CityAM Op-ed on Blockchain Technology and Friedrich von Hayek

byI had an op-ed published by CityAM last Friday, it goes into how blockchain technology will enable FA Hayek’s vision of an economy that…

For honest money and social progress

For honest money and social progress

I had an op-ed published by CityAM last Friday, it goes into how blockchain technology will enable FA Hayek’s vision of an economy that…

Matt Ridley, in The Times [paywall restricted], considers the political relevance of the values of 19th century Liberals, including Richard Cobden. Surely wanting government…

Incoming from Tom Paterson, chief economist at “Gold Made Simple”: I’m currently travelling around Europe in my VW campervan with my my wife and…

Editor’s note: this article, under the title “No end to central bank meddling as ECB embraces ‘quantitative easing’, faulty logic” appears on Detlev Schlichter’s…

It isn’t often that a Bank of England Quarterly Bulletin starts “A revolution in how we understand economic policy” but, according to some, that…

There are many times when working alongside the TCC team I have to smile. Having read a City AM article by our own Dr….

Earlier this morning I updated The Cobden Centre’s media page. Since September we have not only again doubled the volume of our coverage but…

Sean Corrigan is a good friend of TCC. Yesterday, he appeared on CNBC where he provided a masterful overview of current events on the…

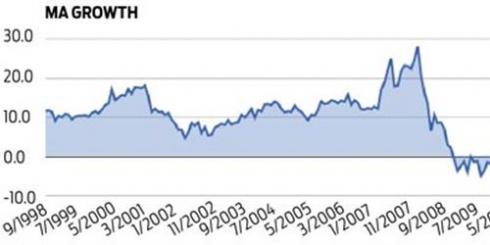

Via Honesty is best policy | The Jewish Chronicle, I set out MA, the Austrian measure of the money supply developed by Dr Anthony J…

Today is the fortieth anniversary of US President Richard Nixon closing the gold window and bringing in for the first time in history a…