The Failures of the ‘War on Drugs’

byI would like to congratulate drugs… for winning the war on drugs. Ever since its declaration by Richard Nixon in 1971, a vicious cycle…

For honest money and social progress

For honest money and social progress

I would like to congratulate drugs… for winning the war on drugs. Ever since its declaration by Richard Nixon in 1971, a vicious cycle…

In economic terms, war and pandemic are the same without even evoking imagery of the virus as an invisible enemy or of a long…

omentous events usually leave strong memories on those who have lived through them, and those memories often become passed on to later generations in…

It seems that every generation or two, fundamental economic ideas are questioned and challenged. The reasonable and important idea that governments should balance their…

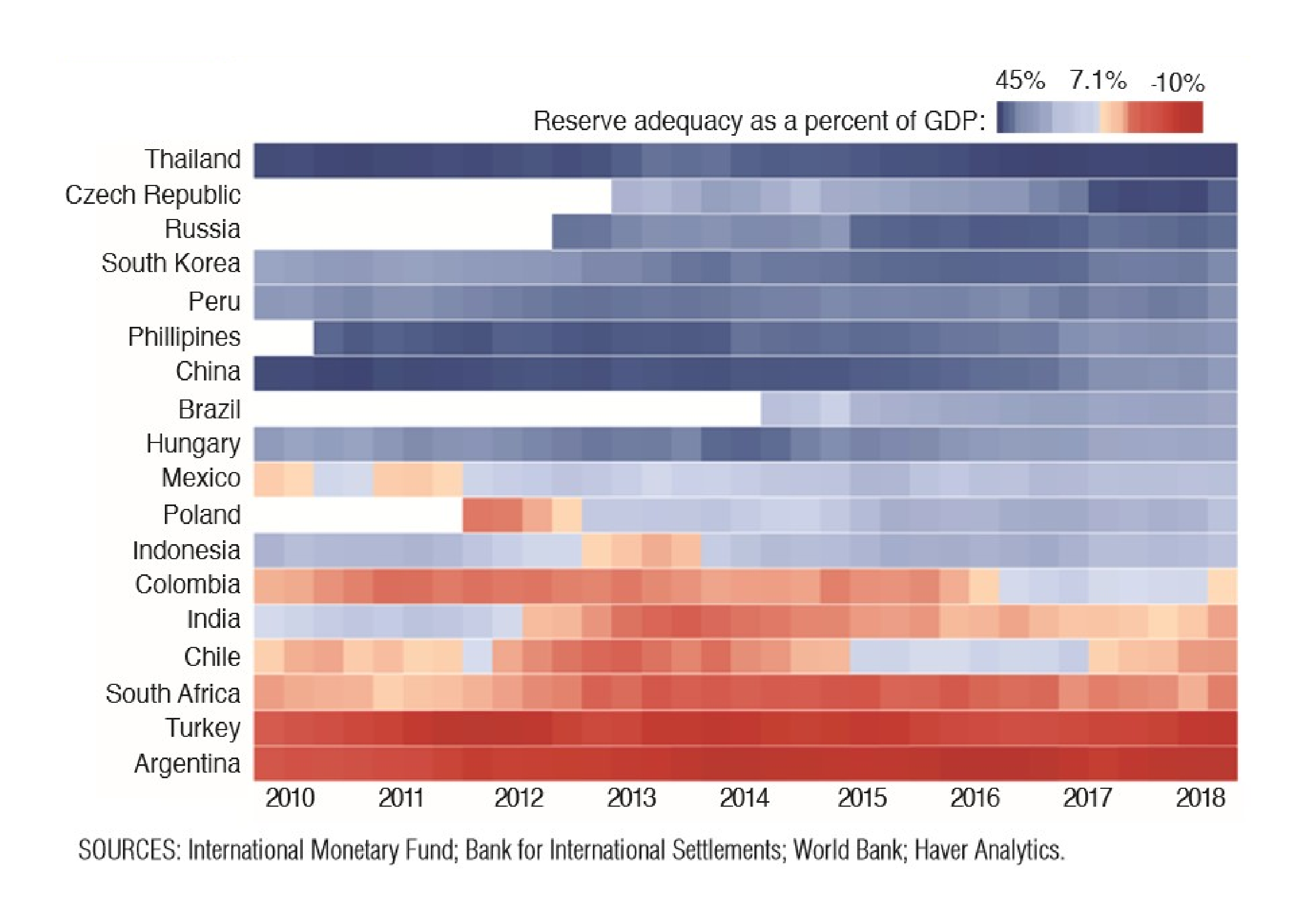

Emerging market currencies have suffered from US interest rate increases The Dallas Fed proposes reserve/GDP ratio as a simple indicator of stress If tightening…

By Joakim Book With the 2007-8 financial crisis came a splendid alphabetical soup of central bank interventions to stimulate financial markets, lower interest rates, provide…

“Events, dear boy, events.” Alleged response by the British Prime Minister Harold Macmillan, when asked by a journalist what is most likely to blow…

“A key prediction of traditional economics.. is that the economy as a whole must at some point reach equilibrium – a prediction made by…

Not waving but drowning – Stocks, debt and inflation? The US stock market is close to being in a corrective phase -10% off its…

“There’s a great deal of ruin in a nation.” Adam Smith, in correspondence discussing the Battle of Saratoga, which marked a turning point…