A great post by George Selgin: Is there a prudent second best?

I don’t think I’m adding anything original but as I understand things, George’s position rests on two claims. (1) In an “ideal” system (i.e. free banking) there would be an increase in the money supply in response to an increase in the demand to hold it. In other words the banking system would ensure that MV is stable. (2) In the present system, the costs of attempting to “do nothing” are higher than the costs of attempting to simulate a free banking system, even though you can’t do this perfectly. Therefore if V increases the Fed should increase M. Hence there is “a case” for QE.

Many Austrians deny the first point, and so it is obvious that they would reject the second. Peter Boettke is right to say that the second point doesn’t necessarily follow from the first (although I’m not totally sure if he fully agrees with the first point himself). But – and let’s take it as given that the first point is accepted – here are a few things to consider when thinking about the second point:

- As George says, the Fed is always doing something. “Do nothing” is not an option.

- If we don’t possess the knowledge required to know when the Fed should increase M, how can we possess the knowledge to declare that they were increasing it too much during the boom? If we literally have no idea whether money is too tight or too loose, surely this dramatically reduces the plausibility of using ABC as an explanation for the underlying cause of the crisis?

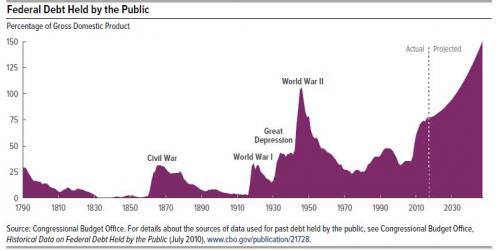

- NGDP is a better way to infer the monetary stance than consumer prices, or real GDP. Therefore thinking in terms of NGDP targets as opposed to inflation targeting is worthwhile.

- Market monetarism seeks to replace all discretionary monetary policy with a very simple rule. Targeting NGDP expectations is a contemporary version of a Friedman rule and also can be seen as a step towards free banking. Of all the monetary policy rule on the table, it’s hard to beat. *If* you want to have some policy relevance, this is where the action is. It directly leads to an acknowledgement that monetary policy should be neutral, and that it should distinguish between productivity shocks and reductions in AD. It would be a massive improvement over the status quo, albeit we’d remain a long way from the ideal.

- Even if you think there’s a case for the Fed to increase M, there’s a number of ways to go about doing it. QE is not necessarily the best. The likes of George, Steve Horwitz, etc, have been very clear from the start that QE as implemented by the Fed has been an error. And particularly on the Robust Political Economy grounds that Pete raised. There are two questions to consider: by how much do you want to increase M? and how? QE as practiced has dramatically increase Fed discretion and could be opposed on those grounds alone. It’s also not been accompanied by an effective communication strategy, meaning its supposed effectiveness has been curtailed. I’ve been in print myself arguing against it on both grounds (i.e. undesirability, and that it will fail on its own terms).

Finally, I sense that Pete (and many other Austrians) accept the basic arguments put forward above but just can’t bring themselves to be seen to be endorsing any action of a government agency. The analogy I use here is that the state is like a wife beater. We all see the damage being done but for whatever reason the person being beaten always offers forgiveness and a belief that things will improve over time. In which case the bystander/economist has two options. You could try to minimise the harm being caused. Or you could try to engineer an event so catastrophic she finally confronts the problem.

Maybe if the Fed tried to “do nothing” in 2008 there would have been such a crisis that faith in central banking would be completely shattered, and we would usher in a new era of free banking. In which case maybe +10% unemployment and a breakdown in monetary calculation “would be worth it”. But holy shit! Maybe if that had occurred it’d have been used as a reason to have an even more centrally planned economy, because instead of putting forward the ideas of liberty in a pragmatic, policy-oriented public debate, our best and brightest are too busy seeking the luxury of irrelevance!

I say this as someone who’s turned down opportunities to discuss the evils of central banking on TV because I know full well an uncharitable audience would fail to understand that you simply cannot spent 10 minutes defining terms and explaining caveats in a brief live interview. Bravo to anyone who has the courage to state their case publicly.

I can sleep at night because although people may mistake me as a Keynesian, a Monetarist, an endorser of monetary socialism, etc, my criticisms are more effective if they are informed criticisms; I find common ground with intellectual opponents where it exists; I have “spoken truth to power”; and I’m staying true to “good” monetary theory as I understand it. Such attacks say more about deficiencies in their knowledge than it does mine.

I have great respect for Joe Salerno and have learnt a lot from him. But I think George is right to say “there is a case for QE” and I think that needs to be opened up and discussed, not shouted down.

