The Japanization of the European Union

byThe Japanization of the European Union[1] Introduction The topic of my lecture today is “The Japanization of the European Union.” I…

For honest money and social progress

For honest money and social progress

The Japanization of the European Union[1] Introduction The topic of my lecture today is “The Japanization of the European Union.” I…

There is a changing of the guard at the European Central Bank this year with two important new appointments. Philip Lane, the governor of…

Professor Joachim Starbatty is a member of the European Parliament. He kindly hosted our event “The Lessons of Economic History” earlier this year. Here…

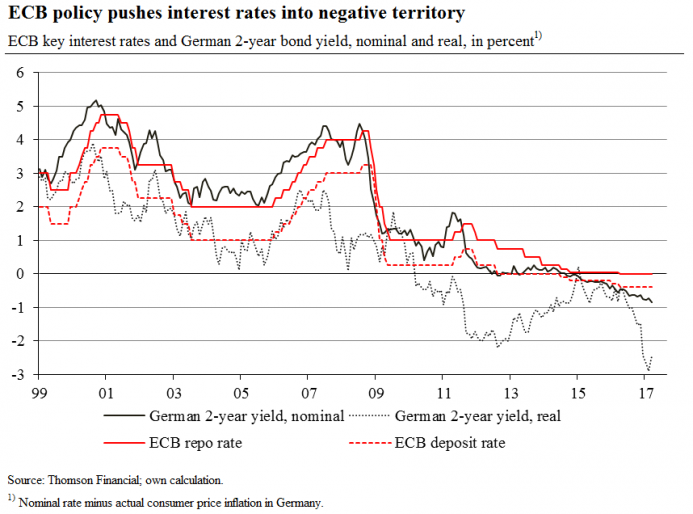

The European Central Bank (ECB) pushed its deposit rate to minus 0.4 percent in April 2016: Since then, euro area banks must pay 0.4…

Purely for geopolitical reasons, namely frustration at the failure of the governments of individual member states to respond to repeated calls for “structural reforms”,…

As discussed last Friday, Greece is back in the public spotlight and – hardly surprising – it is once again on the verge of…

Having already touched upon the UK’s shaky fiscal position, all that really needs to be added, now that the Chancellor has actually delivered his…

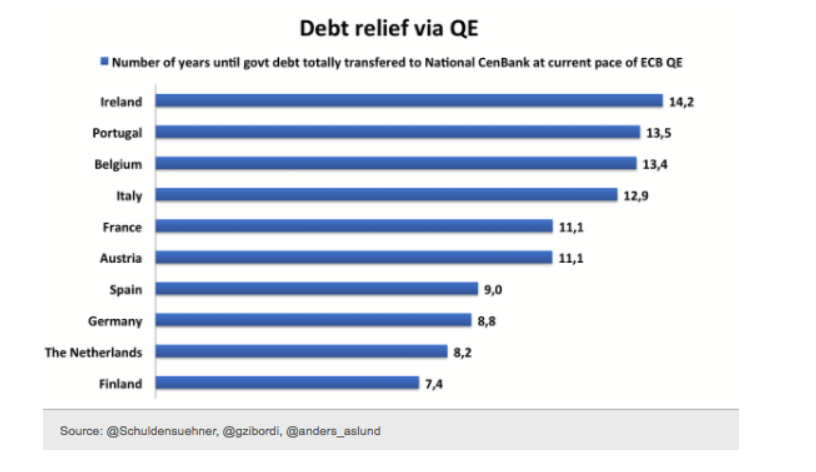

By Mike “Mish” Shedlock Source: https://mishtalk.com/2016/08/25/how-long-will-it-take-for-the-ecb-to-own-all-sovereign-debt-of-spain-germany-france/ Huky Guru on Guru’s Blog posted a chart that answers the question: How Long Will it Take For the…

Money, generally accepted medium of exchange, acts as a veil that confuse and blurs economic relations. This is especially true when it comes to…

On Thursday June 23 2016 the people of Britain voted in a referendum to leave the European Union (EU). Most commentators view Britain’s exit…