Trump’s “American Greatness” Also Political Paternalism

byMind your own business. Every one of us has thought or said words to this effect when others have told us how to live…

For honest money and social progress

For honest money and social progress

Mind your own business. Every one of us has thought or said words to this effect when others have told us how to live…

by Henrique Schneider One particularly important lesson to learn from the Covid-19 drama is which political decisions could help companies through the crisis. It…

One of the sorriest aspects of almost all political discussions nowadays is how often they seem to degenerate into rude ad hominem attacks rather…

July is the month when Americans celebrate the signing and then the announcement of the Declaration of Independence on July 4, 1776. While this…

By Nathan A. Kreider The great struggle in economic science has been the formulation of theories that accurately describe the real world. Though this…

An old adage says that tragedies often come in threes. Certainly, the first half of 2020 has seen a version of this. First, the…

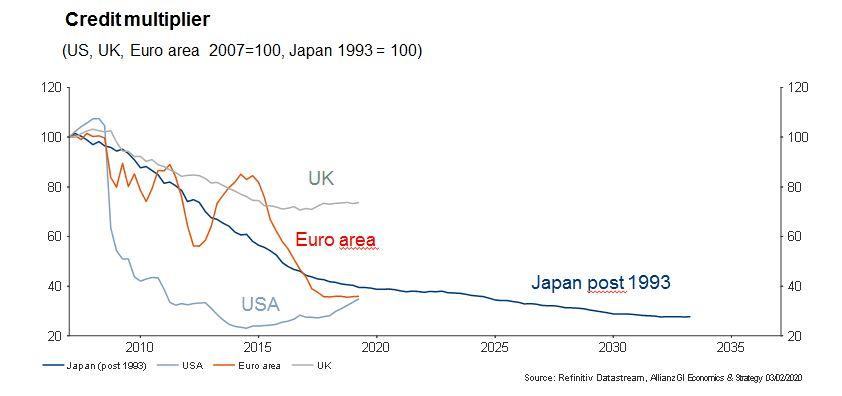

Stock markets have rebounded from their March lows on fiscal and monetary stimulus Corporate bond spreads have narrowed in their wake The prospect…

Even in an era when modern medicine and technologies are adding to people’s lifetimes, along with the gains in general human economic betterment, it…

The coronavirus is a human tragedy, but the markets remain sanguine A slowing of global growth is already factored into market expectations Further…

We grow up in the family. We expect fairness from our parents. Fairness in the family means equality, tempered by some measure of “to…