Lending should be from REAL SAVINGS – not credit-money bubbles.

When there is a credit money bubble (i.e. lending that is not from REAL SAVINGS) then it must be allowed to burst.

“But then there will be terrible suffering” – yes there will, but blame the people who created the credit-money bubble (by lending out “savings” that do not really exist) in the first place.

As for Central Banks….

They just make credit-money bubbles BIGGER than they otherwise would be (if bankers were just left to their own antics). For example the Benjamin Strong bubble of late 1920s – or the Alan Greenspan bubble of recent years.

As for the present “hair of the dog” policies – they have indeed propped up the credit money bubble (and the stock market bubble and, in Britain at least, the housing bubble).

Howrever, propping up bubbles is NOT a good thing – eventually this false economy will go.

The suffereing has not been prevented – just delayed (and the eventual suffering made WORSE than it otherwise woudl be).

There is no substitute for thrift (self denial) and hard work.

If people only save 1% of their income – only 1% of income is availabel for (HONEST) loans.

And money that is lent out is NOT available to the saver.

Two steps must be understood.

First saving is the REDUCTION OF CONSUMPTION by the saver (it is a SACRIFICE).

If I save 1% of my income – then I consume 1% less.

Also I take a RISK by lending some of my income (either directly or indirectly – via a bank) to borrowers.

Till when and IF I am paid back, I do NOT have this money any more.

On “fractional reserve banking”.

If REAL SAVINGS entrusted to the bank are (for example) one million Pounds and it lends out (in various complex ways) ten million Pounds this is NOT a “fraction” as ordinary people would understand the word “fraction”.

If I have one hundred Pounds and I lend you ten Pounds I have indeed lent you 10% (one tenth) of my money – and I DO NOT HAVE THIS MONEY ANYMORE (till when and IF you pay me back).

However, if I have one hundred Pounds and I lend you “one thousand Pounds” I am doing something different – I am (in one complex way or another) creating a credit-money bubble.

Such a bubble MUST eventually burst.

The “broad money” (the bubble) must shrink down towards the “monetary base” (the money that PHYSICALLY exists).

Any government effort to prevent “boom turning to bust” will just, in the end, make things even worse.

Lastly on the Great Depression.

It should be remembered that what we think of us the “Great Depression” was NOT just just a monetary matter.

There was indeed credit-money boom (bubble – all such “booms” are bubbles BY DEFINITION) in the late 1920s – the Benjamin Strong bubble. And it did indeed burst.

HOWEVER the real cause of the prolonged suffering in the 1930s (compared to the short term suffering of the 1921 crash – and other crashes going back to the Panic of 1819 (see Murray Rothbard – “The Panic of 1819” and “America’s Great Depression”) was the REACTION to the crash.

In all previous busts prices and wages were allowed to adjust – but first Herbert “The Forgotten Progressive” Hoover and then President Franklin Roosevelt did everything they could to PREVENT the adjustment of prices and wages to the bust.

This (and the international begger-my-neighbour trade war) is not a matter of monetary policy – it is a matter of direct government intervention designed (under the influence of the “demand” fallacy) to PREVENT the market clearing.

It is true that World War II was a period of such inflation (inflation hidden by price controls – the real prices are the “Black Market” prices) that government maintained wage rates became meaningless (so the market cleared by default).

However, the idea that a massive monetary expansion (the true meaning of the word “inflation” – which may or may NOT involve an increase in prices) is needed to enable markets to clear (i.e. unemployment to come down) is false. No previous bust had needed such a policy for markets to clear. Markets did not clear in the 1930s because the government DID NOT LET THEM CLEAR.

“But there was a collapse in the money supply of 1929”.

Please see above – there was no collapse in the monetary base. Gold was not stolen by the evil elves.

What happened was that “broad money” i.e. the CREDIT “MONEY” BUBBLE burst – back down towards the monetary base (i.e. the real money that actually existed).

If people think this is a bad thing then they should work to prevent the “boom” (i.e. the credit bubble) in the first place.

Not react by declaring that gold is not money, stealing privately owned gold, and voiding the gold clauses in contracts.

If banks (and other such) did not have the gold (the real money) they claim to be lending out, then they should not lend out what they do not really have (I repeat my point that lending out, say, ten times what you have is not a “fraction” as the term is normally understood – one hundred tenths is a “fraction”?).

If people save one ton of gold then one ton of gold is available to be lent out – and people (real savers) do not have this one ton of gold anymore (after it is lent out) till when and IF it is paid back.

Pretending you have vastly more gold than you actually have – lending out this paper “gold” and then (when the bubble inevitably collapses) saying “the money supply has declined – the government must DO SOMETHING” is not good. Not in 1929 and not at any other time.

