With the halls no longer decked with boughs of holly and the wassailers at last stuffed full of figgy pudding, we have all reluctantly begun to struggle back to our desks, turn on our Bloomberg screens, and wearily face up to the long slog ahead towards the annual profit target.

Even though the New Year is still wrapped in its swaddling clothes, it is hard to avoid the jaded feeling that the market has already arrived at an all too cosy consensus about how events will unfold in 2013 and where the money is to be made as they do.

The Yen will continue to fall and fall under the maniacal compulsion of the new Japanese government; bond yields will finally cease their three-decade decline; and stocks will (of course) rally, probably dragging industrial commodities with them. In Europe, the worst is widely held to be behind us – even though nothing much has been done there beyond persuading traders that the line of least resistance lies in not calling Mario Draghi’s bluff when he insists that sovereign spreads must not widen. China’s typically sagacious new central planners will somehow ‘rebalance’ the ailing giant that is their fiefdom by pouring yet more concrete and digging yet more holes without this time stumbling into a further mindless duplication of capacity, sparking a divisive property rush, or re-igniting a socially disquieting round of consumer price rises. Perched high above, in the crow’s nest which sways alarmingly above this Ship of Fools, the Bernanke Fed will keep on buying however many of the obligations of an incurably profligate government it feels like monetizing, thereby hoping to prise the prudent out of their more passive habits of saving by means of the insidious, corrosive, time decay which negative real interest rates visit on the thrifty and, in doing so, it will seek to insure us against all possibility of renewed recession.

Easy, isn’t it?

Well, perhaps. But before we start spending our bonuses before we have truly earned them, let us first pause to consider whether any or all of these suppositions are really imbued with the full hue of inevitability or whether instead an all too typical mass disappointment will set in, either around the start of February (as has traditionally been the tendency when the last winning trade of the old year is carried too eagerly on into the new) or sometime in the Spring (as has been the case in the last three years of policy undulation and Risk-On/Off hysteresis).

Take the US, for example. Just like the Mayan fiasco of prophecy, the budgetary apocalypse of the so-called ‘fiscal cliff’ (a hackneyed phrase whose overuse grates on the ears almost as much as that damnable cliché relating to metallic containers, public highways, and coups de pieds) has been partly averted, even if we can all look forward, in the coming weeks, to another round of facile political posturing ahead of the near-inevitable debt ceiling extension.

Rather than cheer, however, any rational investor would find this procrastination a mater of deep anxiety for, as Laurence Kotlikoff points out, it is not so much the minor contour change of the ‘cliff’ which should be exercising our concerns, but the terrifying, Miltonian ‘abyss’ which lies beyond it in a country where the accelerated transmutation of ageing Baby Boom tax payers into voracious entitlement eating retirees is adding no less that $11 trillion a year to the unpayable $222 trillion NPV of the nation’s overall sum of actual and contingent liabilities.

For now, though, even if the recovery is a deal more anaemic than anyone seeking votes might hope, America has managed to avoid slipping back into the mire in the way so many of its peers have done, where, that is, these latter have been fortunate enough to free themselves from the choking quagmire of unresolved crisis in the first place.

By all accounts, the economy – and by extension, a stock market flattered by the artificially exiguous discount factors applied to its prospective earnings stream – has much going for it: corporate profits are elevated, cash flow is at record highs, wages are subdued, the buying-back of equities is proceeding apace, that last aided greatly by a booming market in corporate debt . Capital expenditures are on the rise (if not so impressive in inflation-adjusted, net – rather than nominal, gross – terms) and payrolls are indeed expanding if not as rapidly as some might wish.

Moreover, the broad brush of the overall jobs numbers has been obscuring the heartening detail that the country’s more productive sectors are making their contribution to re-employment (manufacturing and the extractive industries have, between them, added almost 600,000 to the roster since the trough), while the bulk of the retrenchments have come in the non-productive, if not parasitical, sectors of finance (mea culpa!) and government.

