that sea-room may be even more enlarged if the economic correction takes on a momentum of its own, as we suspect it yet might. Moreover, if the next wave of handouts takes the form of personal tax breaks, greater welfare spending, a higher SOE payroll outlay, and a programme of subsidies aimed at individuals and not at the behemoth producers, as before, public outrage may be sufficiently mollified to ensure a relatively calm hand over of power, later in the year.

Easing, then, may not be as promiscuous nor as swiftly undertaken as the Bulls might wish, nor will the interregnum between the new bubble and the old be entirely without drama for China and her satellites, but we doubt the ruling elite is yet ready to relinquish the Mandate of Heaven and the forced expansion which they deem essential to its maintenance.

Though far from clairvoyant last year, our analysis turned out largely for the best, not least in our estimation that while the notorious ‘Bernanke Put’ had not been cancelled, it did lie a great deal further out of the money than the Pollyannas had been expecting. Under assault from both left and right – pincered between the ‘Occupy’ movement and the Tea Party – the Fed could no longer fend off criticism that it was only enriching the plutocratic Few at the expense of the make-ends-meet masses of plumbers and plasterers.

Having dissipated a good deal of its credibility through its laughable attempts to pretend that it had had nothing to do with the rising price of everyday goods and services – or, conversely, that rising energy prices constituted a veritable economic boon by dint of their role in reducing real interest rates – it was then left thoroughly red-faced when the NY Fed’s latest in a long line of well-heeled, reverse-amakudari, William Dudley, tried to defend the institution’s record with a failed attempt at emulating Marie Antoinette, only to be told dismissively that no-one can eat an iPad, no matter how hedonically cheapened it might have become at the hands of the BLS statistical manipulators.

Thus, though he has long been itching to do more, the Fed Chairman has spent much of the past six months hemmed in by opposition emanating from both within and without his committee rooms, to the point where all he could do in the interim was pledge to keep near-zero rates for some unconscionable time hence while messing about with the maturity of his vast portfolio of securities in the hope of shaving a few extra basis points off the long end.

Ironically, however, his own forced inaction seems to have coincided with the first signs for some good while of a monetary inflation not being fuelled by the central bank itself. After a brief pause in the late summer, the past few months have seen a marked reacceleration of the aggregates in the US. This has come about to the accompaniment of a partial utilisation of some of that mountain of excess reserves of which the banks dispose with the result that there has been a more ready extension of credit to business and a greater take up of its paper, as well as of that of the GSEs. Domestic banks in America – if not, understandably their foreign-domiciled competitors – seem to have been doing Blackhawk Ben’s work for him in recent months, even as Corporate America has been restocking and taking a last-minute advantage of the tax breaks temporarily afforded to those making below-the-line outlays on plant and equipment.

However we look at this, with CPI no longer rising steeply, these past few months, and with the YOY comparison about to made with a quarter which saw the third fastest burst in a decade, our noble Chairman – and his packed council of Ueber-doves – will have a good deal more room for manoeuvre should the economy stutter this time, especially since he has been careful to trail the idea that any prospective easing would be aimed at relieving the sufferings of those still trapped in a moribund residential property market on Main Street rather than those fretting on a bonus on Wall Street. Nor would the present occupant of 1600 Pennsylvania Avenue be likely to raise too many objections were an injection made around the vernal equinox come to produce the maximum feelgood factor by the time the autumnal one arrived.

All this leads us to believe that though the US economy is arguably the one least in need of any further monetary amphetamine at present, its central bank stands far more ready, willing, and – critically – able to provide one than at any time since the Fall of 2010. Phrased another way, the ‘Bernanke Put’ whose activation proved so disappointingly absent during last year’s retreat, may lie a good deal closer to the money now than it did when things turned sour last year.

In Europe, too, there is a sense that headline fatigue has set in – that the only sort of surprise from Greece that has not long since been discounted is a good one. Thus, on the somewhat incautious proviso that no new outbreak of financial Ebola occurs, the market may persist awhile in its willingness to sieve through a still-growing, mountainous ore of despair, in search of the few gleaming nuggets of hope it contains.

Moreover, there is some chance that the scale of the last LTRO – coupled with the alleviation afforded by the Fed’s $100 billion-odd of dollar swaps – was finally sufficient to overcome the attrition felt earlier in the year when many of the ECB’s actions were simply substitutional – i.e., when its intercession via TARGET, its government bond purchases, and its repo finance were more about sticking fingers in the leaking dyke of interbank credit than they were about channelling a new flood of employable liquidity between the levees.

