When the tectonic plates underneath society shift, confusion reigns, together with wishful thinking.

It appears that financial markets have again managed to get themselves into a state of unrealistic expectation. The European summit this coming Sunday (or the follow-up summit on Wednesday) is now supposed to bring a “comprehensive plan” to solve the European debt crisis. Of course, nothing of the sort will happen, and for a simple reason: it is impossible. Those who cherish such fanciful hopes are naïve and will be disappointed.

Let’s step back and look at the problem, which in a nutshell is this: the dominant societal model of the second half of the twentieth century – the social democratic nation state with its high levels of taxation, regulation and stifling market intervention, and thus increasingly dependent on a constantly expanding fiat money supply and artificially cheap credit – is rapidly approaching its logical endpoint everywhere, not just in Europe: excessive and unmanageable piles of debt, systemic financial fragility and weak growth.

For many, including quite a few of those demonstrating under the ‘Occupy Wall Street’ banner, this whole mess deserves the label “crisis of capitalism”. That this is nonsense I explained here. What we are witnessing is not a crisis of capitalism but the failure of statism. The present system, certainly the financial system, has very little to do with true capitalism, and if financial markets are now being demonized for their failure to go on funding political Ponzi schemes, then this means shooting the messenger rather than addressing, or even understanding, the root causes of the malaise. As I said, this is also a time of great confusion.

Failure of statism

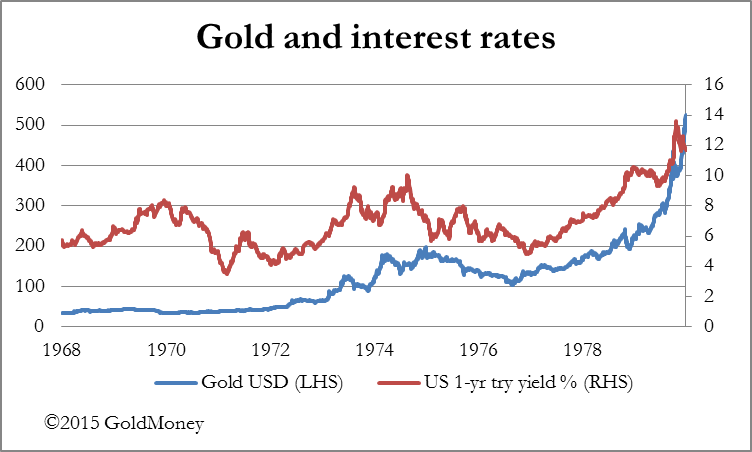

The monetary madness of recent decades was only made possible by the transition from apolitical and inflexible commodity money (free-market money) towards limitless, entirely discretionary fiat money (state money). This shift was completed on August 15, 1971, when this system was also made global. What does such a monetary system logically entail?

In a complete paper money system, banks cannot be private capitalist enterprises but must be extensions of the state because the state holds the monopoly of unrestricted money creation. The banking sector is cartelized under the state central bank. To operate a bank, you need a state license that requires that you open an account with the central bank.

In such a system, the central bank can create bank reserves out of thin air and without limit, and has thus full control over the level and the cost of such reserves. The central bank has therefore ultimate control over the funding of the banks and the availability of credit in the economy – which is now supposed to be magically freed from its natural constraint under capitalism: voluntary savings.

In such a system, it is generally assumed that the state cannot go bankrupt as it can always print more money to fund itself. It is equally assumed that the banks cannot fail and do not ever have to shrink, at least collectively, as ever more bank reserves can be made available to them – if need be at no cost, as has become – now that the system arrived at the point of ultimate excess – the global norm.

It can hardly be surprising that those who are in charge of the banks and those who are in charge of state finances have behaved for decades as if the Great Regulator of economic life, the threat of bankruptcy, was of no concern to them. Now that the system has finally overdosed on cheap credit and that the forty-year fiat-money-fed boom is over, reality is sinking in. And it comes as a shock.

There is a lot of talk of return to normality. The market has, of course, a way of returning to normality, which involves liquidating the excesses, clearing out the dislocations, defaulting what will not be repaid, and deflating prices that do not reflect real demand. Liquidation, default and deflation, however, are politically unacceptable, as they cut right to the core of our system of state-managed ‘capitalism’: the notion that the state is above the laws of economics and that it can bestow a similar immunity on its protectorates, most importantly the banks.

What’s €2 trillion among friends?

Back to the alternate reality of the policy debate in Europe. The hope of many financial market participants seems to be that the summit will reveal measures by Germany and France to erect a firewall around Greece in case it will default, that the banks will get ‘recapitalized’, and that steps will be taken toward further ‘fiscal integration’. The wish here is evidently that Big Daddy will finally step forward, that he draws a line in the sand, and says, hey, this stops here. Time out on the crisis.

There is only one problem: nobody has the money to do it.

Two days ago The Guardian broke the story, unconfirmed so far, that Germany and France had agreed to a €2 trillion bailout fund. In response, equity markets around the world enjoyed a brief rally. Finally, the big bazooka had arrived.

Really? I was wondering if nobody ever heard of Brian Cowen.

He was the hapless Irish chap who in 2008 played Big Daddy himself and implemented an official government back-stop for the Irish banks. And duly bankrupted his country.

If Merkel and Sarkozy were really stupid enough to launch a €2 trillion bailout fund, it would certainly pay to go short French BTANs and German Bunds right away. Germany and France have no money to bailout anyone. All they could do is pile on more debt on the already large and ever-growing debt pile of their own. It would not take the market as long as it did in 2008, in the case of Ireland, to figure out what the endgame must look like.

