The term inflation is used by many people to mean rising consumer prices, regardless of the cause. Though most are aware of nonmonetary causes, there is a tendency to scrutinize the quantity of dollars whenever prices are rising. Milton Friedman famously said that “inflation is always and everywhere a monetary phenomenon.”

Bear with us, as we go through a bit of theory. We will address the likely consequences of Ukraine, both on prices in the short term and on the financial system longer-term, below.

Inflation from Useless Ingredients

The cause of rising prices is not always monetary. Before Covid, we wrote a lot about mandatory useless ingredients. This is when regulators and taxinators force producers to add things to their products, which buyers do not care about (and often do not know about).

There has been a steady march of added useless ingredients over the decades. But, like watching a child grow taller every day, you may not always think about the big change compared to five years ago (or 50 years ago, in the case of useless ingredients). It would be very difficult to estimate how much useless ingredients have added to the prices of each good.

How much do all the required airbags add to the cost of every new car? How many costs are added by all the emissions gizmos, and safety devices? The same is going on, in the fuel you pump into the car, the tires you drive on, and everything you put in the trunk when you go shopping.

The cost of these useless ingredients is high and rising. Before Covid, this was the biggest driver of inflation.

Inflation from Trade War

For a few years prior to the virus, another driver began to emerge. Trade war. For us, this is a broader term than just tariffs. Though, there have been many tariffs added in recent years. Some readers may assume these are targeted at China due to its military threat, but there have been American tariffs imposed on Scotch whiskey, Canadian lumber, and many other things. Like useless ingredients, the consumer is often unaware of tariffs and how they drive up the price of the 2×4’s they buy. So they assume that the cause is simple money printing.

Trade war is not limited to tariffs. In the wake of President Trump’s China policy, every corporate supply chain manager has been forced to rethink the jurisdiction risk of every supplier. They have been forced to embark on multiyear projects to change the mix of sources, reducing or eliminating suppliers in jurisdictions that are either out of favor today, or at risk to become out of favor tomorrow.

Intel and TSMC are both building additional factories in the US, at a cost of perhaps $100 billion. This stupendous sum is necessitated by trade war. Pre-Trump, this cost would not have been incurred. In the meantime, something is occurring which would have been inconceivable previously.

There are chronic shortages of computer chips. Also chicken wings, onion rings, and a myriad of other things.

And this leads to a phenomenon that would be curious if it were a simple case of money printing. Prices are, at once, both lower and higher. Growers of chickens are getting less per bird, while consumers are paying more. Canadian timber growers are getting paid less, while American home builders are paying more. Russia is getting paid less for its oil (and selling less volume), while freezing Europeans are paying more.

This is what economic discoordination looks like. Wider spreads, with both producers and consumers kept apart by a growing gulf.

Inflation from Lockdown Whiplash

This leads to a third nonmonetary cause of rising prices. The lockdown and its release have caused a sharp whiplash. It has hit shippers, truckers and warehousers. Shipping costs skyrocketed. Shipping times stretched much longer. And they became unpredictable. Businesses have been scrambling ever since, to try to somehow plan and keep generating revenues. Business models are forced to change.

Take car dealerships. In the old model, they had vast inventories on their lots. They could move it, by offering incentives to buyers (and sales staff). In other words, low unit margins times high volume. Now, they don’t have many cars in inventory. They can sell cars at list price, or higher. But it’s low volume times higher margin.

Would you rather be in the custom furniture business, selling a desk that takes you 8 months to make, for $60,000? Or in the furniture manufacturing business, selling 10,000 desks that it takes your employees 8 hours to make, for $600?

Car dealers previously were limited by the number of buyers they could find. Now they are limited by the number of cars they can obtain. That’s a pretty big change, and not for the better.

Non-Linear and Synergistic Effects on Prices

There can be a non-linear synergistic effect between multiple nonmonetary drivers of higher prices. For example, the UK passed a law forcing coal- and oil-using industries including power generators, to switch to natural gas. And it also passed a law banning domestic production of natural gas. The total impact on energy costs, from the combination of both green energy restrictions, is probably much greater than either alone.

And there is another synergistic effect, with another driver. The turmoil in shipping and logistics pinches the UK’s supply of natural gas, with a further magnified effect on prices.

And now, in the wake of Ukraine, it is increasingly dubious that gas produced in Russia will continue to be available in Europe or the UK. The price of natural gas at the Netherlands terminal is 13 times higher than the price of natural gas in the US. Food production depends on natural gas because fertilizer production depends on natural gas. So this will reduce food production.

Speaking of food, Ukraine used to be a big exporter of wheat, accounting for 10-15% of global wheat exports. Will those exports continue? We suspect another big shock to the wheat supply is coming. On top of the shock due to the lack of fertilizer. The price of wheat is reflecting this already, having logged its 6th consecutive “limit up” trading day.