We will not know for sure until we see the data for January, but the fact that most of the stress indicators we mentioned above have backed off appreciably (and have not yet, as we write, been too aggravated by the renewed focus on Portugal), together with the fact that European yield curves have undergone a bullish steepening, certainly points in that direction.

Moreover, one suspects that the seeming apotheosis of Hausfrau Merkel’s starkly uncomplicated version of haute finance might just turn out to be a Pyrrhic victory as far as the continent’s fast-dwindling band of hard money men is concerned in that the immediate and tangible inflationary quid for the delayed and highly-contingent pro quo of budgetary rectitude might well be a successfully renewed push for more overt ECB involvement as a monetary counterweight to the theoretical fiscal austerity to come. What our German friends hope one day to gain on the swings may well turn out to have long since been lost on the intervening swirl of the roundabout.

The last few days of February will be critical to this assessment, since we will then receive the first hard evidence of just what it was that the first massive LTRO actually achieved, with this clarification arriving not too far in advance of the implementation of a follow-up operation already subject to a good deal of hyperbole about exactly how gargantuan in scale it might be turn out to be.

The upshot of all this is that we stand uneasily at something of a watershed: the economic data seem to be worsening everywhere bar the US as an inescapable consequence of the lesser degree of monetary ease which has prevailed of late in most of the major centres, but, despite this, we are all trying to whistle bravely past this particular graveyard of deterioration in the hope of the inflationary resurrection we believe will shortly come.

For now, the same people who were shaken rudely out of the bullish complacency of the front half of 2011 and into the stomach-churning round of long liquidation of the back half seem eager to be back in the game. After all, it is doubly hard to justify being on the sidelines when markets rally and when the returns to either prudence or pusillanimity (depending upon your vantage point) are zero nominal, negative real.

Not only are equity and bond markets responding to this stirring, with more participants being pulled in on each tick higher, but commodities, too, are rising despite the arrival of the annual purdah of fundamental news associated with the Lunar New Year. New positions are being built in metals; stale, largely geopolitical longs in energy are happy to cling on awhile; gold is responding once more to an inflationary thrust of policy which has seen as many dollars added to the balance sheets of the Big Five central banks in three years as would serve to pay for seven-tenths of all the bullion mined in the past three millennia.

To the extent that we have little positive to say about the prospects for genuine economic healing and recovery we can argue that this is already premature, but to the greater extent that such anaemia will only induce the quack doctors to administer a further, larger does of intravenous monetary poison, we could conversely argue that the party may have only just begun.

Having been up and down this roller-coaster of stop-go, stimulus-stasis three times already since the Fed’s first discount rate cut in 2007, it is difficult to ignore the presentiment that we are about to embark upon a fourth. Nor, being of the Austrian persuasion, is it hard to imagine that this next burst of treating symptoms and ignoring causes will prove similarly unavailing in terms of providing a final resolution of our self-inflicted ills.

If we additionally concede that even the most mule-headed Blue Skyer is susceptible of a little Pavlovian conditioning (even if we doubt his ability to draw the correct conclusion by any less painful means), we must also expect that this coming round will deliver less short-term growth, at a higher cost in price inflation, more quickly after its inception. One must follow this reasoning through to the prognosis that the rush for the exits when the next local maximum is deemed to have arrived will be equally less reluctantly embarked upon and hence that the inevitable downleg beyond it will be potentially even more violent that the one from which we have only recently emerged. Wash, rinse, repeat – und so weiter und so fort.

Hysteresis is the watchword, then, so enjoy the boomlet while it lasts but be ever ready to try to preserve what fleeting gains you can when the euphoria gives way to a funk, once more. Remember, too, that such a stagflationary trajectory is a meat-grinder for the guardians of capital and a spirit-sapper for the entrepreneurs on whom they and we ultimately rely. Only those who best serve Leviathan are likely to prosper in this Vale of Tears until the day dawns when we at last steel ourselves to break free from a repeated round of economic error and political poltroonery which has got us precisely nowhere, for all the plaintive bleatings of the biens pensants who insist that no possible alternative exists.

As so often, the question is not “if?” but “when?”.

We all know this international Central Bank supported house-of-cards is going to collapse – but WHEN?

I hope it collapses very soon (perhaps due to the shock to false “confidence” from a Greek default and other such developments), and I freely admit that my hope for a quick collapse is for political reasons (to help get Comrade Barack out of the Whitehouse), but I must also admit that I actually expect the farce to be kept going till next year.

Very depressing – for then the collapse will be just in time for newly reelected Comrade Barack to impose Emergency rule (for which the plans have already been drawn up by the Centre for American Progress and others).

Then Paul, is when we will hear calls for the repeal of the XXII amendmend. “Centre for American Progress” sounds exactly like ATLAS SHRUGGED.