But surely, everyone involved must realize that the little boy in the crowd has already pointed out that Emperor Sarkozy and Empress Merkel have no clothes. Interest spreads on French bonds have already blown out, and Moody’s has warned that France’s AAA-rating (what? Triple-A?) might come under review. Credit-default spreads on German bunds have widened of late, and the cost of insuring against the bankruptcy of the Bundesrepublik Deutschland will most certainly only go one way: up. Have I mentioned that Bunds are the short of the century, and U.S. Treasuries, too?

The whole notion of ‘ring-fencing’ Greece is, of course, absurd, as if Greece had contracted some rare contagious disease from which healthier nations, such as Italy or Spain, had to be isolated. Ongoing, endless fiscal deterioration is, however, not a virus but a self-inflicted and ultimately fatal wound that all European states, and in fact, almost all modern social democratic states are already suffering from. The difference between Greece and Germany is one of degree, not principle.

For these reasons, the idea that some form of ‘fiscal integration’ could be the solution, is equally absurd, as if pooling the finances of the already-bankrupt and the almost-bankrupt will somehow give you a community of the fiscally strong. As if you could improve the financial standing of a trailer park community, in which some inhabitants are maxed out on their credit cards while others still have some borrowing capacity left, by giving all of them a joined bank account.

So does this mean that all political options are exhausted, that default, liquidation, and deflation are now unavoidable?

It will get worse

Not so fast. There are still some options left to governments. None of them will solve the problem, all of them will make the crisis worse. All of them are scarily ugly and destructive. Of course, I expect that all will be adopted by governments soon.

There is, of course, always the prospect of growing regulation and market intervention, of capital controls and the banning of short selling of government debt. I expect all of this to be enacted at some point in the not-too-distant future. Like all government intervention, it will make things worse and accelerate the demise of the system.

But the biggest of all policy mistakes is already being made, and we will get more of it, much more of it: printing ever more money ever faster.

The ECB will be forced/asked/convinced to support the market for government debt of ever more European states to an ever larger degree. Central banks and fiat money are not creations of the free market but of politics. Their role has always been to fund the state. We have already reached the point at which all major central banks are dominant buyers, frequently the largest marginal buyers, of their governments’ debt. The U.S. Fed is already the single largest holder of U.S. Treasuries, and when the just-announced second round of ‘quantitative easing’ in Britain will have been completed, the Bank of England will own almost a quarter of all outstanding Gilts. Funding the state directly with the printing press is the logical penultimate stage of the demise of the present global fiat money system, and all major economies are approaching it fast. The eurozone will be no exception. The ultimate step is loss of confidence in paper money and inflationary meltdown.

If there is one outcome from the European debt summit that I am most convinced about it is that another crucial step will be taken to accelerate the ongoing debasement of fiat money.

This article was previously published at Paper Money Collapse.

I have a question however. If government through its central bank can print money at will to fund itself… why the very high taxation (direct & indirect), the useless regulations, the high fines of all sorts etc., which drain people’s money AND block them from circulating and producing profit, jobs and so on? Sheer stupidity?

What would this particular money-printing system result to, if taxes were extremely low, regulations and interference to private lives non-existent and people were hassle-free to trade and work?

So I think the article is right, but there is another factor which the author overlooks: the use of paper money and regulation ability by government idiots (encouraged by various pressure groups/activists/do-gooders/saviours) to enforce certain whatever morals, which are unrealistic and malefic and have very nasty social consequences…

So, in my humble opinion, the real critic against statism isn’t the economical aspect but the legal one. Inevitably when statists have an unlimited supply of money and without the safety-valve of bankruptcy, then they face the temptation to use all these money not to fight poverty, or to spread wealth (as their original claim had been) but take an irrational leap into the area of “correcting” society and “managing” people’s lives, behaviours etc. according to a preferred ‘moral’ system – usually any one currently in vogue – which may not be exactly the best possible (lacking any philosophical thinking, any trial by time etc.).

However it isn’t Law’s role to manage and enforce moral beliefs. Law has a completely different reason of existence, role and function!

And it cannot be, in any case, a tool in the careless hands of vain moralists, who simply because they can print enough money believe that they have any right or are in any position to tamper with Laws… to twist them, manipulate them, distort them, in order to enforce their beliefs, pursuing their ‘dream’ of ideal society… until they wake up too late, noticing the nightmare they have made.

Therefore, I say that the real reason of this crisis, is not economical but a crisis of Law and justice, principally and basically.

Actually, the argument against statism is an economic one. The state is simply too expensive to support at it’s current size. That scale has become intrusive, offensively so, legislatively arrogant and dangerously controlling.

The danger is politicians. Small men whose goals are aimed at their own interests, not the nations. Europe is the ideal for them: a perfect career path into an unaccountable governing elite, disassociated from the people and safe from the annoyance of elections. For the people, Europe is a disaster that we can all easily understand.

The financial system has, as thearticle states, been allowed to not break to fuel thse political dreams. That is the real danger. Government becomes interested only when it gains control. It cannot be allowed to control market systems at any level. To do so would cause catastrophic damage. It is the equivalent of a geneticist preventing human evolution by favouring it’s own species and thus completely disrupting the rational order of failure and growth.

Fundamentally, the problem is the the market system was not allowed to succeed by failing.

No more cogent, succinct and accurate analysis of this crisis has yet been penned. All Eurozone leaders should be made aware of it. When my website designer returns from a brief vacation I will ask for this to be posted on the Cobden Partners site.

I urge all Cobden Centre readers to send this link to opinion formers, representatives, and those with an interest in understanding the crisis. With thanks to Detlev.