As Europe continues bailing out its troubled economies, a subtle point is sidestepped. Providing additional doses of liquidity has brought short-term relief to some of the most troubled countries. Greece’s €110bn bailout earlier this year allowed it to save its burgeoning government payroll from starving. Ireland’s drawing on the €750bn. European bailout fund to the tune of €85bn. has saved some privileged banks. The next country to get bailed out will likely also see its troubles sidestepped for another day.

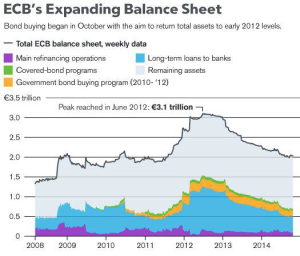

But the problem that no one wants to answer relates to what type of crisis this really is. Providing additional injections of liquidity may be a good Band-Aid solution if we are faced with a liquidity crisis. By expanding its balance sheet over the last two years, the European Central Bank has provided ample liquidity to keep its Eurozone banking institutions from failing. And if the ECB’s liquidity facilities weren’t enough, America’s Federal Reserve has been on hand to make U.S. dollar funding available at request. Tuesday’s extension of its U.S. dollar liquidity swaps reinforced the Fed’s commitment to maintaining a European banking system awash in credit.

Yet in continually ratcheting up the provision of liquidity, the ECB and the Fed have been battling yesteryear’s fight. Today’s crisis is fundamentally not of liquidity. It is one of solvency.

For a decade European governments spent beyond their means. Indeed, the ECB was one of the prime culprits allowing the newly formed Eurozone to pursue such prolific sovereign deficit spending. By allowing government debt to be used as collateral for its refinancing operations, the ECB ensured that Eurozone governments, especially Southern Eurozone governments, had access to cheap credit. With artificially reduced interest rates on their sovereign debt, Europe’s PIIGS economies were able to partake on a spending binge, with little heed for the coming liquidity crunch. The ECB, after all, had its hand on the lever to keep the liquidity coming.

Implicitly the ECB has treated the whole of the last decade as a liquidity crisis. Instead of functioning in its traditional role of lender of last resort, the ECB became a lender of first resort.

Today the use of liquidity has already largely been exhausted. The prolific spending of the past has created a solvency crisis. The governments of the Eurozone, aided by the excessive liquidity provided by the ECB during the last decade, have partaken on spending paths far overreaching any semblance of sustainability. An imbalance created in the past is now becoming apparent as these countries’ past debts come due.

In fact, the today’s recession is at its core not the result of “tight credit conditions”, “debt contagions”, or any other frivolous explanation. At its core we are faced with the realization that the previous fiscal state of affairs was unsustainable. By the time entrepreneurs realized that we were living in an unsustainable situation, it was already too late.

Of course, once you realize that the crisis is one of insolvencies the question that must be raised is what the best course of action is to get these insolvent situations solvent again. If we were indeed in the midst of a liquidity crisis, keeping the credit channels open may (and we must use the word cautiously) aid affected businesses.

An insolvency crisis implies one of two things. Either institutions are unable to pay off their debts as they are falling due, or, institutions have negative assets – liabilities in excess of assets.

The former seems to accurately describe the sovereign debt situation in Europe. Bond auctions are increasingly dismal. National governments are having difficulties raising the capital to meet their operating expenses. Normally capital is raised primarily through the financial markets – banks, mutual funds, insurance companies and the like purchase government debt as a “safe” asset for their portfolio.

The problem today is that this group of financial companies that typically funds government debts is under the second form of insolvency. The banking system in particular functions in an insolvent position as a normal state of its business affairs. Liabilities are always issued in excess of the assets available to pay them off – this is the fundamental basis of the fractional reserve banking system we are bound to today. As loans are issued in excess of deposits, a ballooning set of liabilities is permitted to be issued against a dwindling balance of assets.

The ECB allows the Eurozone domiciled banking system to issue up to 50 times the liabilities than assets are available to fund them. The Bank of England pursues an even more extreme path. With a reserve ratio on demand deposits set at zero, an unlimited amount of banking sector liabilities can be pyramided off an inexistent base of assets.

An insolvent financial system is unable to purchase additional amounts of government debt. Consequently, the sovereign debt crisis is unable to continue. The ECB pumping additional liabilities into the financial system cannot change the unalterable fact that assets cannot be created from thin air. Insolvency crises require a different exit plan than their less troublesome illiquidity counterparts.

Lacking a quick and easy method to create assets, the only solution to an insolvency crisis is to allow insolvent institutions to fail. Purging the bad debts from today’s financial system is an essential step in creating a sound foundation for recovery. Iceland, over the course of the past two years, has witnessed the bankruptcy of an insolvent banking system – one which had three large banks dominate the economy with liabilities amounting to 1100% of GDP. One would think that permitting such a dominant and centralized part of the economy to “fail” would cause undue hardship.

The purge of insolvent assets from Iceland’s financial landscape allowed for a fresh start. Government spending was forced to be cut as revenues were sharply curtailed. Talk of austerity measures that Britain and the Eurozone only hesitantly discuss became quick reality for Icelanders. An unsustainable situation came to an end, and Icelanders have commenced rebuilding with knowledge of the flaws of their past.

If the Eurozone could realize the same fate it too could have a quick exit. Past mistakes have been made, and insolvent institutions have been created. Allowing them to flourish further will do nothing but prolong the current economic malaise.

David,

Can you further explain your definition of insolvency. Are you saying that these banks have negative equity which would imply balance sheet insolvency?

Also, is a lack of liquidity not a key implication of either type of insolvency? Last, focusing on the balance sheet, wouldn’t most banks actually be cash-flow insolvent rather than balance sheet insolvent unless they had negative equity, in which case it may be both?

> Also, is a lack of liquidity not a key implication of either

> type of insolvency?

Yes it is.

> Last, focusing on the balance sheet, wouldn’t most banks actually be

> cash-flow insolvent rather than balance sheet insolvent unless they

> had negative equity, in which case it may be both?

If a financial institution has assets greater than it’s liabilities and it can show other businesses this then it can borrow to cover any immediate needs.

The problem comes – as I think you mentioned once before – when it doesn’t have greater assets, or when it can’t prove that it does. Some British banks, for example, have less than 1% greater assets than liabilities. In that situation creditors may doubt that their assets really are larger than their liabilities, then getting credit becomes a problem.

Thanks for that Current.

Have a Merry Christmas.