Hear! Hear!

A little bit of light polishing and that comment would do well as a post on the front page. Well put.

Many thanks Mr Howard.

Of course in the “old days” it was easy to spot there was a problem.

When gold was money (the very term “gold standard” is so vague as to be an open door to fraud – so let us leave it aside) people still did not come out of banks with bags of gold as their “loans”.

Why not?

Well the official reasons were that the gold would damage their clothing, and was heavy, and they might get robbed on the street and….. (on and on).

Officially the gold was in the vault of the bank – but it had been moved from the account of the saver to the borrower (“credited to the account”).

Oddly the “depositor” was not told that his or her savings had been moved (the very word “deposit” makes no sense – how can one earn interest if the money is “deposited” rather tban LENT OUT).

But there was a more important point.

Had one gone to the bankers and said…..

“I see – so you give people bits of paper (as loans) representing the gold you have in your vault, MAY I SEE THIS GOLD PLEASE”

They could not have shown you the gold – because most of it DID NOT EXIST.

That was the true (as opposed to the official) meaning of “fractional reserve banking”.

Bankers did not lend out (say) nine tenths of the gold.

They lent out more like ONE HUNDRED TENTHS of it (many times the gold they actually had was, in various complex ways, “lent out”).

“But none of that matters now Paul – because gold is not money any more”.

Does anyone really believe that the banks have (in their vaults) the notes and coins that are now “legal tender” – that their “loans” (and so on) just represent these fiat notes and coins in their vaults?

If anyone believes this (that there is no gap between the “monetary base” and “broad money”, credit-debt) you have a shock comming.

A more honest system would have been as follows….

“You are not depositing your gold savings with us – if you want interest, we must LEND THEM OUT, which means you do NOT have this gold anymore till when and IF it is repaid”.

And to not lend out bits of paper (“representing gold in the vaults” – honest gov), but to just lend out the physical gold.

Yes I know you (the bankers) were just worried about the borrowers being robbed in the street, or the damage to their clothing, or…..

Yeah – of course you were.

You had no dishonest intent at all – not even slightly.

Now about that bridge I have to sell you…..

To be serious.

Electronic transfer of ownership are fine – as long as the physical commodity (gold or whatever it is) ACTUALLY EXISTS. As long as you really have the physical stuff in your vaults (which you do not – not even fiat notes and coins).

Sorry lads – but “one hundred tenths” (or whatever) is not a “fraction” as normal people use the word “fraction”.

The vast mountains of credit games of bankers (and other such) are indeed very clever – vastly clever and complex.

But in the end, it is just an electronic version of a House of Cards.

And NO you should not get government bailouts (open or hidden) when your House of Cards inevitably collapses.

“But then there will be terrible suffering”.

Of course there will be.

But bailing you out (with the “low interest rate”, “cheap money” policy) does not prevent the suffering.

It just puts it off – and makes it WORSE.

Brilliant

waramess – my head would swell with the kindess of your complement.

If my head was not already swelled up from all the tines I have been hit over the head – down the years.

I think that given an increase in the demand to hold money the value of money (expressed in terms of other goods) would simply rise. There is no need for an increase in the supply of money. George’s error is to see “money” as a good in its own right rather than a medium of exchange. At different times “real” money, such as gold, can be either. Fiat or paper currency is not a good and is a poor, even dangerous proxy for a medium of exchange.

If there is an increase in demand in a good (in its own right) say, grain, then it makes sense to increase supply of it. Not so for money. There is no gain there.

Money is not just a medium of exchange – it is also a store of value. And (as Carl Menger pointed out long ago) it is hard to see how fiat money (which can be created in unlimited quantities by the whim of the state – without warning) can be a dependable store of value. If it were not for government legal tender law and tax demands – would anyone regard these bits of paper and token coins as a store of value? And most “money” is now not even paper notes and token coins – it is computer fraud (numbers on computer screens that do NOT represent actual fiat money notes and coins in the vaults).

All money starts off as a good – the good (be it gold, silver or salt) is valued by people BEFORE it starts getting used as money. Only latter does the state come along and say “accept these tokens” (OR ELSE….) “we have the commodity you value – honestly we do…”.

On a Pound (although not on a Dollar) the lie “we promise to pay on demand…” is still written.

As for George Selgin – in the past he has pretended that all lending is from real savings (which is wildly false), whether that is his present position I do not know.

Of course, in reality, banks and other such do not even have real savings in fiat money (government notes and coins) to “cover” their loans. But then I explain the real situation (at length) above.