The main concern here is that, despite the Fed’s ongoing efforts to force everyone to swim by flooding the land in liquidity, overall business revenues have undergone something of a deceleration in recent months and regular surveys of small businesses are obstinately throwing off readings typical of a slump, while claims of rediscovered vigour in the enfeebled construction sector seem to be belied by the trifling gains in headcount and hours worked in the field, not to mention the refusal of mortgage purchase applications to shake off their post-crash sloth, or of office vacancy rates to decline in any meaningful manner.

In Europe, politics may yet play an unexpected part, not least in Italy where Il Caviliere seems to have found a way to manoeuvre himself back to the centre of things in the form of the partial self-denial of ambition encapsulated in his faction’s deal with its erstwhile allies of the Northern League, under the terms of which he would settle for the finance minister’s job. However that particular gambit pays out, it seems certain that the hustings everywhere will resound to cries of repudiation for anything associated with the slow grind of Orient Express Austerity (i.e., that pernicious assault on the commonwealth which seeks to keep an overgrown and intrusive state as large as possible, no matter what the cost to that enterprising and self-reliant middle which is otherwise most likely to spark a renaissance).

Even in Germany, the cracks have begun to appear as the Merkel coalition has already delivered a sackful of costly pre-election sweeteners to keep the electorate onside in this, the key year for the coalition. As one perceptive acquaintance put it, we should expect little else when the struggle for power will be conducted between what he sourly called the red socialists, the green socialists, the yellow socialists, and the black socialists.

For our part, it has always been the contention that the true test of Germany’s avowed resolve to insist upon budgetary discipline and at least the pretence of monetary rectitude would arrive if and when the country’s recent good fortune began to run out and its own mighty engines of growth were heard, at last, to sputter and cough.

With business revenues now falling in all sectors, except that of what are probably inflation-boosted consumer non-durables (making the MDAX, if not yet its larger sibling the DAX, seem historically expensive by comparison) and with industrial production and exports each having suffered a three-month retracement of a magnitude not seen outside either 2008’s global ‘sudden stop’ or the post-Reunification hangover, we’ll see the test of our thesis that the Bundesbank may soon pass from a show of Schlesinger-like sternness to its polar opposite of Welteke-like vacillation.

Curiously, this slowdown seems to be taking form despite an intensification of the Eurozone’s dysfunctional ‘biflation’, a sharp divergence in monetary trends between the core and the periphery which has seen the key aggregate grow at accelerating double digit rates in the Eastern Frankish Realm and barely growing (if not actively deflating) in the Western half of New Carolingia.

Some of this inconsistency is largely to be explained by the transfer of deposits from the PIIGS – where they run a risk, however vanishing one is meant to believe it is, of not only being lost in a local banking collapse, but of being summarily redenominated in a devalued numeraire – to the perceived safe havens of Germany, Luxembourg, Finland, and the Netherlands. When such monies come to rest in banks north and east of the Rhine, they are not immediately intended for spending on the output of the Mittelstand: their ‘velocity of circulation’ is preternaturally low, if you will.

However, that this is not the full story can be seen from the fact that, since Draghi quelled the incipient panic last summer when he issued his resounding boast to ‘do whatever it takes’, the tell-tale TARGET2 balances which reflect this twin-sided process of credit withdrawal and flight-to-quality have undergone a partial decline which we can quantify roughly either by way of the shrinkage of the joint Spanish-Italian total (or of that of its De-Fin-Nl-Lux counterpart) of some €110 billion seen between August and November. Alongside this, non-currency portion of the money supply in the former has shrunk by €6.2 billion (-1.8% annualized), while that in the latter has shot up by €77 billion (a massive 19.4% annualized which stretches to 26.0% in Germany alone).

If these funds, too, are not being spent with quite the abandon they were a few short months ago, it might be taken to indicate that conditions are worsening and sentiment darkening more drastically than the superficial optimism of the securities markets would have us infer.

The one place where things do seem to have taken a decided downward lurch is in France. After coming back broadly into balance, its T2 debits jumped back up to €43 billion in October (the last period for which the BdF has seen fit to publish its balance sheet). Alongside this, there has been a sharp, €15 billion, -10.5% annualized decline in non-currency money supply which has served to take the annual rate of change close to zero in real terms and hence very much back into the danger zone.