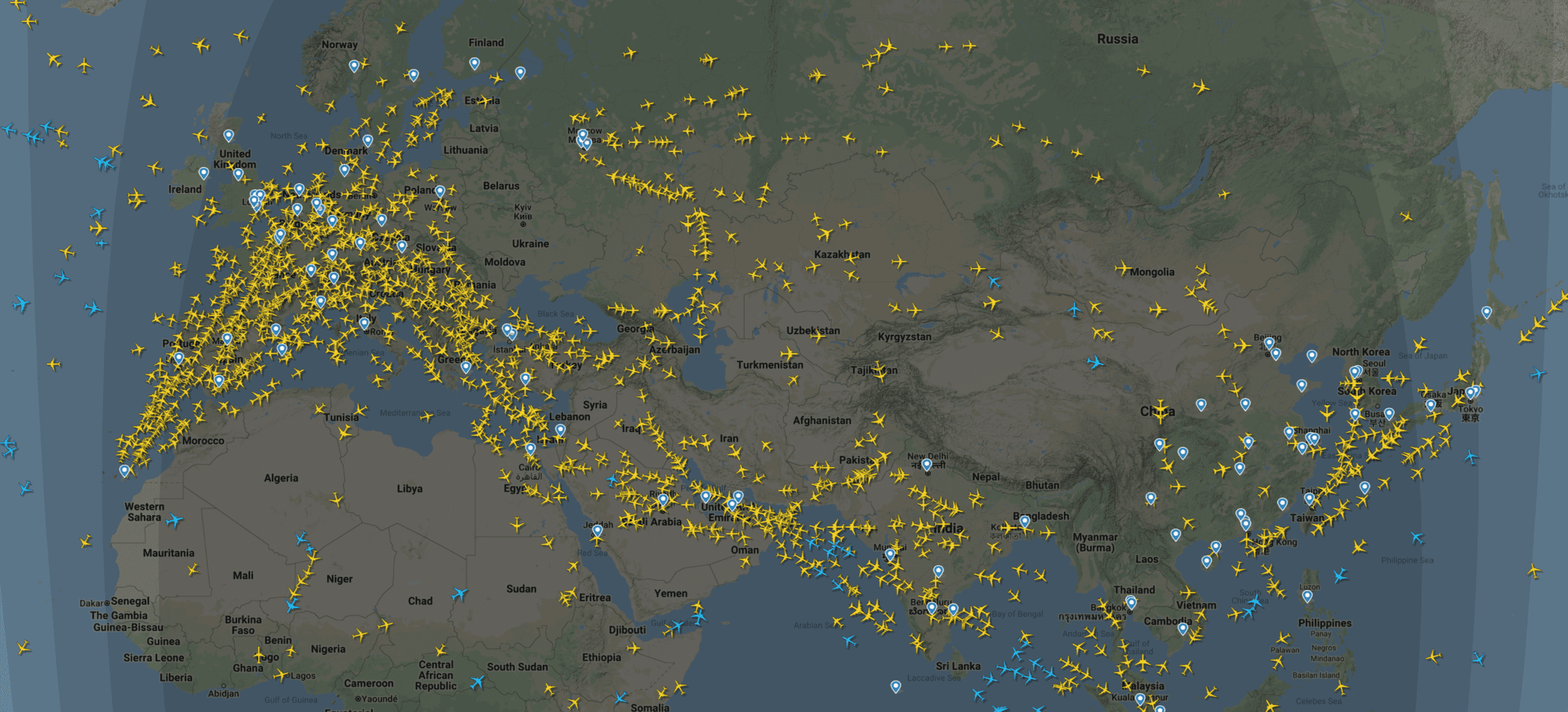

Here is a picture of the commercial airplanes in the air, as of Saturday afternoon (Arizona time).

Obviously, there are no planes over Ukraine at the moment. Also Belarus. There are some over Russia, but not to or from cities in Europe or America. Has anyone thought about the implications for air travel? At the very least, certain routes will become much longer, as the planes are forced to go around. Ukraine is a fairly large country, and Russia is huge. What will be the impact on trade of goods?

Inflation, Who’s to Blame?

We can be sure of three things. One, goods will become generally scarcer, higher priced, less predictable, and more difficult to source and plan. Two, the ensuing increase in prices will be blamed on the Fed for printing too much money. Three, the root cause is actually nonmonetary. It bears repeating that goods will become genuinely scarcer.

On an amusing note, The Economist just sent us this article, asserting that central banks should somehow “ignore soaring energy costs” due to Ukraine, but “they must continue fighting home-grown inflation.” Which means that they recognize that central banks cannot change the growing scarcity caused by war, or the effect which is the rising price of energy. Which implies that The Economist knows that war is a nonmonetary driver of higher prices. But The Economist doesn’t realize that the other causes of rising prices are also nonmonetary.

This concludes Part I. In Part II, we will revisit the fallout from Ukraine, Russia, and China’s challenge to the US Dollar system, and whether Russia could enact a gold standard with its gold reserves.