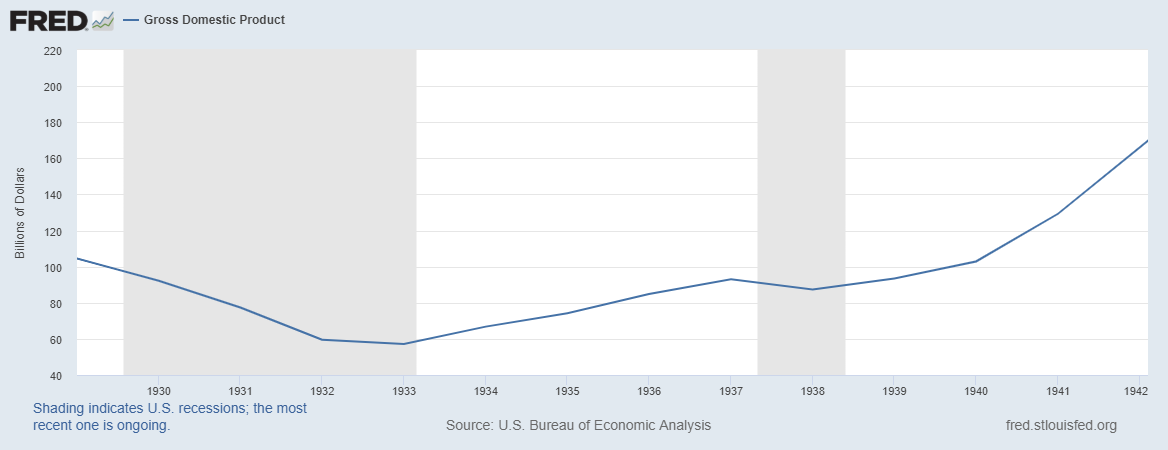

When does a recession become a depression?

byDefining a depression as opposed to a recession is open to wide interpretation Recessions are a natural part of the credit cycle Depressions…

For honest money and social progress

For honest money and social progress

Defining a depression as opposed to a recession is open to wide interpretation Recessions are a natural part of the credit cycle Depressions…

By Henrique Schneider Around the world, productivity growth has been slowing. In developed economies, productivity has risen by less than 1 percent annually for several…

The world seems to be on fire. A couple of months ago, the economic upswing was still firmly established, production expanded, and unemployment was…

“As I’ve written in past memos, I have an indelible recollection of the first book I read as a Wharton freshman in 1963. The…

Through most of the coronavirus crisis, those who have made the case for stay-at-home, reduce or stop work, and narrow the range of retail…

Here is a typical statement regarding supply and demand: “if the demand for any product increases, given the existing supply, the price of that product…

Economists who understand credit cycles expect the current cycle to enter its crisis stage at any moment. Furthermore, it combines with increasing trade tariffs…

Not too long ago, we wrote about the so called Modern Monetary so called Theory (MMT). It is not modern, and it is not…

New entrants into every aspect of banking were encouraged by two recent regulatory developments: the Open Banking initiative and the ‘sandboxing’ exemptions from regulations….

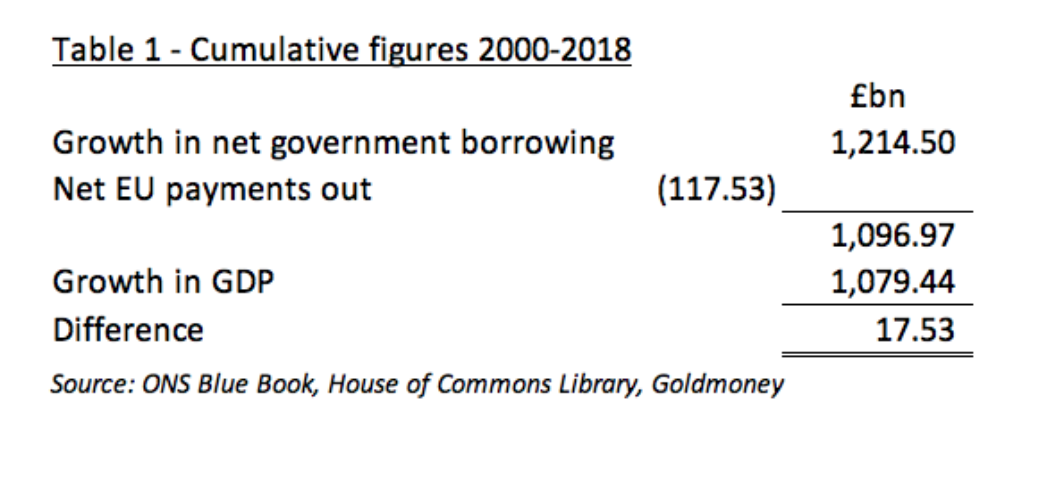

This article demonstrates that only government borrowing in the US and UK drives GDP growth. This surprising conclusion is confirmed by long-run statistics. GDP…