It can hardly be a coincidence that this mini-run occurred in the context of the spat over the possible nationalization of Arcelor Mittal’s steel works; the implosion into internecine strife of the UMP opposition; and the disarray so evident at the heart of Hollande’s administration – not least regarding the status of the soak-the-rich tax – which led to the international embarrassment of Gerard Depardieu’s very public defection to the Russians.

The country, which has seen debt/GDP jump 20 points since the crisis (and with ongoing deficits of ~€2 billion a day do add to the tally) and which has a €40-45 billion structural–looking current account gap to fill, is not entirely securely placed in the affection of the world’s investing public even if the implicit support of the rest of the European mechanism makes a full-blown flight an unlikely prospect just yet. Nonetheless, all this bears watching.

Just across the channel, the fall of the services sector PMI to a 3 1/2 –year low, coupled with a dip in the construction analogue the bottom reaches of its last two years’ range, has raised the spectre of a ‘triple dip’ recession. Notwithstanding this, the UK manages to run a record trade gap in goods, clearly in excess of £100 billion a year, leaving the overall trade deficit of £36 billion a bare £3.8 billion less deep than it was at the peak of the boom and a current account which is beginning to push into a zone which heralded the last two sterling crisis – in the mid-1970s and during the first ERM break-up.

Ironically, this has come about as the BOE’s latest efforts at QE have finally had some purchase on the nation’s stock of usable money. Between February and November last year, the Old Lady’s balance sheet expanded by £90-odd billion and money supply rebounded from its post-Crisis lows, climbing £70.6 billion at an annualized rate of no less than 10%.

Loose money, loose fiscal policy (the shortfall is still running at some £10 billion a month), low competitiveness, and a weak leadership unable to steel itself to do anything to address the issue. This all sounds horribly familiar to this particular seed of Albion.

All of which brings us to China (sigh!).

No-one can surely need to be told that the last few months have seen a modest improvement in the Middle Kingdom’s fortunes which has auspiciously coincided with the induction of the new leadership. In part, this was grounded on the usual year-end orgy of spending undisbursed government budgets, in part on the typical fourth quarter acceleration which took place in the money supply. This last quickened to a 34% annualized rate from the third quarter’s unchanged pace – impressive enough, perhaps, but still the slowest closing burst in four years. Furthermore, the volume of new loans granted – seemingly hamstrung by lacklustre deposit formation – touched a 3-year low, with the important medium-long term sub-category dipping to a 4-year nadir.

But if the banks were not officially in the game, the ‘shadow system’- including Xiao Gang’s Ponzi component – certainly came up trumps!

‘Total Social Financing’, as it is called (and less equity issuance), outstripped boring old bank loans by a factor or 1.7:1 in the final quarter of the year and constituted no less than 72% of all new credit extended in December. Compared with the same month in 2011, new, official, on-balance sheet bank loans declined 38% from CNY733 billion to CNY453 billion, while all other forms of credit rose 112% from CNY538 billion to CNY1, 139 billion.

Now some of this shift is probably not entirely a retrograde step, at least not to the extent that it represents a genuine entrepreneurial attempt to circumvent China’s antediluvian, financially-repressed, SOE-favouring, bank-coddling regulatory framework and instead tries to put people’s savings to work at a suitable rate of interest, funding genuine productive undertakings.

The problem is that some sizeable – if necessarily unquantifiable – fraction also comprises local government boondoggling, loan sharking, and outright fraud. No wonder the central authorities moved last week to clamp down on the activities of the lower tiers of government in this regard.

To put all of this in come kind of context, it looks as though every extra renminbi of incremental GDP in 2011 was ‘bought’ with around CNY1.76 in new credit: last year the ratio was 3:1. Capital efficiency, anyone?

Moreover, when we look at liquidity, matters become even more pressing. In 2011, the system was already pyramiding Y5.50 on top of every new Y1 of actual new money created (2.54:1 for the shadow component). Last year the overall ratio was 8.22:1 and the shadow one stretched to 3.87:1.

And what is all this moolah being used for? For moving away from a malinvestment-led graveyard of capital such as has been constructed over the past decade of SOE princeling dominance? It certainly doesn’t look like it.

‘Urbanization’ may be the new buzz word (and one about whose exact meaning we still maintain certain caveats), but this just means that instead of crushing returns at home and abroad (and piling up zombie loans on the books of the pliant state-owned banks) in such sectors as aluminium, steel, ship-building, photo-voltaic, etc., China now seems to wish to emulate post-bubble 1990s Japan with a whole host of non-paying propositions aimed at the domestic, rather than the international, market.

Take commercial real estate. Forced to cut back on their residential excesses, developers have been parlaying a good part of those new funds into building shopping malls wherever they can cut a deal with those paragons of municipal virtue, their buddies at the local land office. And, typically, they have not done things by halves for, as a recent press report made known, between now and 2015, if all goes according to schedule, China will add no less than 600 million square metres of mall floor space (around 120,000 football pitches’ worth). For comparison the ICSC estimate of the existing stock of US shopping malls comes in at around 650 million, around half the nations’ overall retail area.

Then there are the subways. All well and good in principle to reduce congestion, increase safety and convenience and lower logistic costs, but they are hardly going to pay even their maintenance charges, much less their construction costs if the present economics are anything to go by.

As the China Daily reported in what was – for the sensitive tenor of the times – an unusually critical article, doubts are already surfacing about the sustainability of the current programme.

Keen to spare the new bosses the loss of face of a soggy end to a soft year, in September, the NDRC suddenly approved 25 subway projects in 18 cities, for a total investment of more than CNY800 billion. Still furiously pump-priming, by November they had authorised four more cities — Beijing, Nanchang, Fuzhou, and Urumqi — to commit to plans requiring another CNY135 billion even though 35 cities had already broken ground on such projects in 2012, for an estimated ante of CNY260 billion, said the paper, citing a report of the Comprehensive Transport Research Institute of the commission.

Among the doubters, was one Wang Mengshu of the Chinese Academy of Engineering who told the interviewer that:-

A city is eligible to build subways only if it has an urban population of more than 3 million, an annual GDP that exceeds 100 billion yuan, and a local government budget higher than 10 billion yuan. In addition, the one-way traffic flow must reach 38,000 people at peak time, according to the National Development and Reform Commission…

“However, some less developed cities in inland China have manipulated the figures to meet the requirement,” he concluded.

Quelle surprise!

One other thing to note is that, despite running a trade surplus of $235 billion and attracting FDI inflows of what will turn out to be around $95 billion over the 10 months since the last lunar holiday, the official count of foreign exchange reserve holdings shows zero net gain for the period. Subtracting outward FDI of an estimated $70 billion (and noting that euro and sterling parities versus the US did not undergo any significant changes in the interim), that leaves a cool $260 billion unaccounted for.

No wonder the North American and Australasian press is rife with tales of Chinese visitors getting stopped at customs for not declaring $10s of 1000s of bills stuffed into their luggage, or of their less than discreet presence at housing auctions in their destination countries. All well and good, you may say, if the external surpluses are being recycled into the hands of private individuals, rather than being directed, via purchases of government securities, to the dead hand of the state, but it nonetheless speaks volumes about how the insiders view the prospects for wealth preservation, much less further capital gain, at home.

It is presumably on such grounds as these that Bernard Connolly recently compared present day China to 1830s America – an era your author dealt with in the fifth chapter of ‘Santayana’s Revenge’. Glancing back at this today, we can see where the similarities lie: a vast orgy of infrastructure spending taking place in a wildly uncontrolled manner by eager local governments; a febrile property market in denationalized land, rampant speculation in commodities – all financed by pliable, politically-controlled banks and their shadow market counterparts.

Tick…tock… tick… tock!

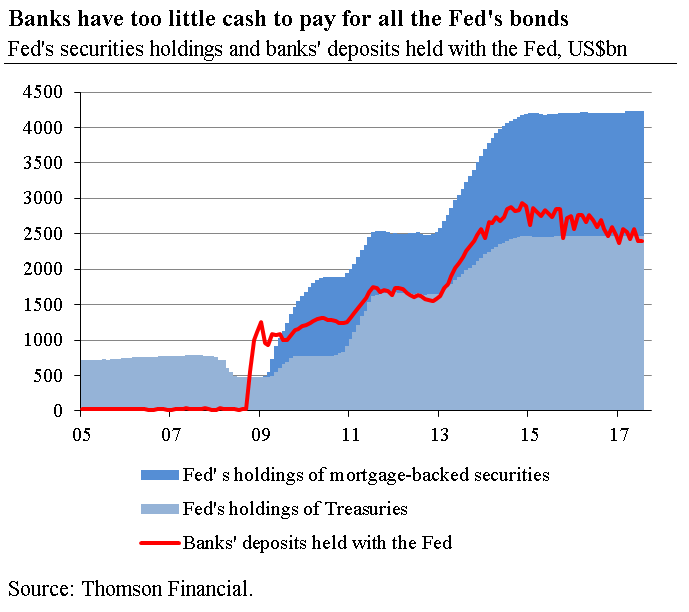

So, as we started by saying, we are uneasy regarding the consensus, but, for all the whispers that the Fed is about to become a deal less accommodative—and frankly, we’ll believe it when we see it—it doesn’t look as though anyone is short of anything out at the back end, even if that bear market dog-with-fleas, the 5-year, has seen specs switch to the other side of the trade in the past few weeks That said, a number of the key interest rate charts are showing some signs of stress, with a number of trend breaks to be found here and there, not least in the US.

Hardly the calamity of 1994 as yet then, though the one area which does bear watching is the Japanese bond market.

It may be too much to hope that Abe and his coterie of economic illiterates can grasp the fact that by trying to favour his export lobby, he is raising Japanese input prices across the whole economy, and so not only potentially eroding margins but reducing real incomes and hence possibly hurting both the supply and the demand side of a system which hardly needs to be inflicted with any further disadvantages. But what he might take cognisance of is that any lack of trust he engenders in the value of both the currency and the mountain of government debt which, in the main, provides its backing—not least on the balance sheets of the banking system—might begin to cost him more than he can possibly hope to gain by stimulating ’consumption’ like the good little Keynesian he is.

Yes, the country needs, once again to re-orient itself, as it did in the wake of each of the major busts of the past 20 years. Further, it can probably not rely so heavily from here on upon supplying China’s vast, subsidized processing trade with high value-added inputs for incorporation into mass consumer products and transhipment to a West not so willing or able to indenture itself so as to buy them. This would have been the case even before the casus belli of the Diaoyu/Senkaku island dispute put business relations between the two prickly neighbours into the deep freeze. No one suggests that this will be swift or simple to effect, but given that the country has done it several times before, there is no prima facie case to suggest it will prove unable to do so again.

If Abe really wants to help, he should get someone to pull up a chart of what happened during the term of office of his predecessor Koizumi. Government shrank and a re-invigorated private sector expanded into the gap. Even if the aggregate GDP numbers recorded this as at best a minor victory, the quality of the whole was improved and hope of something greater briefly flickered into life before the experiment was prematurely abandoned.

The state and its pampered banks have everywhere reduced private initiative to near impotence, if not to outright Randian insurrection. It’s about time it quit its infernal meddling and let the wealth creators at the problem once again.

I suspect they’d be more than happy to have the opportunity to show what they can do, if asked.

I doubt that manufacturing in the United States is as strong as is claimed.

And, even if it is, the rest of the economy (for example the hopeless government finances) will drag it down. The very thing that is helping the stock market now (the flow of funny money from the Federal Reserve) will destroy the markets – and destroy them soon.

“Moreover, when we look at liquidity, matters become even more pressing. In 2011, the system was already pyramiding Y5.50 on top of every new Y1 of actual new money created (2.54:1 for the shadow component). Last year the overall ratio was 8.22:1 and the shadow one stretched to 3.87:1.”

Dear Sean, above paragraph is very hard to understand. Could you elaborate it a bit.

Thank you!